ACCT6007 Financial Accounting Theory and Practice Report

Context:

This assignment develops research and critical thinking abilities. It is a critical analysis/ review of an academic article. Changes in technology are impacting accounting and how accountants perform their jobs. This activity will provide students information on new trends in accounting field.

Instructions:

Download and critically analyse an academic article written by Jun Dai and Miklos. A. Vasarhelyi. This article can be found in the Torrens University library using the following citation:

Dai, J. & Vasarhelyi, M.A. (2017 Toward Block chain-Based Accounting and Assurance. Journal of Information Systems Vol. 31 No. 3, p5-21,

https://torrens.idm.oclc.org/login?url=http://search.ebscohost.com/login.aspx?direct=true&db=bsu&AN=126177472&site=ehost-live

You may use an essay format or any other acceptable academic format for critical review. Use APA 7 referencing style guide. Use minimum 10 academic references.

Answer the following questions during your analysis.

1. Discuss the three phases of blockchain technology? What is the potential use of blockchain technology in accounting?

2. The author discusses Triple Entry Accounting. What is your understanding of the concept?

3. Do you agree or disagree with any arguments made by the author? Explain your point of view and provide evidence in support of your point of views from other academic resources.

4. Critically review any potential issues or problems with blockchain technology being used in accounting.

To answer all the above questions: Review the article provided and search for related academic journal articles. Use minimum 10 academic references.

Solution

Introduction

In this paper, an article related to the Blockchain technology and the utilization of it in accounting is going to be analyzed critically. “Toward Blockchain-Based Accounting and Assurance” is the article that is going to be analysed here.

Three phases of blockchain technology

By considering the information shared in the article, it can be stated that since 2009, blockchain is getting evolved through three phases and these three phases are blockchain 1.0, blockchain 2.0, and blockchain 3.0. At the initial stage, the technology has been designed by considering it as a complementary technology to Bitcoin (Nebreda et al., 2021). By considering the viewpoint of Dai &Vasarhelyi(2017), it can be stated that the focus of blockchain 1.0 was on crypto-currency. For Assignment Help, In the case of Blockchain 2.0, it has been found that the similar trading is involved. However, the matter is that blockchain 2.0 has broader scope with respect to financial applications. The applications related to blockchain 2.0 include derivatives, digital asset ownership and others. However, the matter is that blockchain 3.0 has been able to expand the system further. It supports the system to work in other areas beyond business and financial applications. Blockchain 3.0 is found having the features to be used in voting systems, and government’s administrative works.

Potential Use of Blockchain Technology in Accounting

In the article, the utilization of the technology in the field of accounting has been elaborated. It is a fact that blockchain technology is gaining an attention (Noferet al.,2017). The authors have stated that the accounting profession can get a number of benefits with the utilization of this technology, and it has also been stated in the article that the technology is changing the working processes of accountants. The technology is helping accountants to keep accounts-related data securely, and it can be regarded as the most effective utilization of the technology in the field of accounting. Apart from that, with the utilization of the technology, companies are getting the ability to generate new accounting information system that can record validated transaction on secure ledgers. These transactions include monetary exchanges and accounting data flow within an organisation.

Triple Entry Accounting

It is a fact that technology is being changed in the world in an unprecedented manner (McKee et al., 2020). In the article, a significant discussion regarding triple-entry accounting has been made, and it has been stated that the triple-entry accounting is being used in these years in a significant manner as a secure and independent paradigm. As per the viewpoint of the authors, it can be stated that the triple-entry accounting system can bring an improvement to the reliability of the financial statement of an organization. The system requires transition authorization from a neutral with each party. It makes the transaction process secure, and that is why the utilization rate of the system is being increased. Apart from that, it creates a record for transaction so that adequate transparency can be maintained in regard to the overall transaction process.

Discussion Regarding The Arguments Made by The Author and Personal Viewpoint

Casado-Vara&Corchado(2019) have stated that in the last few years, blockchain has become one of the most frequently used words among scientists. The author has made a significant discussion regarding the utilization of the technology in the area of accounting and the viewpoint of the authors of this article is found has a similarity with the viewpoint of Casado-Vara&Corchado. The authors have stated that the technology is bringing a number of changes to the way accountants are working, and I am completely agreed to this statement.In this regard, I want to consider the viewpoint of Qasim&Kharbat (2020), who have also stated that the introduction to BT as a database is changing the landscape of accounting. It means that the statement of the authors is justified, and that is the main reason I have been agreed to them.

In accordance to this statement, the authors have provided significant evidence, and some benefits of the technology with respect to the area of accounting have been elaborated. The concerned technology can be regarded as a set of cryptographically linked data blocks (Alkan, 2021). By considering the viewpoint of Dai&Vasarhelyi (2017), it can be stated that the technology can bring an improvement to the area of record keeping in regard to the accounting process. The authors have also stated that the transparency in accounting process is getting enhanced with the utilization of the technology.I think that such statements are completely authentic as I have gone through some literary pieces for more research, and I found a similarity between the viewpoints of Dai&Vasarhelyi and the viewpoints of other authors. For instance, O'Leary(2019) has stated that private blockchain works for an individual organization; it has the ability to control the access to data. It means that it ensures security, and it means that the utilization of the technology is truly beneficial for account-related business areas, and these statements are justifying the statement of Dai&Vasarhelyi.

By considering all of these points, it has been possible for me to understand that the technology is benefiting the accounting system in an effective manner, and this is the argument that has been supported in the chosen article. As I have found adequate evidence for justifying the argument made by the author, I think that there is no need to be disagreed to the argument of these authors.

