ACCM4300 Financial Reporting Assignment Sample

Assignment Brief

Weighting - 20% of the overall assessment

Submission Via Turnitin-written Memo

Due Date Monday of Week 10 at 19:55 AEST

Assessment information

Work individually as this is not a group assignment. Any work which has been copied or shared between students will result in a Fail grade for all students concerned. So please make sure that the answer to this individual assignment is your own work and not copied from any source.

Required:

Part (A) – Write a memorandum to the Board of Directors (the members of the Board have varying degrees of accounting knowledge or understanding) as noted in the assignment details. The memo should be no more than 1000 words.

Assignment Components

Part A: Technical Component (15%)

This mark covers the technical content of your advice and the explanation on each of the issues, the calculations and the sources and references used and the format of the memo

Details of the Assignment for assignment help

Select Company:

You will select a set of Financial Report of an ASX Listed Company and obtain approval from your lecturer for the Group of Companies that you have selected. Please note that no two individuals may work on the same Group of Companies, so if another individual has already registered their interest in a particular Group of Companies, you will be advised to select a different Group of Companies.

Read the Annual Report including the financial statements of the Group and write a Memorandum to the Board of Directors clearly explaining some of the technical aspects of consolidation. Make sure you draw on the company’s specific details to explain the intricacies of consolidation to the Board and as much as possible avoid answering in general terms.

Please make sure that your assignment is in a MEMO Format – A Report format will not be marked. The assignment must include appropriate references to Accounting standards and other regulatory bodies.

Some of the aspects that you need to cover in your assignment are (but not restricted to):

1. Why did the parent entity have to prepare consolidated financial statements when the subsidiary company is a separate legal entity in its own right?

2. Does the published set of group financial statements reveal the company’s policy on corporate governance, Audit committees, Sustainability, Solvency? Does it reveal these issues and if so where and why?

3. Has there been any goodwill on the acquisition? Or any gain on bargain purchase? Where would you find it in the financial statements and what does it mean? Any impairment?

4. Any other relevant matter that you may wish the Board of Directors to make note of in respect of some transaction or event, the balance of account or disclosure that will assist them in understanding the financial statements of the group.

Solution

Memo to the Board of Directors

Date:

Subject: Technical Aspects of Consolidation for Commonwealth Bank of Australia

Reasons for Consolidation:

Parent companies as well as the subsidiary companies under them are necessarily required to merge and produce the relevant financial information of both the companies under one statement, which is basically called the consolidated financial statements. The parent company needs to present all the financial information in the statement of income and expenses as well as the balance sheet and the cash flow statement of its own company as well as the relevant information of its subsidiaries in the consolidated income statement as well as the balance sheet and the statement of cash flows (Santis, Grossi and Bisogno, 2019). As far as the Commonwealth Bank of Australia is concerned, there are three main subsidiaries under the parent company, which are the Commonwealth Securities, The colonial First State as well as the Bankwest. As per the Australian Accounting Standards Board or AASB 10 as well as AASB 3, the parent company as well as the subsidiary company needs to show the relevant information in the consolidated financial statements as well as the vital adjusted financial statements and at the same time, include the points in the notes to the financial statements in the annual report of the financial statement (AASB, 2021). The annual report of Commonwealth Bank of Australia shows all the information of the main company as well as the information of its three subsidiaries and at the same time, all the relevant information about the joint ventures of the company with other companies and business organizations. This is very crucial as the adjustment of the fair values of all the accounts will then be possible and will reflect a true and fair image of the consolidation (AASB, 2016). A consolidation worksheet is a tool that includes making adjustments in attempt to recognize goodwill. Fundamentally, the parent company would be in the greatest position to gather all the information and offer an integrated look at the financial reports by excluding all intra-group transactions in order to measure the overall performance and wealth of an entire corporation. The parent firm can use the consolidated reports to assess its control over its subsidiaries and plan forward for the next aim the group intends to attain (Sánchez-Serrano et al., 2020).

