ACCT6001 Accounting Information Systems Sample

Question:

Background

Good Group Pty Ltd is a small firm located in Sydney. The company specialises in providing its customers with low-cost homewares. The firm was established 2 years ago and has recently experienced operational inefficiencies and accounting errors. You have been hired to evaluate Good Group’s business processes which are described in the following paragraphs.

Business Processes

At Good Group, the revenue processes are conducted by employees including sales staff, warehouse staff, an accountant, and collection clerk. A description of their duties are as follows:

- Sales staff receive customer orders by email and prepare a four-copy sales order form. One copy is filed, one copy goes to the warehouse staff, one copy goes to the accountant, and one copy is posted to the customer.

- After receiving sales orders, warehouse staff prepare a packing slip, take the proper items from the warehouse, and ship them with the packing slip enclosed. The sales order is stamped with the ship date, and the shipping log is updated. The sales order is filed by customer number. If the ordered goods are not in stock, the customer is notified and the sale does not proceed. When sales cannot proceed because there is no stock, the warehouse staff will order the items to replenish stock to their desired levels.

- After receiving the sales order from sales staff, the accountant reviews the customer records and either approves or disapproves customer credit. If the customer’s credit is approved, the sales order is stamped “approved”. The accountant then prints two copies of the invoice. One copy is posted to the customer and one copy goes to the collection clerk. Finally, the accountant matches the approved sales order to the invoice and files these by customer number.

- After receiving a copy of the invoice, the collection clerk posts the sale to the sales journal and the accounts receivable subsidiary ledger. Daily totals from the sales journal are sent to the accountant who posts these sales summaries to the general ledger.

- If the customer pays by cheque, the collection clerk stamps the cheque “For Deposit Only” and records it in the accounts receivable subsidiary ledger. The cheque is also recorded in the cash receipts journal by the collection clerk. Once this information is entered into the ledgers, the collection clerk deposits cheques in the bank account weekly. For invoices paid using electronic banking, receipts are entered into the accounts receivable and cash book ledgers at the end of each week.

- The accountant receives a monthly summary of cash receipts from the collection clerk. The accountant records these summaries in the general ledger. The accounts receivable ledger is reviewed monthly by the accountant and phone calls are made to customers that have not paid their invoices within three months.

Required

1. Draw a business process map to reflect the processes at Good Group Ltd (include swimlanes in your diagram).

2. Identify strengths and weaknesses in the existing system including the internal controls used

3. Research and report on ways to improve the business processes (include references to support your suggestions).

4. Draw a new business process model that outlines your suggested improvements

5. Include in the Appendix of your report, minutes of meetings held between group members (Include a list of actionable tasks, team members responsible for those tasks, deadlines, and progress towards completing tasks).

Answer

Introduction

The business process map has helped to understand the steps of organizational procedure regarding the completion of several tasks such as ordering a product, hiring employees, and employee engagement. This report has described efficient business process map based of the activities of good group pvt ltd. and the strengths and weakness of this company. Additionally, improving ways and new business models has been evaluated for developing suggested improvements.

Business process map

According to business process mapping, good groups can identify who, what, how, when, and where and analyse the structure by why. With the help of business process mapping, the nation can create easy flow charts and diagrams by defining the factors with several symbols such as circles and arrows, diamonds, and rectangles according to business activities. Based on Mejri, Ghannouchi & Martinho (2016), business process management has focused on enhancing flexibility, variability and developing the growth of access to the opportunity superiorly. According to business process mapping, good group private limited has included sales top warehouse collection clerk and accountant and described the duties accordingly. The cell stops will receive orders from plants with the help of a digital platform and prepare different copies of sales forms.

Sales form copies will be sent to the warehouse staff accountant and collection clerk. After receiving the sales form, the sales staff has focused on packaging and sitting structure with proper items from the warehouse and enclosed the packing procedure. The sales order will be filled by the consumer number. The consumers have been notified if the product is not in stock from the warehouse staff section. According to private limits the warehouse stops are not able to proceed with the sales as there is no particular stock of products, stops will reorder plenty of items for replenishing stocks based on their desired level. As opined by AbdEllatif, Farhan & Shehata (2018), business process mapping has helped to evaluate the factors regarding business development and represent the important solutions regarding organizational development. After that the same staff shift sales order form and has completed a review with the help of an accountant based on customer records and approved by the customer credit points.

Customer credits have approved the sales order and developed two copies of invoices for the customer and collection clerk. After matching the approved sales order, the accountant has filed the consumer number based on their products. The collection clerk has contacted the sales journal after receiving the copy of the invoice based on consumers' orders and posted the sales to accounts receivable ledgers. Besides that, the regular number of cells in the sales journal has been sent to the accountant who has posted the summary of sales to the general ledger. Moreover, the consumer can't pay the number of products by cheque and it has been collected by the collection clerk.

The checking forms from the consumer's section are only collected if those are only for deposit and create records in the accounts receivable ledgers. As per the view of Fleac? & Fleac? (2016), business process mapping structure has helped to analyse organizational development approaches and completed the overview of business growth. The amount of cheque has been recorded in the cash received journal by the collection clerk and the entered information has been deposited through cheque in the bank within a week. The invoices have been paid through electronic banking and receipt has been sent into account receivable and cashbook letters at the end of each week. After summarizing account receivables of a month, ships have been collected from the collection clerk. Chords of the accountant have been summarized by general Ledgers. The account receivables ledgers have been reviewed by accounts in a month and calls have been made to the consumers if the payment of invoices has not been received within three months.

Strengths and weaknesses of the existing system

Strengths

Good group pty ltd has become specialist in developing low-cost home application and maintain a good consumer relationship. In the initial 2 periods, they have experienced sufficient operational inefficiencies and critical accounting errors. They have included sales tab warehouse staff accountant and collection clerk to mitigate conflicts regarding accounting errors in their business organization. By segmenting the entire accounting section and in sales staff warehouse staff accountant and collection card it has become a beneficial perspective for this organization for processing its revenue in each financial year. Cell stop can prepare full copies of the sales order form which has helped to understand the requirements from transaction to the warehouse staff accountant and understand the reliability of organization by consumers. With the help of those sales orders, warehouse staff can usually prepare packing slips with proper items from the stock of the warehouse and shift the items to consumers in a limited time period.

Although if the stock is unable to fulfill the requirements of the consumer section the warehouse staff can notify the consumer through email and sales order as well as replenish the stock according to their desired level. On the other hand, accountant 10 reviews the record of consumers according to the sales order form and approves or disapproves the credit of consumers. The accountant review collection clerk can approve the sales order according to the invoices to the consumer number. Additionally, after obtaining the entire payment through cheque, the collection clerk can deposit the amount of cheque through electronic banking and electronic receipts into the account receivables. Moreover, the accountant has received the summarization of cash receipt of a month from the collection flag which has helped them to understand and review 2 on clarity of payment and they can make phone calls to the consumers for unpaid products within 3 months.

Weakness

There are sufficient strengths for good group private limited in the allocation of employees in their internal accounting section. Allocation of employees in sales staff warehouse staff and accountant and collection clerk can create conflicts in their responsibilities due to the obstacles in accounting errors. According to sales staff, it has become a hard task to prepare copies of cells from forms and send them to warehouse staff, accountants and customers regularly. Moreover, the staff can create challenges for the organization as they can take products from the stock and provide a review of blank stocks. Additionally, the approval of sales orders can create biasing errors as the accountant has reviewed the customer records and approved the products. Without properly reviewing customer records there are higher chances of biasing issues in approval of customer care needs and their products. Decide that if the collection clerk is unable to provide sales journals to account receivable ledgers there can be a delay in summarizing sales amount to the general ledger. On the other hand, payment through cheque can create critical challenges for the good group as the failure of a cheque can be a sufficient delay in obtaining products amount after the definition of consumer requirements. Apart from this, there are several types of consumers, some of them are not willing to pay the payment of their products immediately and there is a chance of inefficient summarizing of Cancer by an accountant and they have to make phone calls to the consumers who had not paid the amount of invoice within 3 months of product celebration.