The paper has been written by using adequate number of references, and it means that credible information has been provided throughout the paper. In this regard, it is also important to state that the authors have written the paper in an understandable manner, and that is why any issue to understand the argument of the authors has not been faced. Along with providing information regarding the benefits of Blockchain, the authors have also highlighted the challenges related to the utilization of the technology in the field of accounting. The authors have considered the viewpoint of other researchers who shown the isuue of technology readiness in the case of EDI or ERP adoption, and by considering the use of blockchain in this field, the authors have developed an argumentative viewpoint that the same challenges can be faced in the case of blockchain adoption, and I found that these arguments are valid. I have gone through a number of websites and articles in order to know about the use of Blockchain and the issues related to the utilization of it. By considering the issues, I have also found that technical readiness is a considerable problem here, and that is why I have been agreed to the argument made by the author.

However, in a particular area, I have not been satisfied with the arguments made by the author. Shao, Zhang & Wang(2021) have discussed security issues in regard to the utilization of blockchain, and they the authors have proposed a model of accounting information security management related to blockchain. However, in this article, the author did not raise any argument regarding security management issue. From personal viewpoint, it can be stated that if the discussion would be made, the literary piece is expected to be more effective.

Potential Issues of Using Blockchain in Accounting

By considering the discussion made by the authors, it can be stated that the utilization of Blockchain can provide a number of benefits to the field of accounting. However, the challenges have also been discussed by the authors. By analyzing the information shared in the article, it can be stated that technological readiness can be regarded as a significant issue in regard to the adoption of blockchain in the area of accounting. Apart from that the authors have highlighted some questions that can come in regard to the utilization of this technology. Stratopoulos (2020) has stated that the adoption of the technology is at an experimental stage. The working principle of multi-entry system and its ability to interface with evolving traditional systems are still not properly know, and it can be regarded as a challenging matter with respect to the utilization of this technology in the concerned field. Apart from that, it is not clear how the actual blockchain model can be adjusted for real-time reporting, and it can also be regarded as a challenge with respect to the utilization of the technology in the area of accounting. These factors can be regarded as potential issues. When blockchain grows, it becomes more vulnerable, and in this regard, scalability becomes a potential issue. However, in the concerned article, discussion regarding scalability has not been made. However, the authors have stated that blockchain requires large computational resources. Otherwise, collusion and corruption-related issues can be faced (Dai &Vasarhelyi, 2017). From this point of view, it can be stated that the authors have highlighted some effective issues of using Blockchain in the concerned field, and the discussion regarding all of these relevant factors has made the article a proper source of information.

Conclusion

In this article, discussion regarding the utilization of blockchain in the field of accounting has been elaborated by considering an article. By analyzing the viewpoints of the authors of this article and by considering the information shared here, it can be stated that the article is informative, credible, and authentic.

References

.png)

5011SP5 Accounting for Management M Report Sample

Learning Objectives addressed in this assessment:

CO1: Apply basic accounting principles and concepts to understand what accounting information is, what it means and how it is used;

CO2: Explain the significance of accounting information in the business environment;

CO3: Read and interpret financial reports and apply knowledge to critically analyse corporate financial and non-financial information.

Graduate Qualities developed by this assessment:

GQ1: You need to operate effectively upon fundamental accounting practical knowledge;

GQ2: You are prepared for lifelong learning and professional practice;

GQ3: You are working to be an effective business-related problem solver;

GQ4: You can work autonomously and independently;

GQ5: You are committed to ethical action & social responsibility for business activities.

GQ6: You can communicate effectively in written language.

This assessment involves 2 (two) parts: (1) a Written Business Consultation Report (80%); (2) an Oral Presentation of your Consultation Report to Company A (20%). Your total marks for this assessment will be based on the successful completion of both tasks.

This assessment can be completed individually, or in a group of no more than two students (These two students must enrol in the same class to complete the oral task together).

Required:

Write a consultation report for CSL Limited

(1) Choose CSL, a pharmaceutical company from the list of Selected ASX Listed

Pharmaceutical Companies, which is provided as a separate file under Assignment on the course website. One company will be CSL Limited (ASX: CSL) (that has been specified earlier) and the other will be used as a benchmark for analysis against CSL Limited.

Note: If you cannot find an appropriate company when following the above selection rules, you may randomly select a company from the list. However, you need to clearly state the reason for the selection you make in your assignment.

(2) After selecting the two companies, go to the company information database DatAnalysis

Premium via the UniSA Library website. Under Company Reports, search for the companies you selected according to their ASX Codes or part of the company's names. Next, go to Financial Data to review these companies’ financial statements for the financial years from 2020 to 2022 (should 2022 data are not available for the company chosen, you can use data from 2019 to 2021). Hint: Provide a Full Analysis of these Companies’ Financial Ratios across 3 years.

(3) Based on the available data, calculate 3 (three) years (2020-2022) financial ratios of CSL Limited and the selected benchmarking company. Based on these ratio results, analyse and compare the financial performance of these 2 (two) companies. Your calculation and comparative analysis should focus on any 2 (two) of the following four points (explain why you choose these two):

a) Which company is more profitable and generates healthier returns?

b) How well are the two companies managing their resources? Do you think Company A is more efficient in managing its assets compared with the benchmarking company?

c) Can Company A meet its short-term debts? How is its liquidity compared with the bench marking company?

d) Do you think Company A will stay in operation in the long term? How is its long-term financial stability compared with the benchmarking company?