Disclosures made by the Commonwealth Bank of Australia

As per the Board of Directors of the bank, a good corporate governance is the foundation of the success of all business companies and so, it is crucial for the all the companies to assess the risk and then attempt to implement strategies so that they are able to meet the objectives of the company. For this reason, the Board of Directors of the CBA has effectively adopted the comprehensive rules and regulations of Corporate Governance Guidelines, which is also in compliance with the “Corporate Governance Principles and Recommendations” that has been released by the ASX Corporate Governance Council (Chan, Watson and Woodliff, 2014). As far as the audit committee is concerned, the audit committee of the bank consists of three independent directors who have a good expertise in the field of accountancy and finance. The responsibilities of all the audit committee is duly fulfilled by all the members of the audit committee and the relevant disclosure have been made in the annual report of both the parent company as well as the subsidiary companies. Solvency refers to a company's capacity to satisfy its long-term financial obligations. The interest coverage ratio, which divides operational income by interest costs to illustrate a company's ability to pay interest on its debt, can be used to assess its solvency. A larger value indicates better solvency (Coulon, 2020). As far as the CBA is concerned, there is no disclosure as such which has been made in the annual report of both the companies, but the solvency situation can easily be analyzed using the financial metrics like the calculation and the interpretation of the solvency ratios, which will give a better idea about the debt liability position of the bank. As per the sustainability report of the Commonwealth Bank of Australia, the business organization aims at believing that the success of a business is dependent on the actions as well as the customer profile and satisfaction along with the great interests of the stakeholders and the community, and this is the sustainability goal of the bank as well (CBA, 2021). There are several disclosures that have been made by the sustainability report of the bank, which mainly consists of the:

1. Responsible Financial operations

2. Sustainable business practices

3. Community contribution and action

4. Engagement of talent in the company

5. Environmental Stewardship

Goodwill

As far as the goodwill is concerned, it is clearly evident from the fact that the bank is involved with a number of other financial institutions regarding funds management as well as brokerage and investment securities. The goodwill was definitely purchased upon the acquisition of the Aussie home loans, where there was a decrease in the overall value of the acquired goodwill by approximately $72 million as a matter of fact after the adoption of the AASB 15 by the bank (CBA, 2021). The goodwill will be mentioned in the notes to accounts sections of the financial statements of the annual report where the section of goodwill will be comprised under the Intangible Section and the amount which will be recorded will be the amount at which the goodwill is purchased as well as the closing amount. No impairment of the goodwill will be recorded in the financial statements of the parent company or the subsidiary company (Carlin, Finch and Ford, 2007).

Intra Group Transactions

These transactions are those transactions that takes place between the entities under the parent group of the company. These might include all the different transactions of the profit or loss that has been realized between the parent company and the subsidiary company. As far as the Commonwealth Bank of Australia is concerned, the intra group transactions also contains the different borrowed funds by the parent company to the subsidiary company and this way, the Board of Directors can easily get a fair and true picture of the financial status of the subsidiaries as well as the Bank after a thorough analysis of the intra group transactions (Pane and Dodds, 2020). This will be very helpful for an overall observation.

References

AASB. 2021. Compiled AASB Standard AASB 10 Consolidated Financial Statements. Retrieved 18 May 2021, from https://www.aasb.gov.au/admin/file/content105/c9/AASB10_07-15_COMPdec17_01-18.pdf

Almagtome, A., Khaghaany, M., &Önce, S., 2020. Corporate Governance Quality, Stakeholders’ Pressure, and Sustainable Development: An Integrated Approach. International Journal of Mathematical, Engineering and Management Sciences, Vol 5 No 6, pp. 1077-1090.

CBA, 2021. 2020 Annual Report - CommBank. [online] Commbank.com.au. Available at: <https://www.commbank.com.au/about-us/investors/annual-reports/annual-report-2020.html> [Accessed 19 May 2021].

Coulon, Y., 2020. Key Liquidity and Solvency Ratios. In Rational Investing with Ratios (pp. 47-62). Palgrave Pivot, Cham.

Kabir, H., Su, L., & Rahman, A., 2020. Firm life cycle and the disclosure of estimates and judgments in goodwill impairment tests: Evidence from Australia. Journal of Contemporary Accounting & Economics, Vol 16 No 3, pp. 100207.

Pane, T. and Dodds, N., 2020. Icing, spreads and tax avoidance purposes. Taxation in Australia, 54(11), pp.619-623.

Sánchez-Serrano, J.R., Alaminos, D., García-Lagos, F. and Callejón-Gil, A.M., 2020. Predicting Audit Opinion in Consolidated Financial Statements with Artificial Neural Networks. Mathematics, Vol 8 No. 8, p.1288.

Santis, S., Grossi, G. and Bisogno, M., 2019. Drivers for the voluntary adoption of consolidated financial statements in local governments. Public Money & Management, Vol 39 No 8, pp.534-543.