Ways to improve business process

It is essential to improve the business process by streamlining task factors for improving the efficiency of the organization. Good group private limited has gone through several organizational steps in order to generate a business report for resolving consumer complaints including new clients and developing new products. The process should focus on formal and informal procedures and well-established steps to develop receiving and submitting invoices by developing good relationships with clients. As opined by Sjödin et al. (2021), inclusion of artificial intelligence technique can be highly helpful for transformation of business development and develop new business model capabilities. Improvement of business processes is essential for mitigating numerous problems such as the frustration of colleague duplication of work practice, increment of cost of products, wastage of resources, development of bottlenecks, and complaints from consumer sections regarding product quality and good services. As cited by Estevão, Lopes & Penela (2022), the development of a favourable business environment can be a reason for improving risk factors due to higher chances of error occurrence. For improving the organizational procedure good group private limited should focus on business processing for improving documentation of flowchart and swim lane diagram.

Besides that, swim lane diagrams have developed complexity and superiority regarding the involvement of people. It is essential for a good group to include detailed information of sub-steps by consulting organizational executives properly without overlooking any minor factors. According to Vemuri et al. (2021), with the help of IoT technology, business organizations can enhance the impact of the business environment by analysing the business procedures good group private limited can understand the reason for frustration from the consumer section and which factors of an organization can efficiently create bottlenecks. As reported by Li, Voorneveld & de Koster (2021), forecasting model based on technology development and changes in social perspective has helped business organization during Covid pandemic situation. Moreover, they can understand the reason for the increment of the cost of products and by which steps they can reduce critical problems. Following root cause analysis, causes effect analysis and five wise analyses can be utilized in order to trace the particular problems from the depth of organizational activities and develop fixing problems by analysing the symptoms.

Additionally redesigning the entire business process, they can use new approaches by changing early stages. Identifying brainstorming they can note down the changes and cost factors involved with business understanding. As stated by Chen et al. (2018), information system analysis can be helpful for mitigating risk compliance and developing the factors regarding fundamental benefits. Moreover, risk analysis and impact analysis can be utilized for understanding the failures, and by considering customer experience in mapping the organization can focus on consumer engagement. With the help of acquiring resources and proper resource management, they can develop the communication between HR management and the IT section based on a beneficial perspective. According to Huang et al. (2021), business mapping model of emotional intelligence has become an important weapon for modern developed E-commerce operational activities. Implementation and communication changes in business organizations can be beneficial for the development of organizational growth. Utilizing the change curve and Kotter's 8 step change model can be beneficial for overcoming the resistance regarding implementation and communication changes. Reviewing small improvements regularly can reduce frustrating factors from the consumer section and in monitoring procedure in order to fix critical problems.

New business process model

The organization can develop sustainable business reports in order to resolve complaints from the consumer section and include new clients by developing new products based on the requirements of clients. With the help of formal and informal procedures, they can easily mitigate challenges and conflicts in accounting errors and duplication of work practices. In the new business model, they can maintain a sustainable price for low-cost products in order to maintain a good relationship and develop consumer engagement.

By utilizing organizational flowchart and swim lane diagrams good group private limited can document the organization procedure and reduce the occurrence of accounting error sufficiently. In the new business model, good group private limited can use a risk analysis and impact analysis for understanding the failures and understand the customer experience by developing process mapping. With the help of SWOT analysis and Kotter's analysis, they can understand the changes strengths, and opportunities for organizational growth and reduce the weaknesses and threats from the business practices.

Conclusion

The new business process model has helped organizations to understand and optimize the work practices by developing a visual representation of fruitful business procedures. Its cab be concluded that by evaluating the factors of suggested improvement, good group put ltd cab easily create a new business model for their business growth.

Reference

AbdEllatif, M., Farhan, M. S., & Shehata, N. S. (2018). Overcoming business process reengineering obstacles using ontology-based knowledge map methodology. Future Computing and Informatics Journal, 3(1), 7-28.https://doi.org/10.1016/j.fcij.2017.10.006

Chen, T., Wang, W., Indulska, M., & Sadiq, S. (2018, September). Business process and rule integration approaches-an empirical analysis. In International Conference on Business Process Management (pp. 37-52). Springer, Cham.https://doi.org/10.1016/j.is.2021.101901

Estevão, J., Lopes, J. D., & Penela, D. (2022). The importance of the business environment for the informal economy: Evidence from the Doing Business ranking. Technological Forecasting and Social Change, 174, 121288.https://doi.org/10.1016/j.techfore.2021.121288

Fleac?, E., & Fleac?, B. (2016). The business process management map–an effective means for managing the enterprise value chain. Procedia Technology, 22, 954-960.https://doi.org/10.1016/j.protcy.2016.01.096

Huang, H., Kaigang, Y. I., Kumar, R. L., & Praveena, V. (2021). Category theory-based emotional intelligence mapping model for consumer-E-business to improve E-commerce. Aggression and Violent Behavior, 101631.https://doi.org/10.1016/j.avb.2021.101631

Joshi, A., Benitez, J., Huygh, T., Ruiz, L., & De Haes, S. (2021). Impact of IT governance process capability on business performance: Theory and empirical evidence. Decision Support Systems, 113668.https://doi.org/10.1016/j.dss.2021.113668

Li, X., Voorneveld, M., & de Koster, R. (2021). Business Transformation in an Age of Turbulence-Lessons Learned from COVID-19. Technological Forecasting and Social Change, 121452.https://doi.org/10.1016/j.techfore.2021.121452

Mejri, A., Ghannouchi, S. A., & Martinho, R. (2016). Representing business process flexibility using concept maps. Procedia Computer Science, 100, 1260-1268.https://doi.org/10.1016/j.procs.2016.09.164

Sarasini, S., & Langeland, O. (2021). Business model innovation as a process for transforming user mobility practices. Environmental Innovation and Societal Transitions, 39, 229-248.https://doi.org/10.1016/j.eist.2021.04.005

Sjödin, D., Parida, V., Palmié, M., & Wincent, J. (2021). How AI capabilities enable business model innovation: Scaling AI through co-evolutionary processes and feedback loops. Journal of Business Research, 134, 574-587.https://doi.org/10.1016/j.jbusres.2021.05.009

Vemuri, V. P., Naik, V. R., Chaudhary, V., RameshBabu, K., & Mengstie, M. (2021). Analyzing the use of internet of things (IoT) in artificial intelligence and its impact on business environment. Materials Today: Proceedings.https://doi.org/10.1016/j.matpr.2021.11.264

HI6025 Accounting Theory and Current Issues Assignment Sample

Assignment Brief

Purpose of the assessment (with ULO Mapping)

This is a group assignment. Students are required to conduct research and analysis of a theoretical financial reporting issue and present their findings in a written report. Students will have to do research on relevant literature and demonstrate understanding and critical evaluation of key disclosure issues relating to the application of specific accounting standards

Weight - 40 % of the total assessments

Total Marks - 40

Word limit - 3,000 words ± 500 words

Assignment submission: Final Submission of Group Assignment: Week 10,

Wednesday, May 26th 2021, at 11:59 pm

.