Your answer should be supported by sufficient evidence (i.e. financial statement data and/or ratio results) and analysis. You can also review the annual reports of the two companies for the last three years (Annual Reports are available to download in DatAnalysis Premium), and use the information disclosed in these reports to complement your answers. For example, whether there are issues of concern mentioned in the annual reports that can imply Company A’s financial health and risks and how this might influence your comparative results.

(4) Go to the benchmarking company’s website and investigate whether and how it reports information about sustainability issues, such as carbon emissions, energy consumption, or community contributions, in its annual reports or stand-alone sustainability, CSR (corporate social responsibility), or environmental reports. Do you think Company A should follow what the benchmarking company is doing? Do you support the view that they have performed optimally for its sustainability reporting by Company A, or do you think the company should

prioritise profit growth more? Explain your views.

Solution

Introduction

Rationale for Selected Company

Financial Ratio Analysis

Company Selection

Hydration Pharmaceuticals Company Limited is a consumer product company that sells tablet liquid and powder products in the North American markets of Canada and the United States. For Assignment Help, Healthy Hydrated Solution markets sit in overlaps of over-the-counter medicines, functional vitamins, and mineral and vitamin supplements, which will help, boost health and wellness with a range of rehydrating products.

CSL Limited is an Australian Biotechnology company that develops, manufactures, and conducts research and market products for preventing serious medical human conditions. CSL Limited is considered a global biotechnology company with dynamic portfolios of life-saving medicines for treating immune deficiency and haemophilia, an immune deficiency, and a vaccine for preventing influenza (Csl, 2023).

Rationale for Selected Ratios

In this study, Hydration Pharmaceuticals Company Limited will be chosen as the benchmark company as both companies are multinational companies and these companies have significant changes in their revenue growth in each financial year. Both of these companies are involved in dealing with chemical products and both of the countries have an origin in developed economies.

Financial Analysis of CSL Limited

Liquidity Analysis

The liquidity Ratio for CSL Limited for the years 2020, 2021, and 2022 came at 3.01, 2.38 and 2.51 respectively. In financial markets, investors will conduct investment discussions with the level of risk perception and available information and study business trends (Jermsittiparsert et al., 2019).

Profitability Analysis

From the ratio analysis, it can be stated that CSL Limited experienced growth in its profitability while Hydration Pharmaceuticals Company Limited experienced significant losses for the three financial years of 2020, 2021 and 2022. The Cash Ratio of CSL Limited for the financial years 2020, 2021, and 2022 was .55, .58 and 1.4.

Financial Analysis of Hydration Pharmaceuticals Company Limited

Liquidity Analysis

Financial ratio plays a vital role in revealing corporate financial soundness, which helps enterprises maintain their competitive positions achieve stable development and eliminate potential risks (Kliestik et al., 2020). The current ratio is considered the liquidity ratio, which helps to analyze if the firm possesses enough resources to meet its short-term liabilities. It is generating by dividing the total current assets by Current liabilities.

The liquidity ratio of Hydration Pharmaceuticals Company Limited for the years 2020, 2021 and 2022 came at 9.02, 7.43 and 7.4. A current ratio above two implies that the company possesses enough current assets than liabilities for meeting its short-term debt obligation. The current ratio of less than one will imply that the company will face significant difficulty in meeting its debt obligations.

Profitability Analysis

Hydration Pharmaceuticals Company Limited's Current ratio came above 6 for three financial years. It implied that the company possesses enough cash and is more than capable of meeting its debt obligations. The gross profit Margin is calculated by dividing the gross profit by the revenue of the company. In certain situations, due to a sudden decrease in revenue because of external factors company may experience a negative gross profit margin ratio. The Cash Ratio of Hydration Pharmaceuticals Company Limited for 2020, 2021, and 2022 came at 7.2, 5.1 and 5.18 respectively.

The negative gross profit margin ratio of Hydration Pharmaceuticals Company Limited implies that the company has not been able to control its costs of production. From the financial report of Hydration Pharmaceuticals Company Limited, it is found that the company experienced a severe net loss for the financial year and generated a loss per share. The revenue of Hydration Pharmaceuticals Company Limited for the years 2020, 2021, and 2022 came at 6127178$, 3756695$, and 296285$ while the net loss came at 8951661$, 743663$ and 3434151$. The loss per share for 2020, 2021, and 2022 came at .06$, .01$, and .12$ respectively.

Comparative Analysis

Profitability Ratio

.png)

Figure 1: Profitability Ratio of CSL Limited

(Source Self-created)

Financial statements include the income statement, balance sheet cash flow statement, and accompanying notes (Brown et al., 2022).From the data obtained from, the financial statements from 2020, 2021, and 2022 of CSL Limited and Hydration Pharmaceuticals Company Limited, it is found that CSL has agreed to health reasons for its sustained growth. Hydration Pharmaceuticals Company Limited has incurred significant losses for the three financial years. CSL Limited was more profitable and generated healthier returns. It also experienced significant growth in its profitability that is considered vital for maintaining the company's sustainable growth. Ratio analysis plays an important role in improving diagnostic accuracy (Pascal et al., 2021). It can be agreed with the fact that Company A (CSL Limited) is more efficient in managing its assets in comparison to Company B (Hydration Pharmaceuticals Company Limited). Even with greater revenue and asset Hydration Pharmaceuticals Company Limited have been unable to conduct effective utilization of its resource to enhance its business performance on the other hand, CSL Limited with less revenue and cash in hand have been able to generate sustainable and healthy profits while conducting its business operation in the three financial years.