FINC20023 International Financial Management Assignment Sample

Question and Answer for assignment help

Suppose you are advising an Australian MNE. The company wishes to purchase a device that costs ¥ .

The company is planning to finance this investment in either of the two ways:

Choice 1

Borrow ¥ from a Japanese bank at an interest rate of p.a. for one-year to purchase the device. At the time of repaying the loan, the company will need some Australian dollar cash outlay to convert to the required Japanese yen repayment inclusive of interest.

Choice 2

Borrow A$ from an Australian bank at an interest rate of p.a. for one-year, and then convert the Australian dollar to Japanese yen at the current cross rate of ¥100.00/A$ to purchase the device.

Thus, at the time of repaying this loan also, the company will need some Australian dollar cash outlay.

Assume, the inflation rate in Australia and Japan are, respectively, and 0.95%, and the purchasing power parity (PPP) holds.

i. Which loan option will you advise the company to choose if the choice is solely based on the required Australian dollar cash outlay after 1 year?

ii. What other factors do you think the company will also need to consider concerning this financing decision?

Solution

Answer 1:

The Australian MNE is Planning to buy a device that costs ‘X’ Yens. There are two choices for the Australian MNE. As per the first choice, the company can borrow yen from a Japanese bank at interest. At the time of repayment, the company will need some Australian Dollar cash outlay to convert the Japanese Yen repayment amount along with interest. Hence in this cash outlay, there will be an inflation effect. Hence for conversion also, more Australian dollars will be needed since the conversion will be at the end of year 1.

However, in choice 2, the company shall borrow the dollars from an Australian bank at the current date, and convert the same into yen at the current cross rate and then buy the machine. Here we see that the local inflation shall hold well only since the yen was borrowed at the beginning and hence there is a fixed amount including the interest to be repaid to the Australian bank. The YEN payment is already done at the beginning of the year. Hence, going by the situation, we infer the following with regards to:

Option 1:

The double effect of inflation- since first borrows yen from a Japanese bank, and repay at the end of the year. Due to Japanese inflation, cash outlay will be extra. Also, the company will have to face local inflation and hence, there will be more cash outlay (Marsh 2013).

Option 2:

Single effect of inflation- borrows Australian dollars at interest now, convert into yen and purchase the machine now. There will not be any effect of Japanese inflation. Hence, the cash outlay will be less.

Solely based on the outflow of Australian dollars at the end of year 1, it is advisable to go for option 2 of loan procurement.

Answer 2:

Since there is limited information in the given case, we are trying to judge the situation as per the conditions mentioned in the case.

The given crossover currency rate is yen 100/A$ where A$ stands for Australian Dollar. Since the inflation rate is 0.95% for Yen, it can be assumed that at the end of the year, the rate will be Yen 95/A$. Since there is purchasing power parity, the inflation will be proportional to their exchange rates. However, the interest rate for both Japanese banks as well as the Australian bank has to be considered to ensure which option is best suited. Since purchasing power parity holds well, one certain thing is that the cost of the device, whether purchased in Australia or from Japan, the cost will be similar in net values. Therefore, the cost of the device in either country is not a matter of concern.

What is to be a matter of concern here is the inflation effect on the choice of finance which the company opts for, which has been already discussed in the previous answer. But, the interest rates may vary and that is something we must watch out for since that is a major effect in taking the financing decision (Gunn 2013). Since in choice 2, interest cost is saved, we can consider that to be the most effective cost decision since interest cost will be saved.

References

Gunn, N. (2013). PART 08: Investment planning - chapter 8.4: Risk profiling. London: Kogan Page Ltd. Retrieved from https://search.proquest.com/books/part-08-investment-planning-chapter-8-4-risk/docview/1810512948/se-2?accountid=30552

Marsh, C. (2013). Chapter 01: Stages In The Development Of A Business And Financial Model. London: Kogan Page Ltd. Retrieved from https://search.proquest.com/books/chapter-01-stages-development-business-financial/docview/1810265107/se-2?accountid=30552

BST903 Financial and Business Analytics Assignment Sample

INDIVIDUAL ASSIGNMENT

KEY DETAILS:

The individual assessed assignment counts for 50% of your final module mark.

The submission date for the assignment is: 11 February 2022 by 11.00a.m.

GUIDELINES

You are required to answer all parts of the assignment. The word limit for the assignment is 2,000 words, excluding appendices, tables and a reference list for assignment help Calculations may be included as part of the appendices (they will not form part of the word count). Please note that failure to comply with the word limit may result in a restriction of marks.