Late submission incurs penalties of five (5) % of the assessment per calendar day unless Student Services of your campus have granted an extension and/or special consideration before the assessment deadline. Submission Guidelines All work must be submitted on Blackboard by the due date, along with a completed

The assignment must be in MS Word format, with no spacing, 12-pt Arial font and 2 cm margins on all four sides of your page with appropriate section headings and page numbers.

Reference sources must be cited in the text of the report and listed appropriately at the end in a reference list using Harvard referencing style.

Assignment Specifications for assignment help

Part A

The corporate disclosure practice will help all the stakeholders to understand and measure business operation. Annual financial statement and particularly income statement is one of the most important ones. However, a company's reported profits will be impacted by different factors, including when particular transactions and events are recognized and how such transactions and events are measured.

Requirement:

1) Using earning management concept, discuss why the timing of recognizing events that impact income, revenue or profit or expenses are important for managers?

"Maximum 1000 words."

Part B

ABC Ltd has incorporated a bonus plan that rewards the board of directors (executive members) by providing a bonus of 3 per cent of reported profits. This is an Accounting-based incentive that has the advantage which the accounting results may be based on subunit or divisional performance.

"A well-informed labour market will motivate management to work to maximize the value of its firm. Underperformance might lead to dismissal and, if the labour market is efficient in disseminating data, a 'failed' manager might have difficulty attracting a position with comparable pay elsewhere." (Deegan, 2020)

Requirement:

1) Using Positive Accounting Theory (PAT), discuss the bonus theme in general and why the bonus plan (Accounting-based) was put in place in ABC Ltd?

2) Explain whether the board of directors could be motivated to try to inflate reported profits.

3) Use the opportunistic perspective of PAT to explain the potential for managers to manipulate corporate disclosure.

"Maximum 2000 words."

Assignment Structure:

Assignment Cover page clearly stating your name(s) and student number(s)

Group's Assignment Task Allocation table (except for Solo group members)

Table of Content

Body of the assignment with appropriate section headings

List of references

Solution

Introduction

This report would be focused on the assessment of earning management concept using which the importance of recognizing the events that impacts revenue would be assessed. It would also discuss the bonus theme in general and why bonus plan was put in place in ABC ltd. It would further explain whether the board of directors could be motivated to inflate the reported profits. The opportunistic perspective of PAT would also be explained through this report. It would end with a conclusion summarizing the findings of the report.

Part A

Why the timing of recognising events that impact income, revenue or profit or expenses.

Earnings management is a technique used by businesses in order to produce a positive financial statement of business through assessment of financial position. Many accounting principles and rules requires the management to male decision based on the financial positioning of business. It takes advantage of the guidelines produced by businesses in order to create financial statement and inflate smooth earnings of the company (Rachmawati, 2019, pp.133-142(4)).

So, in accounting earnings management refers to the manipulation of financial statement in order to make it appear good in the eyes of investors. It is especially used by the companies in order to make the financial position appear smooth functioning. One of the most popular way to tamper the financial record is to use an accounting policy that creates short term earnings for the business.

Revenue recognition principle is an important part of the events management technique which helps in recording the timing in which the revenue of the company is generated and recognized in the financial statement of business. Theoretically, there are several times within a year in which revenue can be recognized. Technically, the earlier a revenue is recorded, the more valuable it is considered for the business (Aladwan, 2019, pp.691-707(2)).

In accounting, revenue recognition is one of the many areas that remains vulnerable to internal manipulation and bias. In fact, it has been estimated that many of accounting fraud taking place within the company arises from issues in revenue recognition, given the low amount of judgement involved in the process. Hence, it is critical for management to understand the different techniques of revenue recognition while analysing the financial statement. There are several criterions for recognizing the revenue of business some of which are as follows:

• There remains an inevitable risk of transfer an ownership reward

• The seller ultimately loses control from the managerial accounting of the sold

• The revenue amount can be effectively quantified

• The payment collection period is assured reasonably

• The incurred cost can be effectively measured (Hatane et al., pp. 196(5)).

Revenue recognition After and Before Delivery

In case of goods sales, IFRS does not allow the company to recognize the revenue until the delivery has taken place. It does allow to record the revenue after the delivery has taken place. There may be situation that makes it uncertain to determine the cost relating to future costs which in turn violates the fifth aspect of revenue recognition stated above.

For instance, if a company fails to project the future cost of the product, the above criteria would not be met. When the fifth criteria are satisfied, the company can effectively recognize the revenue. There are other reasons as well which requires the company to recognize the revenue after delivery. Once such reason includes the inability of company to reasonably estimate the amount of income and unassured collectability of accounts receivable and ownership risks with the sellers (Kaya, 2017, pp -140(2)).

Revenue Recognition for Service Provision

One is which needs special focus while determining the accounting treatment includes the contract of construction. These contracts are especially designed for asset construction or a combination of assets such as large ship and building that is usually used for several years to come. When the business is required to document revenue obtained from service, IFRS usually directs that the business must document in accordance with the rate of completion and the method of computing the completion method (Schroeder, Clark and Cathey, 2019, pp -230(7)).

Then contracts are usually of two times which are cost plus and fixed price contracts.

In case of fixed price contracts, the contractor usually agrees on paying the price before the actual beginning of construction activity. In this way, all risks are transferred to the contractor. On the other hand, in case of cost-plus contracts, the actual price depends on the hours being spent on completion of contract plus the margin of income. For businesses operating under ASPE, the completed contract method can also be used in the place. Unlike the method of completion, completed contract method would only be recognized when the contract actually is complete.

Further, the expense recognition period is another way using which the company can follow guidelines to record their financial items. As per the principle, the companies are only directly to document expense at the same time as the revenue. If this method is not followed, then expense would end up getting recognized when it is incurred which might end by being fore the actual recognition of revenue (Scott and Scott, 2015, pp -49(5)).

This principal also impacts the income tax timing. However, there are some expenses which are difficult to be related with the revenue some of which are rent, salaries and utilities. These rents are usually referred to as period cost and are generally recognized in the period in which they are incurred.

The method of expense recognition is a primary process in accrual basis of accounting which states that revenue can only be incurred when they are earned, and expenses are recognized when they are consumed. If a business practices recognizing expense during the period it pays to the supplier, then it is termed as cash basis of accounting.

So, how we can understand how the concept of timing is critical when it comes to recognizing the income and expenses. It provides a systematic approach which can be used by the business to record its financial items in the most accurate and systematic way thereby reducing the chances of incurring loss through operation and successfully gaining the confidence of the stakeholders on the performance of the business (Zhou, 2019, pp.115(2)).

Bart B

Positive Accounting Theory

PAT tries to make good prediction of real-world events and translate them into accounting transaction. While other accounting theory would usually direct as to what should be done, PAT tries to evaluate and predict those transactions. PAT helps in determining as to which accounting policy must be chosen by a firm and how would it react to the newly implemented accounting standards. The overall intention of PAT theory is to determine the impact of the accounting theory that has been implemented within the company and how it differs in every firm. It recognizes that economic consequences exist. Under this system, firms usually want to ensure that they survive for the longest period of time and can effectively create long term value in the process. Firms are often seen as a collection of contracts that they have gotten into. When it comes to PAT, because firms want to be highly efficient, they would always look out for ways to reduce cost while maximizing income in the process. Hence, in this target, they would always try to adopt an accounting policy that would help in cost minimization. PAT understands that with changing market circumstance, companies also need to be flexible with their accounting standard (Suleiman, 2017, pp.1-3(1)).

With this in mind, an optimal set of accounting theory lays between contract costs and providing flexibility in times of changing circumstances. There are currently three hypotheses of Positive accounting theory.

Bonus Plan Hypothesis: Managers of firms operating with bonus plan would usually try to shift their reported earnings from future period to the current period. By doing so, they can generate more bonus for themselves.