Liquidity Ratio

The capital market plays a vital role in meeting the capital needs of the business world for developing and being sustainable (Pattiruhu, 2020). In accordance with the benchmark Company (Hydration Pharmaceuticals Company Limited), it can be stated that the liquidity ratio of the benchmark company is greater than that of CSL Limited. The liquidity ratio of Hydration Pharmaceuticals Company Limited is considered to be greater than 5. In case of meeting short-term debts, Hydration Pharmaceuticals Company Limited will be able to meet its short-term debt obligations while CSL Limited will face significant challenges in meeting its short-term debt obligation as its current ratio is significantly low and it poses significant liabilities in comparison to its assets.

.png)

Figure 2: Liquidity Ratio

(Source Self-created)

Pre-components Percentage Analysis is used to compare one account to the total account (Sihombing et al., 2022). From the analysis, it is concluded that Company A will be able to stay in operation in the long term. The Hydration Pharmaceuticals Company Limited has experienced significant losses over the three consequent years. The company was experiencing yearly losses while CSL Limited will be able to stay in operation for the longer term as the company was experiencing more than 10% revenue growth in each financial year. Hydration Pharmaceuticals Company Limited is experiencing a steep decline in its revenues and is experiencing severe losses so it will be significantly challenging the company to sustain in the longer run.

.png)

Figure 3: Quick Ratio of Hydration Pharmaceuticals Company Limited

(Source Self-created)

Sustainability Reporting Initiatives

Corporate Social responsibility is considered as a management concept where companies integrate environmental and social concerns in their business operations and interactions with stakeholders. The emission of greenhouse gasses from the combustion of fossil fuel is related to the earth's climate warming and air pollutants, contribute to global warming. CSR is significantly generalized in categories like environmental responsibility, human responsibility, and economic responsibility. It helps companies build credibility and trust with their stakeholders. Hydration Pharmaceuticals Company Limited’s environmental and social issues are reported in its financial statements. The annual financial statement implies that the company operations are not regulated by any kind of environmental regulations under any kind of commonwealth law. Long-term incentives is intended to reward executives’ sustainable long-term growth. It is aligned with shareholder interests. Hydration Pharmaceuticals Company Limited is required to allocate a significant percentage of its net profits towards corporate social responsibility activities. It manufactures rehydration electrolyte products and the company educates the causes of management.

Should CSL Follow the Same

Company A (CSL Limited) should not be following Company B (Hydration Pharmaceuticals Company Limited) in reducing its environmental emissions. The key energy sources of CSL manufacturing factories are considered as natural gas and electricity (Csl, 2023). In CSL plasma network centers electricity is the main source of energy. Combined manufacturing and CSL plasma Centre have significantly contributed to MOT of CSL energy Consumption and greenhouse emissions. As part of its sustainability strategy, CSL has adopted for sustainable future for employees, patients, and communities. CSL announced Carbon emissions that serves as a transparent roadmap for decarbonizing global operations by cutting down carbon emissions. CSL announced the building of cell-based influenza vaccines CSL proprietary and Q fever vaccine. CSL facilities will help implement onsite renewable energy generation, electrification to reduce reliance on natural gas, reclaiming water reuse, and heat recovery for the waste management process.

In the year 2020, CSL Limited announced its first emission reduction targets. Based on its targets, CSL Limited has committed to a 40% reduction in Scope 1 and Scope 2 emissions by the year 2030 using the averages of CSL's FY19-21 emissions as the basis (Csl, 2023). CSL has announced them by the year 2023 it seeks to reduce emissions, which is associated with its operation, and ensure suppliers will contribute 67% per cent of Scope 3 Emissions are associated with science-based target initiatives and CSL targets are being aligned to limit global warming to 1.5 degrees Celsius. In addition to climate resilience, emission reduction and energy are considered as key components in CSKL corporate sustainability strategies and are committed to proactively adapting and mitigating climate changes. CSL supports the use of proper mechanisms for addressing climate change, which are consistent with international approaches and are designed to encourage investment and innovation in GHG emission mitigation technologies while also limiting adverse effects on national economies.

Sustainability Reporting by CSL Limited

Company A (CSL limited) should implement its sustainability initiatives as the world is moving towards an eco-friendly approach it will help in maintaining the company's sustainable growth in the long run. CSL Limited's commitment to a healthier approach implies delivering to both the planet and its people. CSL Limited seriously takes this responsibility to further maintain environmental considerations in buying which will help in delivering a sustainable world for the next century. CSL Limited recognizes responsible management and efficient use of natural resources that are vital for a company's sustainable growth. CSL Limited recognizes that responsible management and efficient use of natural resources are key to the company's suitable growth and will help in implementing its ability to deliver an effective and reliable supply of life-saving medicines. CSL Limited supports meeting the goals of the Paris Agreement for avoiding the worst climate change impacts that are being identified by the intergovernmental panel on climate change. CSL Limited continues to execute the sustainability strategy for integrating sustainability considerations in business decisions and reducing carbon emissions (CSL, 2023).