You will be awarded marks for the assignment for a number of different criteria, including evidence of conceptual understanding of the material being tested, clear and accurate analysis of the data, and analytical and critical thought. You will also be awarded marks for originality and evidence of additional reading. Finally, a proportion of marks will also be allocated for the structure, style and logical development of the report, and grammar and appropriate referencing (you should reference appropriately all your work and cite the complete list of references used at the end of the report).

Kindly double/1.5 space your report and submit it via Learning Central.

All administrative issues should be directed to the Postgraduate Hub: carbs-PGQueries@cardiff.ac.uk

1. Introduction

The board of directors met for their regular quarterly meeting on 6 January at which the CEO, Charles Chatters, presented details about a new project. The board also, as part of its agenda, considered the funding preferences for this project and potential future ones.

The meeting of 6 January was the first meeting that Fred Franks (FF) the new finance director attended. Discussions at the meeting got somewhat heated when FF suggested that the company use the net present value model of investment appraisal to appraise capital projects. CC immediately became defensive and resisted this advice - arguing that the company had traditionally used the accounting rate of return model and ‘there was no need to change methods of appraisal’.

CC and FF were also disagreed on methods of financing for future investment projects. While FF deemed it prudent to use the retained surplus cash within the company before seeking external funding, CC was keen to seek out new debt, as the cheaper form of finance. The company currently has surplus funds of £120 million.

Following the diverse views of the board, a decision was taken to seek advice from an external consultant.

2. Investment Project

In recent years, CC has been keen to move into the niche market of healthy snacks. Following a sizeable investment into the research and development of such products (the costs of which have been written off in the annual accounts), the company has developed a new healthy snack for toddlers, Wigglers. CC now hopes that Wigglers is a commercially viable product. His team has generated the following data.

i. The company would manufacture the product out of its Bournemouth site that is currently unused, if deemed worthwhile. It would require capital investment in plant and equipment of £100 million, half of which is payable immediately and the other half in twelve months’ time. The plant and equipment will have a useful life of five years, at the end of which it will be sold for £25 million.

ii. Annual sales volume of Wigglers is expected to be 10 million wholesale boxes for the first two years. Thereafter it will fall by 20% as competition rises; this fall will be a one-off in year three and stagnate at this level thereafter. The sales price per wholesale box has been proposed to be £22.00 for the duration of the project.

iii. Variable costs per wholesale box have been estimated as follows:

Variable materials 8.00

Variable labour 1.80

Variable overhead 1.20

In addition, fixed costs inclusive of depreciation of plant and equipment have been calculated at £84 million per annum.

iv. Depreciation is computed on a straight-line basis by the firm. All assets are depreciable.

v. The company requires a working capital investment of 10% of the annual sales value. 95% of the working capital investment is expected to be recovered. Working capital investment levels (and in turn working capital recovered) reflect any change in demand patterns.

The company pays taxes at a rate of 20% and makes ample profits onto which to pay this tax. Finally, Magenta plc has a required rate of return of 15%.

3. Company Background

Magenta plc’s humble beginnings started with a staff base of 18 employees in 1988 and a turnover of just £240,000. Currently listed on the Alternative Investment Market (in 2000), the company is valued at £4 billion and has 3,500 employees across 15 locations in the UK. Originally specialising in potato crisps, today the company manufactures a range of different snacks, catering for different client preferences. The company’s financial performance has generally shown an upward trend and in recent years this is in part a reflection of its rapid expansion programme under the leadership of the current CEO. CC joined the company 8 years ago and has led considerable expansion of the business and has two more years to run before he retires. One observation in light of the expansion plans is that Magenta plc is more heavily geared than its competitors – 10% more than the industry average (ruling out any outliers).

REQUIRED:

PART A (20 Marks, split equally between Ai and Aii)

Assuming that the objective of the firm is to maximise the wealth of its shareholders:

i. Appraise the investment project using the two models supported by senior managers and determine whether Magenta plc should proceed with the manufacture of Wigglers, giving a justification for your choice of model. You may use a spread sheet for your computations;

ii. Drawing on literature you are familiar with, evaluate the views put forward by the senior managers in relation to the financing choices should the current project (or indeed other projects) be selected, proposing a solution based on your assessment of the company’s position.

(Indicative word count: 400 words for Ai and ii combined)

PART B (40 Marks)

CC firmly believes that budgets should be set by the board and then imposed on those in functional/operational positions, whereas FF thinks that the company's budgeting system is far more likely to attain its objectives if employees and junior management are given a say in how their budgets are set.