Debt Covenant Hypothesis: The closer a firm is to breaching the accounting base covenants of debt, the higher would be the chances of managers trying to shift the reported earnings from future to current period. This is due to the fact, that by increasing the current earnings, the company is less likely to violate the rule of covenants of debts and management can then minimize their constraints in running the company.

Political Hypothesis: The higher the cost faced by the firm, the more likely would be the manager in choosing an accounting process that would shift the earning revenue from current to future period. Further, high profitability can often lead to political conflict within the country, and which can lead to higher tax payments (Ward and James, 2015, p.143(2)).

Bonus is the pay that the company pays to its employees in addition to the base salary. This strategy is used by several organization as a way to acknowledge the hard work and dedication of the employees and their contribution to the company. It is also used to boost the morale of employees. When a company attaches bonus with the base pay of employee, it encourages them to work harder to reach its objectives and ensure that the business is taking all the right action in order to reach objectives and take the company to new heights of success. There are several benefits of paying bonus to the employee some of which are as follows:

• Boosting morale of employees

• Making the workforce reach objectives within a specified deadline.

• Enabling the company to increase their chances of generating higher revenue

• Reducing staff turnover rate (Roden, Cox and Kim, 2016, pp.80 (3)).

• Ensuring maximum work satisfaction.

As can be noted from the task case study in the assignment, ABC limited has adopted a bonus strategy as per which all the board of directors would be paid within 3% of the reported profit.

The general question that should arise here is whether a bonus plan is really that effective in encouraging the employees to work hard within the company. The straight answer to this question would be when the company makes the right investment strategy, it automatically leads to healthy working environment, which in turn enables the firm to generate higher income for the future. Recent studies have shown that companies working with bonus has higher chances of success compared to those without any effective bonus plan in place (Ausloos, Cerqueti and Mir, 2017, pp.238(6)).

So, based on these assumptions, ABC ltd have adopted the strategy in order to ensure that the directors are working productively and are able to generate significant wealth over time which can be utilized by the company in order to expand brand image and ensure that the company is following a strict protocol. In order to understand the efficiency of a bonus system it is critical that the business is able to compare the performance of the firm with the time it did not have any effective bonus strategy in place.

There are several advantages of having a bonus plan in place and hence ABC ltd is encourage to utilize the strategy in the upcoming years as well (Lin, 2016, p.1253(1)).

Can Board of Director inflate the Revenue

Earning manipulation is easy when directors hold too much power over the business. In order to increase bonus payment, directors would want to inflate the net income of the business. Additionally, the net income would also be boosted when they want to attract higher stakeholders within the business. These inflated earnings would make the business look more profitable while in reality the picture would be much different. First, let’s analyses the ways in which board can inflate the earnings of business:

• Accruing fictitious income from year-to-year income.

• Documenting the sales of the products that have not been shipped.

• Selling the product at inflated price to related parties

• Documenting the revenue in present year that would be generated in the next year.

• Documenting shipments to resellers that are not profitable and hence not a viable income option.

• Accruing projected sales that have not really taken place (Shakeel and Srivastava., pp.110(2)0.

• Intentionally tampering with allowance of receivables.

In an attempt to boost the bonus, pay, board of director can take several measures including:

• Playing around with Expenses: Board would deliberately try to high the expenses in order to inflate the income of the business or

• When they record the expenses in the income statement, they would try to convince to the readers, that even though they have incurred expense, but it would not impact the overall profit of business (Yisha, 2020, pp.125 (8)).

• There are often instances where the board of director have shown profit in the business when they are actually incurring huge amount of loss. In some cases, companies reflect profit when they are generating no profit. In some cases, investors have shown profit on investment even when investors cannot make any sense of that profit. In some cases, companies reflected profit in P/L but were able to convince that even when there are losses, the income statement does not get affected.

• In some cases, directors have also chosen the way of reflecting loss at the last resort when there is no option left.

• They can also not spend on areas that needs immediate attention in order to preserve the capital and inflate the performance of business in return.

• They also change accounting profit whenever necessary in order to inflate the income of business (Sa Vinhas and Heide, 2015, pp.165(2)).

The directors cannot inflate the profit of business in order to suit their best interest and ensure that the company is generating significant amount of profit. Directors can manipulate the data only when they have their best interest in mind and when they hold significant decision-making power over the business. Additionally, the income of the business cannot be manipulated by directors unless stated by the owner of the company or when it is done in the best interest of the company. If under any circumstance, the business fails to identify the manipulation taking place within the organization, it would then have to take legal action against such practices

This is a major disadvantage of having bonus attached to the business. The business would also need to ensure that the company is free from such practices in order to generate maximum benefit and produce reliable result which can be used to generate wealth overtime. The company would also need to understand how these manipulations can harm the brand value in the long run. So, even though bonus is a great way to improve efficiency, it can also result in increased manipulation of data in order to get higher bonus and in turn the directors would try to show inflated profit in the financial statement even in reality the performance is much different. Hence, directors are never given the power to change the statement of the financial statement and work in their best interest (Coutinho, Sancovschi and dos Santos, 2019, pp.250-381(3)).

Use the opportunistic perspective of PAT

The opportunities perspective suggests that when a manager works for a business, he would always have his best interest in mind and would therefore try to manipulate data in a way that would increase his gain in the process. They only adopt accounting policies that allow them to maximize their gains when the firm also gains. There are different types of hypothesis in existence such as bonus plan, political cots and debt hypothesis that show motives makes manager choose an accounting method over another (Yisha, 2020, pp.271(5)).

There are several ways in which the manager can manipulate the data of business. One major reason that leads to manipulation is the increased conflict between the accounting firm and the audit them. Manipulation would always involve steps that would make the manager takes steps that would go against the wish of the company. This in turn would impact the brand value and in turn would also make the company vulnerable to market risk.

Discussed below are some ways in which the accounting data is manipulated by managers to suit their best interest.

• Recording the revenue before suppling the goods and services to the customers.

• Reporting income from investment while using that income to cover for the loan.

• Capitalizing the business expenses, thus shifting them from income statement to the balance sheet (Rachmawati, 2019, pp.133-142(1)).

• Inaccurately reporting the liability or neglecting them all together.

Most common way of manipulating the data is by inflating the value of asset with false count. For instance, a company may have ordinary account of inventory but add 100 items to each count. Hence, investors are advised to cushion themselves from such fraudulence activity and would protect the company from bias. The best way to protect against such manipulation would be to obtain effective financial education. The investors must understand how to read and interpret three aspects of financial statement including income statement, cash flow statement and balance sheet of the company. The company would also need to continue using the company to come up with effective strategy that would prevent its employees from manipulating the data and ensuring that the business is always moving forward in the right direction. Also, it is critical to understand that managers would commit to suit their best interest in the company and would only be productive if only it has some selfish motive attached with it. It would also ensure that the company would be using the company’s financial report in order to come up with the most reliable report which can be used to make investment decision (Aladwan, 2019, pp.691-707(2)).

Financial statement can never be fully protected from manipulation and hence there are effective legal action in place to effectively punish the companies taking part in such practices and putting the reputation of brand at stakes. The company would also need to understand that the manipulation of financial statement is an inevitable part of financial statement and hence the owners need to be more more careful while making decision. This is a major reason why companies choose to get their financial statement prepared by third party auditors who do not only ensure lowest possible error but also increases the reliability on the operations (Hatane et al., pp. 197(3)).

Conclusion

To conclude, earning management is a tool which companies uses to manipulate the data of company to make it look more appealing to the investors. The investors become victim of false information and can incur huge loss as the managers of business work on their best interest and thinking about shareholder’s wealth maximization becomes their last priority. Further, the bonus hypnosis indicates that the managers would always try to shift future revenue to current period in order to generate higher revenue.