Conclusion and Recommendation

To conclude we can state that, the consultancy report of Hydration Pharmaceuticals Company Limited and CSL Limited consultancy report has been prepared. The financial position of the two companies for the three financial years has been analysed to evaluate the financial health of the company. The liquidity ratio and the gross profit margin ratio have been evaluated for three years to evaluate the company's financial performance. Hydration Pharmaceuticals Company Limited has incurred a significant amount of losses in the three financial years of 2020, 2021, and 2022 while CSL Limited has experienced significant growth in its profitability that will help in maintaining its sustainable and healthy growth. In terms of reducing environmental emissions and implementing CSR responsibilities, CSL Limited has a significant edge over Hydration Pharmaceuticals Company Limited. CSL Limited has specific emission reduction targets while operations of Hydration Pharmaceuticals Company Limited are not under the jurisdiction of Commonwealth Law. To improve the business performance CSL Limited and Hydration Pharmaceuticals Company Limited can adopt further clarification of their business plan and adopt a flexible financing structure, which will help in improving their business operations and help in maintaining long-term sustainable growth.

Recommendations

- Evaluating and Clarifying Business Plan :

A business plan is a road map for financial, marketing, operational, and financial standpoints. Hydration Pharmaceuticals Company Limited will have to adopt modern technologies in its cost of production to reduce its operational cost, for the company to be able to experience profitability growth in each financial year. A sustainable business plan is required to be adopted and proper evaluation must be done to deal with the shortcomings. In the case of CSL Limited, the Company has to continue its business operations and avoid acquiring further liabilities or it may face bankruptcy for being unable to meet its debt obligations. Proper experts must be hired to implement an effective business plan that will help in maintaining sustainable growth of the company and maintain environmental ethics while continuing its business operations.

- Adopting Flexible Financing Structure

Financing structure refers to the mix of equity and debt, which are used by a company to finance its operations. Hydration Pharmaceuticals Company Limited has to implement asset utilization to increase its revenue generation and reduce its operational costs. For example, the company may allocate some jobs to ex-employees with expertise, which will significantly improve the quality of the output. Employees can be provided with flexible working hours to increase their productivity. In the case of CSL Limited, the company must focus on reducing its liabilities and implement debt restructuring so that it will not affect its business operations. It will help CSL Limited to avoid the chances of bankruptcy and avoid being sued for debt.

Reference list

.png)

TACC606 Accounting Business Report Sample

Name of the Student

Name of the University

Author’s Note

Table of Contents

Introduction:

Accounting for property, equipment and plant is considered an important element to record the right value of assets in the company’s financial statement. Generally, Net PPE value is determined by Gross PPE, plus Capital Expenditure, minus Accumulated depreciation. In this business report, ranges of measurement are being discussed. Different companies are recorded PPE following different accounting methods at the end of the financial report (Chadda and Vardia, 2020). However, the matter is most important to present such financial records in a most realistic and accurate way. Information about the significant portion of total assets of an entity will be discussed after assessing financial reports of two ASX listed companies: Goodman Group and Genesis Energy Ltd. In short, the objective of the business research report is to discuss and evaluate various disclosures related to PPE recoded by each company.

Evaluate PPE disclosure of the selected companies:

According to AASB116, all tangible items are measured as PPE if they are in use of the production process or in operation as a lease or purchased. However, this standard is generally recorded as PPE which expected to be used during more than the one accounting period. Thus better position of PPE indicates that the company was in good condition to exhaust their expenditures over the period. Goodman group, the chosen company measured their items of PPE at fair value of the cost at the recognition date. Interestingly, the figure of PPE has been increased over the last 3 years. In 2020, PPE was 115.60 $M and 128.7 $M was recorded in 2021. Here Goodman group leases their office buildings, office equipment and motor vehicles. Certain investment properties and developments classified as stocks are also built on land held under claiming interests of leaseholds. The company measures and recognizes an accurate application of asset and a “lease” liability at the date of initiation of lease agreement. The financial note clearly discussed that the chosen company initially measured the asset value at cost plus direct costs incurred considering estimating costs for reinstating the underlying asset or the place where it is situated, deducting any lease incentives collected. On the other hand, the lease liability of the company measured initially at the current value of the payment of rental which are yet to be made payment on the date of the commencement, less discounted incremental borrowing rate. After such initial measurement, the lease liability is determined at cost of amortization and interest expense.

In case of Genesis Energy limited, the valuation of PPE was based on a discounted cash flow model prepared by the management of the company. The recorded financial report in 2020 clearly disclosed that the asset value 3485.04$M which was high compare to the previous year 3367.70$M.Interestingly, the second chosen company valued their assets based on unobservable market data which is based on fair valuation method. Thus the valuation of the property of the company is based on a lot of assumptions. Depreciation of the assets is generally calculated in the method of straight line where the projected value of assets is being reviewed annually. Here the leased assets of the company are recorded at cost less accumulated depreciation and losses of impairment. The leased asset is being depreciated throughout the term of lease.

Validation to add items in PPE for that measured used:

It is completely valid to add items in PPE model of both the companies gives the measured used. During the scaling of the business, it is important to add one or several items of assets which might be obtained in exchange for a “non-monetary” asset or assets, or may be to position PPE between non-monetary and monetary (Prodanova,et al., 2022). The cost of such an item will be assessed at fair price unless the substitute transaction lacks substances related to commercial. However, the fair value of the adding items in PPE is reliable measurable if the possibilities of the several estimates within the range can be considerably assessed and practiced or the inconsistency in the range of fair value measurements is not considerable for that adding up assets.