Give a critical review of the two apparently conflicting opinions, considering claimed advantages and disadvantaged from both practical and theoretical perspectives.

(Indicative word count: 800 words)

PART C (40 Marks)

Based on data relating to the six major firms in the snack industry as presented in the tabs of the accompanying Excel spread sheet:

i) Calculate the industry weighted average of a) the return on capital employed (%) and b) the gearing ratio (%). You should fully discuss your weighted averages, and clearly explain any key underlying assumptions in making these calculations.

ii) Calculate the standard deviation for the two variables in C(i) above. You should fully discuss your results for the standard deviation, along with any assumptions you have made in undertaking these calculations.

You may choose whichever approach you consider the most appropriate for calculating the weighted averages but you must specify and justify that approach.

(Indicative word count: 800 words)

Solution

Part A

Appraise the investment project using two models.

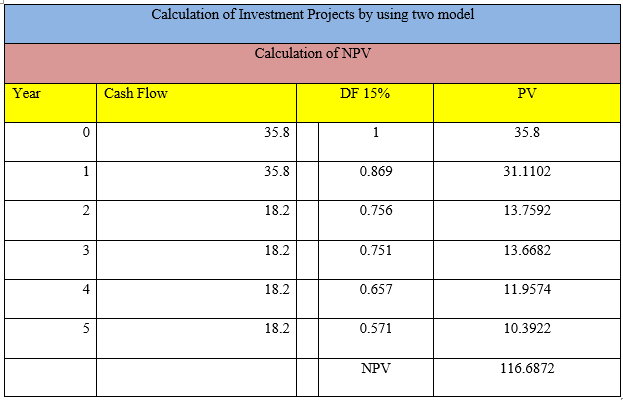

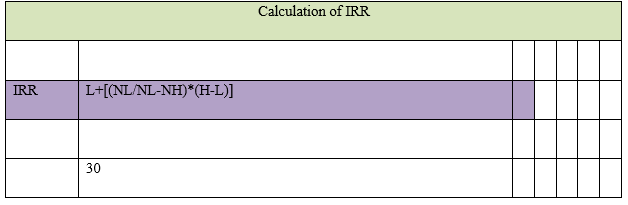

Table 1: Net Present Value

(Source: Created by Author)

Model NPV is considered as the time value of money. These are specified as the financial metrics that have to seek capture with the total value with potential value opportunity. Here, the value of NPV is 116.6872. Discounting factor is 15%. The positive value of NPV indicates the projected earnings that exceed the anticipated costs.

Table 2: Internal Rate of Return

(Source: Created by Author)

There is the calculation of IRR = L+[(NL/NL-NH)*(H-L)] (Wild 2019). Value comes in IRR is 30.

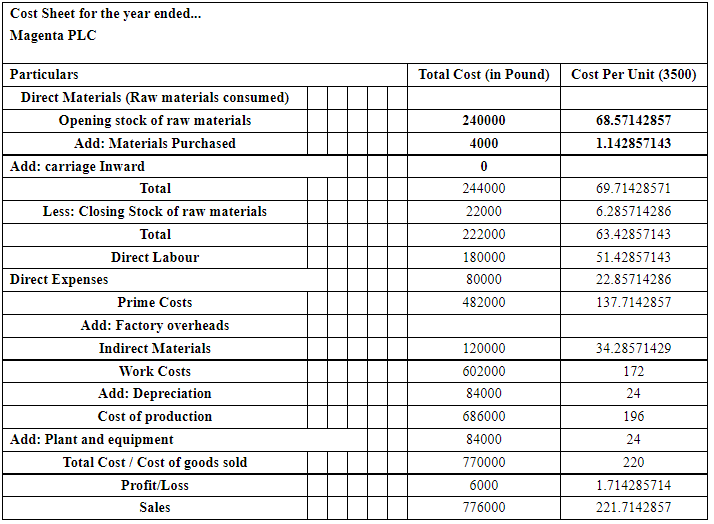

Table 3 Cost Sheet

(Source: Created by Author)

There is the following calculation of the cost sheet of Magenta PLC. The value of sales is GBP 694200. Here, the valuation of Magenta PLC is GBP 4 billion. Calculation of cost sheet is important for analysing production and factory costs (Appelbaum et al. 2017).Value of plant and equipment is GBP 84million.Magenta PLC is making working capital investments of 95%. Opening stock os raw materials are GBP 240000 million is based on 18 employees. Accurate costing information verifies the capacity to build and maintain a proper business in an organisation (Morningstar.com 2022). Here, the total cost/ cost of goods sold is GBP 688200.