References

Aladwan, M., (2019). Accrual Based and Real Earning Management Association with Dividends Policy “The Case of Jordan”. Italian Journal of Pure and Applied Mathematics, pp.691-707.

Ausloos, M., Cerqueti, R. and Mir, T.A., (2017). Data science for assessing possible tax income manipulation: The case of Italy. Chaos, Solitons & Fractals, 104, pp.238-256.

Coutinho, A.H., Sancovschi, M. and dos Santos, A.G.C., 2019. The opportunistic approach of the Positive Accounting Theory (PAT) fails to explain choices made at OGX: An anomalous situation? Revista de Contabilidade e Organizações, 13, pp. e164412-e164412.

Hatane, S.E., Pranoto, A.N., Tarigan, J., Susilo, J.A. and Christianto, A.J., (2021). The CSR Performance and Earning Management Practice on the Market Value of Conventional Banks in Indonesia. In Global Challenges and Strategic Disruptors in Asian Businesses and Economies (pp. 196-213). IGI Global.

Kaya, ?., (2017). Accounting choices in corporate financial reporting: A literature review of positive accounting theory. Accounting and Corporate Reporting-Today and Tomorrow.

Lin, T.C., (2016). The new market manipulation. Emory LJ, 66, p.1253.

Rachmawati, S., 2019. Company Size Moderates the Effect of Real Earning Management and Accrual Earning Management on Value Relevance. Ethics: Journal of Economics, 18(1), pp.133-142.

Roden, D.M., Cox, S.R. and Kim, J.Y., (2016). The fraud triangle as a predictor of corporate fraud. Academy of Accounting and Financial Studies Journal, 20(1), p.80.

Sa Vinhas, A. and Heide, J.B., (2015). Forms of competition and outcomes in dual distribution channels: The distributor’s perspective. Marketing Science, 34(1), pp.160-175.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., (2019). Financial accounting theory and analysis: text and cases. John Wiley & Sons.

Scott, W.R. and Scott, W.R., (2015). Financial accounting theory. Pearson Canada Inc.

Shakeel, M. and Srivastava, B., A Study on High-Frequency Financial Data Manipulation and Visualisation.

Suleiman, S., (2017). Debt Contracting and Conditional Accounting Conservatism. International Journal of Accounting Research, 5(1), pp.1-3.

Ward, T.J. and James, K.L., (2015). Student participation and performance in a graduate accounting theory class. Academy of Educational Leadership Journal, 19(2), p.143.

Yisha, M., 2020. Analysis on Efficiency and Opportunistic Perspective under the Pat. The Frontiers of Society, Science and Technology, 2(17).

Zhou, Y., 2019. A Concept Tree of Accounting Theory:(Re) Design for the Curriculum Development. Education Sciences, 9(2), p.111.

ACCT6007 Financial Accounting Theory and Practice Assignment Sample

Assignment Brief

Length - 1500 words +/- 10%

Learning Outcomes

a) Explain the relationship between accounting theory, the accounting conceptual framework and accounting standards.

b) Work individually and in groups to identify and apply appropriate accounting standards to a range of authentic accounting scenarios.

Submission - Week 9 Sunday midnight (AEST)

Weighting - 25%

Total Marks - 100 marks

Context:

This assignment develops research and critical thinking abilities. It is a critical analysis/review of an academic article. Changes in technology are impacting accounting and how accountants perform their jobs. This activity will provide students information on new trends in accounting field.

Instructions:

Download and critically analyze an academic article written by Jun Dai and Miklos. A. Vasarhelyi. This article can be found in the Torrens University library using the following citation:

Dai, J. & Vasarhelyi, M.A. (2017 Toward Block Chain-Based Accounting and Assurance. Journal of

Information Systems Vol. 31 No. 3, p5-21,

https://torrens.idm.oclc.org/login?url=http://search.ebscohost.com/login.aspx?direct=true&db=bsu

&AN=126177472&site=ehost-live

You may use an essay format or any other acceptable academic format for critical review. Use APA 7

referencing style guide. Use minimum 10 academic references.

Answer the following questions for assignment help during your analysis.

1. Discuss the three phases of block chain technology? What is the potential use of block chain technology in accounting?

2. The author discusses Triple Entry Accounting. What is your understanding of the concept?

3. Do you agree or disagree with any arguments made by the author? Explain your point of view and provide evidence in support of your point of views from other academic resources.

4. Critically review any potential issues or problems with block chain technology being used in accounting.

To answer all the above questions: Review the article provided and search for related academic journal articles. Use minimum 10 academic references.

Academic skills resources: Analyzing the Brief, Essay Writing, and Critical Thinking

These resources can be downloaded from LASU - Learning and Academic Skills Unit on Blackboard

following the link: https://laureate-au.blackboard.com/webapps/blackboard/content/listContent.jsp course_id=_20163_1&content_id=_2498849_1

Solution

Introduction

In the prevailing study, the new technology of block chain for accounting and assurance is been critically evaluated. The relationship between the accounting conceptual framework, accounting theory, and accounting standards is been done. The three phases of block chain technology, potential uses of same, potential issues and challenges of block chain and also argument regarding its challenges is provided in the below study. Further the triple entry system of accounting is been critically evaluated below. The reason why it was introduced, its application in the current system and interconnectedness with the block chain technology is provided. Also the research is done in context of this new technology impact on the current accounting and assurance system.

Main Analysis

Three phases of block chain technology

Since 2009 the evolution of block chain technology gone through three stages. Firstly, block chain 1.0, which purely focused on the crypto currency trading. The function of remittance, digital money transfers also its comprised internet of money- a new payment ecosystem. Secondly, block chain 2.0 which also involves same trading but this time with the broader scope of financial applications. These applications include smart property, derivatives and digital asset ownership etc. (Banafa, 2020) This phase expanded the simple digital currency platform into the platform of wide variety of digital products with the help of new application that is smart contracts. These smart contracts automatically execute, verify and enforce the terms of the contracts operating on block chain. The terms and conditions agreed by various trading parties are encoded through the smart contracts. Further these smart contracts execute the tasks which were pre- specified automatically and settle the contract by examining the changes in conditions with relation to the contracts’ embedded rules. The last phase, block chain 3.0 was the further expansion of block chain2.0 system. This expansion was beyond the business and financial applications. This includes voting system, products related to cloud storage, attestation services, even the government administration transformation (Umarovich, et al, 2017). Through this version the administration of government could also be dramatically transformed into the decentralized monitoring tools and self-management.

Potential uses of block chain

• The first and foremost potential of use of the block chain is that, it could be used in transformation of auditing process into more precise and timely automatic assurance system.

• The block chain technology for accounting could re- conceive corporate accounting

• It is considered as a new kind of data base which has the potential to play role in ERP as accounting module.

• Also could be used as conjunction for the existing accounting system

Triple entry accounting

The concept of triple entry account is been observed and discussed by various professionals and academics since years (Ravi, 2020). The primitive mechanism was of single entry book keeping transaction under which there were high chances of risks and fraud apart from being simple and effective, it was difficult to get repaired and track. In order to overcome these issues double entry system was introduced. This system was quite efficient and rapidly enables the conformation that whether the transaction recorded is correctly or not. This introduction helped in minimizing the human transactional errors but was unable to provide sufficient assurance to the high level companies regarding their financial statements. Therefore, in order to overcome this issue of assurance the triple entry accounting system was introduced. It was proposed to get utilize as independent paradigm also a secure one. This helped in improving the reliability of various companies on their financial statements (Zhang et al, 2020). Originally this system included or it could be said that it requires the neutral intermediary in its transaction recording process with each of the party. So there was involvement of three parties those are two of the parties which are involved in the transaction and one intermediary, this resulted in total three entries. However, the intermediary required under this triple entry system must be reliable and independent in order to verify each party transaction (Block, 2020). In addition to this the entries stored by the middle person are highly exposed to risk, or unauthorized changes due to cyber-attack. But the new launched technology of black chain has the potential to mitigate these cyber-attack risks and improve the mechanism of triple entry system. This technology could play the role of intermediary by automating and distributing the storage, providing secure platform for transaction, verifying the entire process and prevent the transaction from getting tampered.