Interpretation of total amount of PPE in the financial statement:

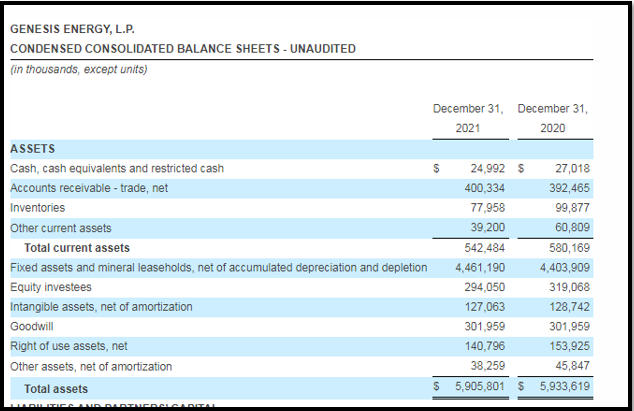

Plant, Property and Equipment are generally interpret the total amount long term fixed assets of the company which is tangible, identifiable and expected to generate an economic return for more than one operating cycle of the company. Here the total value of PPE can be derived from Gross PPE with adding up capital expenditures, less accumulated depreciation for the financial year. Based on the recent year’s reports of Genesis Energy LP, the company has been expecting to invest in fixed assets to sustain growth by aiding in operations.

.png)

(Source: Genesis-energy LP, 2021)

Initially, the carrying values of PPE items were valued at costs which are significant in relation to the total costs. Here Genesis Energy Company practiced revaluation method. Generation assets were revalued at 30th June 2021 to $3273.2 million resulting in a net gain of revaluation of $191.5 million. Here the carrying value of assets in June 2020 derived from $3177.2 at fair value of cost deducting accumulated depreciation and impairments which reduced the end carrying value of assets from $3662.5 to $3367.7 million (accumulated depreciation figure $294.9 million. It has been found from the financial report (specifically in Balance sheet) that assets were generated through following revaluation method $191.50 million. Interestingly, accumulated depreciation was increased from the year June 2020 ($535.1 million) to June 2021 ($570.7 million).

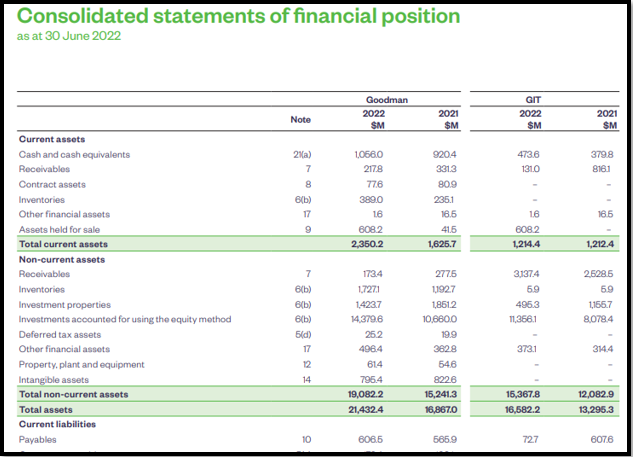

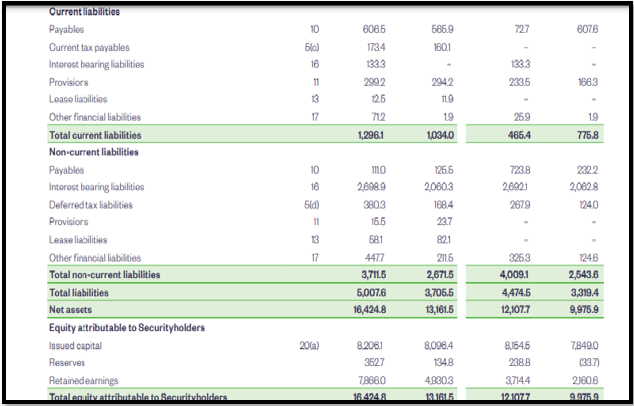

On the other hand, investment in plant, property or equipment of Goodman Group has been increased which disclosed in their financial report from $115.6 million to $128.7 million. Investment properties are carried at fair value. Here the fair value of stabilized investment properties of the Goodman Group is calculated considering present prices in an active market for similar properties in the same condition and location and also allowing for same lease and other contracts. The “carrying” value of PPE at the end of the financial year interprets the amount of newly acquired assets list of capital expenditure, and net gain from fair value adjustments and so on.

.png)

(Source: Goodman Group, 2022)

The value of assets are initially measured at cost plus any direct costs associated like labour costs, to restore the underlying assets less any lease incentives received over the particular period. In this way, total amount for PPE is being interpreted from the statement of financial.

Measurement comparison used by the several companies for same type “items” in PPE and finding inconsistencies, if any:

PPE is measured as per revaluation model or cost model by many companies considering the benefits as per the company’s financial requirements over the period (Karim, Islamand Bhuyan, 2020). PPE firstly recorded at its costs, consequently priced either using a revaluation model or cost and depreciated later, which indicates that such “depreciable” amount can be comprised on a methodical basis over the useful life of PPE. The carrying amount of PPE under the cost model, is generally being measured at its cost less accumulated loss and accumulated depreciation for impairment of assets. Goodman Group has been used such cost model in contrast of Genesis energy LP which used revaluation model for measuring PPE items for their company. Under the revaluation model, an asset is recorded at the revalued amount less depreciation which is accumulated and any losses of impairment. Generally the management of the company uses this revaluation method to ensure most accurately the fair value of PPE (Prodanovaet al., 2022). However, the business entities can switches from cost model to revaluation model, but there is no need for applying this change in the accounting policies. The chosen company, Genesis energy has previously experienced fluctuation in fair value of some items of PPE. Thus, all items of property, plant, and equipment was then revalued by the management and reported accordingly. Compare to cost model, the revaluation model helps to avoid inconsistencies of assets and the reporting figure in the financial statements that ascertain different values or cost at different date. Revaluation gain is recorded in the balance sheet as equity as a separate capital reserve, called “revaluation surplus”. On the other part, revaluation loss is being booked in the “statement of income” as considering expense. However, if there is some balance in the revaluation surplus presents in the accounts of the company from any previous revaluation gains of the same asset, that surplus of revaluation amount will be adjusted first and accounted for. Any excess revaluation loss will be recorded in the statement of income of companies. In that circumstances and for treating those surpluses and losses, the company will measure their PPE items of similar categories under revaluation model. As cost model is relatively simpler than other model of PPE measurement and it is based on cost of historical principles, inconsistency can be found in the fair value changes of PPE over the period.

Considerable factors that important for setting up accounting policies for the company relating to PPE:

Accountants need to evaluate various factors before establishing company accounting policy relating to PPE. In case of structuring of PPE model for the company, all the factors such as useful life of the asset, depreciation method for PPE, correctly determination of value of assets, policy for PPE impairment and so on.

Detailed discussion of above mentioned factors are as follows:

Functional life of an asset: Useful life is generally indicates approximate efficacy period imposed on a range of the business entity’s properties. This information provided by the accountant is valuable for setting up accounting policies to PPE because useful life of assets forecasts end at the point where assets are anticipated to become outdated. The design of the valuable life of each asset, premeditated in years can be practiced as a reference to make the depreciation plans for inscribing outflows associated to investment purchase of goods for the company.

Depreciation method for PPE: Choosing right depreciation method for PPE valuation is significant as the accounting standard defines such depreciated value is a systematic allocation of fund over its useful life which can be used for cash collection or capital generation for the business. The carrying amount of PPE items can be measured by applying “straight line” method or reducing method or unit of production method. For instance, Genesis Energy uses the straight line method for valuing long lived assets to cover the total costs of an asset over its lifespan instead of recovering their purchase costs on an immediate basis. In accelerated method for PPE calculation, which generally creates more depreciation in early phase of the fixed asset. It considers the point of income tax which is a reasonable factor to make difference the value of assets for this reason.

Appropriate asset valuation: It is indeed an important factor for PPE to make an accurate asset valuation which is all about setting the right value of property including inventories, houses, equipment or land. It is typically happened when the management of the company is to make a decision to sold, taken over or insured their fixed assets. Such perfect valuation thus is significant factor for PPE to generate maximum cash for the growth of the business in future.

Impairment policy of PPE: As prescribed in accounting policy, an accountant must not carry an asset in the firm’s financial statements an exceeding highest amount which might be recovered through its sale or use. If the carrying amount of asset exceeds the recoverable amount, the asset is described as impaired then (Hladika, Gulin and Bernat 2021). Thus the accountant must maintain such impairment policy to provide the right information to the stakeholders of the company. In case the accountant find its fair market value of PPE items is less than its carrying amount then, it should be recorded as impairment loss for that difference. Therefore, accountant practitioners must be practiced their impairment policy of PPE with full conviction and clarity in books of accounts.

Initial and consecutive recognition criteria of PPE: An Accountant must initially measure their PPE items at its costs. However, there is a choice of subsequent measurement. The criteria of the recognition must be fulfilled with discussing the matter with the management of the company. For instance, Genesis Energy LP used revaluation model for the PPE recognition after initial measurement of assets at its costs. On the contrary, Goodman Group used cost model and allocate depreciable asset value on a periodic basis over its useful life. Here the fair value variations were being ignored while accounting those records into book.

Detailed observation on succeeding measurement of PPE:

Initially PPE must be recorded at its cost which includes purchase price of the asset adding up duty of import, directly associated costs (cost of installation, freight in, site preparation cost, testing, professional fees, and inescapable costs such as disassembling, removing and reinstating the site cost. Policy setters however, will definitely choose either the cost or the revaluation model in the subsequent phase of measurement of PPE. Under paragraph 6 of AASB 116, items of PPE are tangible in nature and expected to be used for more than one period. Thus subsequent measurement policies of PPE need to have an immense importance for the accounting practitioners. For the purpose of accounting, entities need to be measured subsequent expenditures for determining if it may be capitalized or treated as expense at the time of occurrence.

However, the asset recognition criteria must be fulfilled in case of subsequent PPE expenditures. It means that future economic benefits or the ability to contribute to the objectives of the entities for delivering goods or services for one that one accounting period can be capitalized. On the contrary, subsequent measurement for that expenditure on an item of PPE that fails to meet the recognizing criteria of asset at paragraph 7 of AASB 116 shall be considered as expense and positioned in the income statement of the company’s financial records at the end of the reporting period. Under the model of cost, if fair value calculates correctly, the value of the asset then should be calculated at its cost value, subtracting “accumulated depreciation” less “loss of impairment”.

To categories most PPE, AASB specifies the accounting treatment of PPE while recording the books of accounts in the financial statement at the end of the financial year. The cost model incorporates items of PPE being held at a lower price of depreciation and loss of impairment. On the other hand, the carrying amount of PPE whose fair price can be quantified reliably utilizing the revaluation model. In other words, where reliable cost measurement can be attained it is like that the expenditure would produce future economic benefits in case of subsequent expenditure on an item of PPE are for a part of replacement, major inspection, and enhancement or for safety or environment equipment. Here the fluctuations of fair value can be measured and accounted for at the end of the financial period. Under this model, the accountant shall take asset’s carrying value at its PPE’s fair value at the time of the revaluation less any following accumulated depreciation and loss of impairment. In other words, the asset is carried at the rate of revaluation if the model of revaluation is being practiced. This formula of measuring PPE items under this revaluation model is the fair value less asset’s cumulative depreciation along with any lack of impairment.