Disagreeing on the argument

That block chain-based assurance and accounting methodology would provide verifiable information disclosure, real-time, and progressively automated assurance

Undoubtedly the above argument is true but is not acceptable as the block chain technology comes with various limitations and drawbacks though. The goal of the author was to discuss regarding the impact of block chain technology on accounting and assurance profession, but it has although many drawbacks. This technology is rapidly getting developed and emerged due to which various new approaches and algorithms are been introduced in the application of accounting and assurance. So these algorithms are needed to be expanded due to the rapid growth of such technology and are required to be reconsidered. Further the author has only discussed about the impact and role of such technology on the profession of accounting and assurance which it plays. The challenges such as in the areas of government auditing, corporate auditing need further identification and re-thinking. As the regulatory frame work of block is is decentralized, which means there’s no one power to enforce law and order in the network no leaders, no moderators (ALI, 2021). Also the concept of triple entry system under this is not acceptable in such a rapidly changing world; the adaption of such might just be an adaption to the advanced world. Unfortunately, the operation of this new tech technology needs computation resources and sufficient storage. The placing of such a lengthy corporate data would be extremely expensive and potentially demanding for the computation of current commercials (Schifrin, 2019). Such requirements of the technology could eventually impede the popularization of this technology especially for the medium and small term firms. Even also the large enterprises might refuse the usage of such technology if they had significant issues from the performance and efficiency of current system operations. Thereby I disagree with the argument of author on the benefits of this block chain technology as it has several drawbacks and would most probably rejected from being used.

Potential issues with block chain technology in accounting are-

Security and transparency related issues are the potential problems associated with the block chain technology (Tochen, 2019). The block chain technology is secure as secure the weakest links are. For instance, if one party wants to access the data within the block chain they could only access one node of it. That means the block chain is easiest to hack, hence there is huge threat to the entries embedded in it. That is not the only risk with it, but also it is possible to get exposed in fraudulent practices for the approved transactions. The poof of identity, proof of stake both are at risk, as anyone could easily get access in the block chains. The existing accounting standard in the technology could further be adapted increasingly for more transparent and verifiable accounting ecosystem (Hastig & Sodhi, 2020). The role of auditors also in the new accounting system is required to be re-through and the reengineering of currents audit paradigm is required.

In addition to this, one important issue that is worth careful consideration is the scope of participants in the block chain based accounting ecosystem. This especially occurs in the case when the verification of transactions or creation and validation of smart contract is there. The black chain technology for the accounting system is a permission block chain in which only the transaction of the companies can be submitted into the block chain ledger, with the verification function being restricted to accountants, management, and auditors (Orcutt, 2018). Also substantial security and cyber-attacks knowledge is highly required by the block chain technology algorithms and its operating paradigms. For such challenges the managers and accountants are required to get the training from the IT professionals, which is necessary to use such technology effectively and correctly. Further to participate in the implementation and designing of the smart contracts the training is required by these parties.

Conclusion

From the above study of critical evaluation on the block chain technology it could be concluded that the technology has several potential uses and merits. Such as, it could be used for re- conceiving corporate accounting, could make the present accounting system more precise and accurate. Further it could be noticed that the technology was evolved through three major phases and also the introduction and concept of triple entry system is understood briefly above. But apart from these potential uses, this technology also contains various limitations or drawbacks with it application. Such as it requires sufficient space, it is quite expensive; also some of the shortcomings are noticed in terms of cyber security and transparency of this technology. Thereby, it could be said that the technology has more shortcomings than the uses.

References

Ali, F., 2021 (Online) The Top 5 Problems with Block chain Technology. Retrieved from <https://www.makeuseof.com/problems-with-blockchain-technology/> .

Banafa, A. (2020). Block chain technology and applications (Ser. River publishers series in security and digital forensics). River. Retrieved November 13, 2021, https://lesa.on.worldcat.org/v2/oclc/1224527152

Block, D. A. (2020). Output management technology: the missing link in the information delivery chain. Computer Technology Review, 40-43, 40–43.https://lesa.on.worldcat.org/v2/oclc/5321867264

Dai, J. & Vasarhelyi, M.A. (2017 Toward Block chain-Based Accounting and Assurance. Journal of Information Systems Vol. 31 No. 3, p5-21, https://lesa.on.worldcat.org/v2/oclc/7286844609

Hastig, G. M., & Sodhi, M. M. S. (2020). Block chain for supply chain traceability: business requirements and critical success factors. Production and Operations Management, 29(4), 935–954. https://doi.org/10.1111/poms.13147

Orcutt, M. (2018). Block chain. Mit Technology Review, 121(3), 18.https://lesa.on.worldcat.org/v2/oclc/7613275795

Ravi, S. (2020). Block chain technology & its use in banking sector. Business World, (oct 26, 2020). https://lesa.on.worldcat.org/v2/oclc/8685801874

Schifrin, M. (2019). Block chain 50. Forbes, 202(3), 86–86. https://lesa.on.worldcat.org/v2/oclc/8094358989

Tochen, D. (2019). Block chain technology: a solution in search of a problem-or a revolution? The Brief, 49(1), 50–56. https://lesa.on.worldcat.org/v2/oclc/8531105397

Umarovich, A. A., Gennadyevna, V. N., Vladimirovna, A. O., & Alexandrovich, S. R. (2017). Block chain and financial controlling in the system of technological provision of large corporations' economic security. European Research Studies, 20(3b), 3–12. https://lesa.on.worldcat.org/v2/oclc/7146245319

Zhang, L., Xie, Y., Zheng, Y., Xue, W., Zheng, X., & Xu, X. (2020). The challenges and countermeasures of blockchain in finance and economics. Systems Research and Behavioral Science, 37(4), 691–698. https://doi.org/10.1002/sres.2710

ACG508 Accounting Standards, Application and Disclosure Assignment Sample

Length: Multiple Xero Reports and 800 words

Group Assessment: No

Submission method options: Alternative submission method

TASK

Assessment conditions: This is an individual assessment task (not a group assessment task).

This assignment requires you to use Xero accounting .

You must complete your assignment within this prescribed period. As Xero is a cloud-based accounting system, you will need an internet connection to use the system.

The assignment has been designed to enable you to complete the assessment within the 30 day period. You are urged to set up your date.

Part A: Xero

You are the accountant for HOSS, a company that commenced in 2020 to provide home office styling solutions for employees working from home. Clients include individuals and Corporates wishing to provide safe and secure home office solutions. While the initial demand for the services stemmed from the requirement to work from home during the pandemic demand for the service has not declined with many businesses offering flexible employment options post pandemic. Up to this time, the accounting work has been completed using a manual system based on spreadsheets. However, with the future looking bright and more clients enquiring about the service, in particular the systems security and occupational health and safety services provided as part of the service to clients you have investigated other options. Your recommendation is that HOSS transition from their existing manual accounting system to a cloud based computerised accounting system for the financial year ended 30 June 2022 to achieve

better management and growth of the business.