Recommendations to accounting standard setters related to PPE measurements:

Perfect policy choices must be taken considering the use of the PPE items of an entity. Interestingly, accounting standard setters are already discussed that such assets must be measured considering either the expense model or the model of revaluation. This is completely a management oriented decision whether which model will be choices later in the subsequent expenditure measurement of PPE items. As per the cost model, if fair value can be measured truthfully, the asset shall be priced at its cost subtracting “accrued depreciation” less loss of the value of impairment. On the other hand, the revalued sum is equal to fair value at the time of revaluation less following up any accrued losses of impairment and depreciation under the method of revaluation model. According to AASB 116, it is recommended to practitioners that all assets in the same group can be re-examined if one value is revalued. For instance, if the management of an entity wishes to revalue its equipments or buildings, and recorded to have five buildings and ten machineries, then it will re-evaluate all number of equipment and buildings of that entity. For simplicity reason, the cost model is always preferred and easy to measure PPE items for subsequent measurement purpose over revaluation model. However, an important recommendation for changing one measurement model to another can be taken place by any entity for better presentation of fluctuations of fair value where cumulative depreciation is calculated and any lack of impairment.

Conclusion:

The above report clearly discussed principles considered for identifying items of PPE as prescribed the accounting standards. However, different companies are followed different policy to record subsequent expenditures of entities after the initial measurement of PPE at cost. The above chosen both companies are followed different measurement policy for their PPE items. It makes it rational for PPE to be calculated at “Cost plus other accumulation” for obtaining the item of PPE’s definite cost for prospective purposes of valuation. The sum of the less accrued depreciable asset moves to the statement of performance (B/S) and the fee over the period goes at a cost to the P/L statement. Undeniably, both the chosen firms attain the right depreciation amount of assets and fulfilled requirements of overseas reporting from any assessment. Thus PPE reporting and measurement process is vital for any business firms at the financial year end.

Appendix:

Goodman Group Balance Sheet 2021-2022

Genesis Energy, LP Balance Sheet

References:

.png)

- Assignment - Child Care

- Assignment - Mathematics

- Assignment - Accounting

- Assignment - Auditing

- Assignment - Biology

- Assignment - Law

- Assignment - Management

- Assignment - Nursing

- Assignment - Finance

- Assignment - Computer Science and IT

- Assignment - Humanities

- Assignment - Economics

- Assignment - Statistics

- Assignment - Architecture

- Assignment - Engineering

- Assignment - cookery

- Assignment - Marketing

- Case Study - Chemistry

- Case Study - Accounting

- Case Study - Law

- Case Study - Management

- Case Study - Nursing

- Case Study - Finance

- Case Study - Computer Science and IT

- Case Study - Engineering

- Case Study - Economics

- Case Study - Biology

- Case Study - Auditing

- Case Study - Marketing

- Case Study - Project Management

- Coursework - Diploma

- Coursework - Accounting

- Coursework - Auditing

- Coursework - Biology

- Coursework - Management

- Coursework - Nursing

- Coursework - Finance

- Coursework - Computer Science and IT

- Coursework - Engineering

- Coursework - Humanities

- Coursework - Child Care

- Coursework - Project Management

- Coursework - Economics

- Coursework - Cookery

- Coursework - Law

- Dissertation - Accounting

- Dissertation - Auditing

- Dissertation - Biology

- Dissertation - Law

- Dissertation - Management

- Dissertation - Nursing

- Dissertation - Finance

- Dissertation - Computer Science and IT

- Dissertation - Humanities

- Dissertation - Economics

- Essay - Politics

- Essay - Childcare

- Essay - Accounting

- Essay - Biology

- Essay - Law

- Essay - Management

- Essay - Nursing

- Essay - Computer Science and IT

- Essay - Humanities

- Essay - Economics

- Essay - Auditing

- Essay - Engineering

- Essay - Architecture

- Essay - Finance

- Essay - Science

- Essay - Marketing

- Programming - Computer Science and IT

- Reports - Management

- Reports - Computer Science and IT

- Reports - Project Management

- Reports - Marketing

- Reports - Nursing

- Reports - Engineering

- Reports - Accounting

- Reports - Humanities

- Reports - Finance

- Reports - Architecture

- Reports - Biology

- Reports - Economics

- Reports - Childcare

- Reports - Law

- Research - Accounting

- Research - Auditing

- Research - Biology

- Research - Law

- Research - Management

- Research - Nursing

- Research - Finance

- Research - Computer Science and IT

- Research - Science

- Research - Engineering

- Research - Humanities

- Research - Economics

- Research - Project Management

- Research - Statistics

- Research - Architecture

- Research - Marketing

- Thesis Writing - Computer Science and IT

- Thesis Writing - Engineering

- Thesis Writing - Biology

- Thesis Writing - Finance

- Thesis Writing - Humanities

- Thesis Writing - Auditing

- Thesis Writing - Economics

- Thesis Writing - Law

- Thesis Writing - Nursing

- Thesis Writing - Accounting

- Thesis Writing - Architecture

.png)

~5.png)

.png)

~1.png)

.png)