It is now June 2022 and you are transitioning HOSS’s existing accounting records from their manual accounting system to Xero and recording the June transactions so that the financials for the year ended 30 June 2022 can be prepared using the computerised system. Additional information required for the completion of your assessment task will be provided to you in yourInteract Site under Assessment Resources / Assessment Item 2. This includes details for each part of the assessment including; set up instructions; the opening trial balance at 31 May 2022; June transactions; and any year-end adjustments. You will be required to export the Balance Sheet, Profit and Loss and the General ledger accounts at 30 June 2022 which you have prepared in Xero and amalgamate into a single Excel file. Failure to download and submit material from Xero will be counted as a non-submission for that component of the task. It is your responsibility to ensure all required components have been extracted from the Xero cloud computing system and submitted as part of your assessment.

Part B:

Based on the reports you generated in Part A above, prepare a report (maximum of 800 words) to HOSS providing a high-level analysis of the financial position, financial performance, and overall financial health of the business. Your report should include justification for the accounting treatment you have chosen for the property, plant and equipment purchased in the current financial year and all calculations you have performed. You are encouraged to draw upon your knowledge from prior subjects regarding financial statement analysis and financial statement ratios.

RATIONALE

This assessment task will assess the following learning outcome/s:

• be able to apply professional judgement in the preparation of financial statements for reporting entities in accordance with relevant ethical, professional and statutory reporting requirements.

• be able to apply and analyse generally accepted accounting principles and specific financial reporting standards relating to concepts of recognition, measurement, disclosure, revaluation and impairment of key financial statement elements.

• be able to critically analyse and communicate clearly and concisely the relevant principles and accounting standards to a diverse audience. The report to your client needs to be professionally presented, at a level appropriate to send to a paying client. This includes:

• The reports generated from Xero need to be presented in a consistent manner and easy to read.

• Headings and subheadings must be used for your recommendations and each of the Xero reports you have generated.

• Use of a standard font, such as Times New Roman, Calibri or Arial font, with a font size 11 or more.

• Suitable margins for your recommendation, being a minimum of 2cm from all sides (left, right, top and bottom).

Requirements for Assignment Help

APA must be used to reference all the sources you have used for your assignment. The CSU Library site provides an online guide to APA (7th ed.) referencing. This is the referencing style adopted by the School of Accounting and Finance. The guide can be found at: http://student.csu.edu.au/study/referencing-at-csu.

Review the rules regarding plagiarism, and if you are not sure contact your lecturer or student learning skills advisor for advice. There is no excuse for presenting the work of others as your own; this includes cutting and pasting material from the web without properly referencing the source.

Solution

Introduction

The aim of this report is to evaluate the performance of 11712399-Jency rameshbhai patel, over the time frame 1st June 2022 to 30th June 2022. The analyst has considered financial statements such as balance sheet and income statement to evaluate their performance. Accounting ratio represents relations that exist between various items appearing in record books such as balance sheet and profit and loss account. Here, the analyst has used ratio analysis method to evaluate the performance of the company.

Part A: Analysis

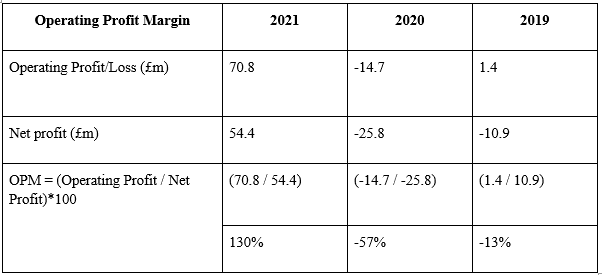

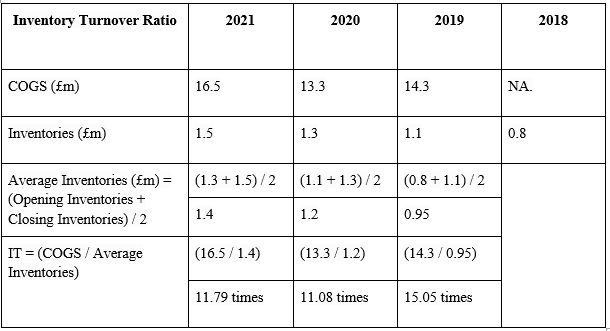

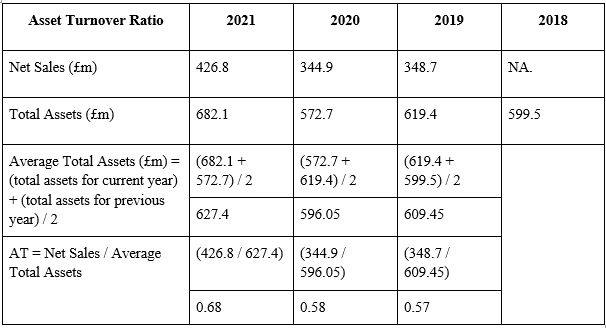

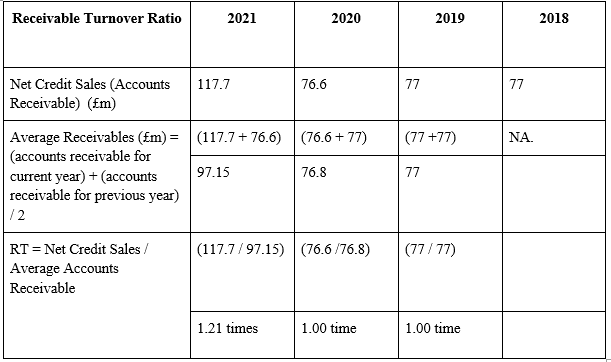

.png)

Part B: Discussion

The gross profit margin on income of a company is represented by the gross profit ratio. A larger gross profit % indicates that the company's financial situation is steady, and they can easily cover their operating expenditures. The Gross Profit Ratio is computed by taking gross profit by operating sales and multiplying the quantity by 100. A proportion illustrates the connection between gross profit and net earnings from operations. This percentage indicates the enterprise's price strategy and effectiveness in direct trade operations. The gross profit is 94.625 percent, indicating that the company is doing well in terms of gross profit.

The net profit margin on sales is represented by the net profit ratio. It is a percentage that illustrates the ratio between net profit and net sales. A bigger profit margin shows that a company's operations are more profitable and efficient. We may deduce from this ratio how firms set their expenditures and pricing to maximise profit. The net profit is 41.39 percent in this case, indicating that the company is doing well.

The amount of an organization's yearly return or net income divided by the sum of the entire shareholders' equity stated in percentage is called return on equity (ROE). It is one of the most important factors that prospective investors consider when deciding whether or not to invest in a business. ROE may be used to determine if a company has the capacity to transform its shareholders' money into profit.

The operating return on capital (ORC) is a metric that quantifies how much money an organisation makes on its capital. To make money, one might look at how successfully the organisation generates cash flow. Divide the Net Operating Margin by the invested capital to get the Operational Return on Capital Employed (Zavadskas, et al., 2018). The return on capital employed (ROCE) of a corporation reveals if it is doing a good job of producing profits from its capital. The ideal ratio is ideally equal to or more than 2%. If the rate is less than 2%, investors will be discouraged.

Conclusion

It can be concluded from the income statement and balance sheet of 11713299- Jency rameshbhai patel that the firm performed well in June 2022. They have also provided proof of 100% accounts receivable for the prior month. The current ratio was also found to be 1.25, indicating that the company has enough liquid cash to cover its short-term commitments.

ACC601 Introduction To Financial Accounting Assignment Sample

Assignment Brief

Individual/Group Individual

Length 1500 words (+/- 10%)

Learning Outcomes:

The Subject Learning Outcomes demonstrated by successful completion of the task below include:

a) Articulate and implement regulatory and ethical frameworks and the use of accounting information to support business decision-making.

b) Apply the accounting cycle and double entry accounting principles to process transactions.

Assessment Task

There are two parts to this assessment. Firstly, Part A, requires you to write a business letter with suggestions on how to address the ethical issues discussed in a case scenario. Secondly, Part B requires you to process accounting transactions using Xero (cloud-based accounting software) and prepares a reflection report discussing your experience and knowledge gained from this task.

Instructions

Part A – Ethics Case Scenario

University introduced a project that gives students the opportunity to gain work experience as an intern in a public accounting firm. As a participant in this project, you had an opportunity to work at JM Accounting, a public accounting firm for a month. During the internship period, you received training from several employees of JM Accounting. In particular, you had opportunities to work closely with two individuals, John Roberts and Peter Clare. John works as a trainee accountant and Peter is John’s manager who works as a senior accountant.

John is now in his first year of training within the firm. A more senior trainee has been on sick leave, and John is due to go on study leave. John has been told by Peter that he must complete some complicated reconciliation tasks before he goes on leave. The deadline suggested by Peter appears unrealistic, given the complexity of the tasks.

John feels that he is not sufficiently experienced to complete the work alone. He would need additional supervision to complete it to the required standard, and Peter appears unable to offer the necessary support. If John tries to complete the work within the proposed timeframe but fails to meet the expected quality, he could face repercussions on his return from study leave. He feels slightly intimidated by Peter, and also feels pressure to do what he can for the practice that is now going through challenging times. John is facing ethical dilemmas about what he should do.

Write a business letter in your own words, addressed to John Roberts explaining:

1. the ethical principles that will be affected if he performs the reconciliation tasks, and

2. possible courses of action that he can take in this situation.

Part B – Reflection Report

Please follow the instructions below to complete this assessment.

1. Register an account with Accounting Pod. Access to Accounting Pod will be granted via email invitation to each student’s Torrens email address from the Accounting Pod team.

2. Complete the practice set by following the instructions provided by Accounting Pod. Note: Accounting Pod will offer you immediate task feedback (i.e., one piece of feedback per Xero technical task) and interactive technical support via its educational platform (during business days and within 24 hours response time)

3. Prepare a reflection report answering the following questions on 5 topic areas. Each topic listed in the template below requires evidence to support your reflection such as including a screenshot with an example of a specific practice set question relating to that topic.

Solution

Part A: Ethics Case Scenario

XYZ

Intern

JM Accounting

Date: 12th April 2022

John Roberts

Trainee Accounting

JM Accounting

884 Stanley St, East Brisbane QLD

4169 Australia.

Dear John,

I am writing this letter as I heard you are facing some ethical dilemmas regarding the reconciliation tasks allocated by Peter Clare. The prime purpose of this letter is to share my opinion regarding your confusion to maintain professional ethics before moving towards study leave.

Possible Ethical Issues for adopting the task

I get to know that the works allocated by Peter have an unrealistic expected timeframe and their completion possibility is beyond your professional experience. In such a scenario if you opt for the reconciliation then it will cause the violation of the ‘objectivity’ principle within the fundamental principles of APES 110 Code of Ethics forProfessional Accountants (Vermeesch, 2018). The objectivity principle is directed to not compromising judgements in the business and professional arena due to any sort of conflict of interest, biases, and undue pressure creation from any other irrespective of seniority. As it can deteriorate the quality of the activity and its adverse effects also can be implicated over the entire organisation.

Due to such compromise from your side, the needed integrity for the tasks would not be achieved which is also is a violation of the features of maintaining integrity in financing activities like straightforwardness and honesty as per APS 110 code (Vermeesch, 2018).

Also, Peter has not provided due supervision for the reconciliation tasks which can be dangerous for providing the required skill level and professional knowledge to ensure the competency of the tasks. Lack of competency in those tasks can hamper the expectation of the valued clients of JM Accounting which can generate negative implications for the organisation in the upcoming future. APS 110 also directs to maintain such competency in the professional activities and deliver the solution which nodes existing standards regarding technical and professional of the finance operations along with maintaining legislative regulations as well (Vermeesch, 2018).

I know you are feeling intimidated as if you turned the reconciliation then you have to face some negative issues within your professional career and this feeling also appears due to the behaviour of Peter. You should have to remember that if you optimise the reconciliation due to such a feeling then such activity can discredit the occupation desirables.

Driving by your level of expertise the quality of the reconciliation can be at stake due to such a challenging deadline which also can hamper three principles that are integrity, competency maintenance, and objectivity.

Possible Solutions regarding Ethical Issues

a. If you are opting for the reconciliation then you have to put your entire effort into the work. Any sort of half-heart action would not be correct in this regard. In that case, you have to shrink your study leave and move to leave after completing the work with quality and competence. Also, you should appeal for needed assistance to the top management of JM Accounting as by this any sort of quality concerns would not have arisen further.

b. If you do not want to act on the reconciliation without any future reputations then inform the top management regarding the entire situation including your purpose of such an application. Your application also should include your ethical dilemmas as well. If Peter receives orders from the top management only then he would not pressurise you for doing the work. Also, you can inform the violation of the professional behaviour from Peter’s side, however, for assignment help this activity should be entirely your discretion.

Sincerely,

XYZ

Part B: Reflection Report

.png)

.png)

.png)

.png)

.png)

.png)

.png)

![]()

References

.png)

MCR004A Accounting System and Process Assignment Sample

Assessment criteria

In assessing group report consideration will be given to overall neatness, completeness and quality of report, timeliness of submission and demonstrated application of appropriate issues in financial accounting and reporting.

Report is expected to be made in a clear, concise, and understandable manner. It is required that an outline be made at the inception of the report to show introduction, body, and conclusion of the report.

Group Report Topic:

Each group will be allocated a topic from section 2.5 of the subject outline (Topics are listed below) and each group will be allocated a company from ASX 500 top listed. Group report includes: (a) Overview of the selected company and (b) explanation of the selected topic with relation to selected company. Group Company selection and topic selection should be available in Moodle in week 2.

Accounting Systems and Processes Assessment 1 Group Report T2, 2022

Group Report Topics:

(a) Conceptual Framework

(b) Accounting Regulatory Body: AASB

(c) Company Regulatory Body: ASIC

(d) Accrual accounting concept

(e) Inventories: Perpetual method and Periodic method

(f) Accounting for current assets

(g) Accounting for non-current assets

Solution

Introduction

The assignment includes the analysis of the financial statement’s qualitative characteristics. The fundamental qualitative characteristics and the enhancing qualitative characteristics of the company have been discussed. The assignment also discusses the significance of the qualitative characters in decision making. It also includes a detailed analysis of the fundamental and enhanced qualitative characteristics per the reporting standards. The Financial reporting standards for assignment help prepared by the Australian accounting standards board applicable to the Australian economy's public and private sector entities have been discussed. Further, the assignment includes a detailed analysis of the qualitative characteristics of the financial information incorporated in the financial statements of the BHP group.

Overview of the company

The broken Hill proprietary company or BHP is a petroleum metal and public mining company of Australia head with its headquarters in Melbourne. It was founded in the year 1885. The company is engaged in the development to proceed in and extraction of coal, copper, oil, gas, and minerals. The company incorporates four divisions: copper, iron ore, petroleum, and coal. The sale of the company's products is across the globe in countries such as Singapore and United States. The organization's objective is to bring the individuals and utilities together in a way that creates a better world. The organization has been achieving this objective by using high-standard assets, prominent stocks, and opportunities for building long-term value and massive returns for its stakeholders (Bhp, 2022).

Overview of the topic