Evaluate the views with senior managers about financing choice of current projects.

In this organisation, financial managers are responsible for the financial health of the organisation. Guiding as per supervisors in an individual’s departments is the following responsibilities roles of the senior managers. Investing and financial planning have to be analysed organisation weaknesses and strengths. Managers of organisations help to improve the profitability of an organisation. The above financial analysis is familiar with the business because of the positive value of Net present value. The positive value of net present value iis accepted for investment analysis. This current project must be select for the organisations current position. Most simple way of net present value determines about the market capitalisation of an organisation. Managers should be accepted positive value of NPV because of the free additional cash flows. Magenta PLC is required working capital investments 10%. Positive amount of IRR is also acceptable of a business organisation. Calculation of Net present value is done with the help of discounting factor 15%.This mainly, indicates about the angel investments, which is considered as the good for the organisation.

Senior manager assisting departments by creating and managing forecast and budgets for gathering information of an organisation. Financial manager helps to build capital structure of the organisation (Sun et al. 2017). This business used as a combination of financing sources and raising funds. Proper financial decision helps to perform in the financial statement analysis of the organisation.

Part B

Advantages and disadvantages of budgets in both theoretical and practical perspectives

Top down is more tedious in nature and have a vital advantages in growth of financial. Proper budgeting should be used in managing the money efficiently. Top down approach has an advantage for stating based on goal and budget allocation in an organisation. Specific flexible budgets are created by using formula and certain price of the organisation. Budgeting helps to know about the specific information of financial position in the organisation and in this organisation, flexible budgets and saves time with more realistically emphasising executive resource planning and decision in an organisation.

Figure b.1: Graph of budget in CC firm

(Source: Kim et al. 2020).

Certain financial criticisms of budgets have to reduce flexibility and entities of an organisation. Proper budgeting systems arises motivation of an organisation. Bottom down approaches in budgets is creating a financial budgeting in an organisation. Proper department of the organisation is creating is creating cost projection and list in expenses. Budget of employees in bottom down approaches of budgets can approved capital expenditure in a specific period.

A disadvantage in top down approaches may lead over and under employment with new plan of budget allocation. Top down approaches of may result in unrealistic calculation economic situation and organisational activities. Budgeting mainly allows to the financial managers to explore revenue and price within the sets of the operating assumptions. This represents a certain qualifications within management features. The Top down approach has eliminated bulks and fragment and accumulated High employment coverage and with having top visibility are the advantages of implementation in practical approaches. Specific standardize with services and products is having a business impacts of the theoretical approaches in management. Whereas the Bottom ups approach has initially identified the Proper budgets are having conflicting roles to evaluate co coordinating activities in an organisation. Output of the budgets should be matched with projected sales. In preparing the budgets properly, managers of all the levels of management have to take systematic rules of the organisation (Aydiner et al. 2019). Operational budgets systems are having vital roles that built difficult to meet them. It is often to evaluating individual managers from their budgets standards effects in price or certain circumstances in this development expenses.

There is the potential conflict of top down approaches between motivation and evaluation roles of budgets. Top down approaches involves with senior management team that can improve high level of budgets in organisation. During the end of the budgets periods, certain modification and adjustments have to be made for changing this environmental condition in this organisation. Budgets are having specific consequences that have to achieve financial and academic goal of these organisation. Bottom down budgeting helps in indicating faster budgeting procedure and better financial controlling of the organisation. Effective budget mainly, forecast expenses and incomes of this organisation. Significance of the budgets helps to make investment contribution. Inaccurate forecasting and having potential with underperformance can be deducted in performance of demand planners in the organisation (Vidgen et al. 2017). Budgets are the following estimation of expenses and revenue in a specific future period.

Budgeting is also having unrealistic outcomes in this organisation. Following budgets is also set with assumptions that generally are not so distant in operating conditions. Top down approaches; budget can save both resources and time of the organisation. Due to these approaches, managers of the organisation can saves time in organisation and can use to formulate of implementation in budget Proper cost structure and organisation’s revenue can be change actual results from this expectations plotted of the budgets. In this organisation, there is rigid decision making in the practical perspective of budgets functions. Here, budgeting procedure mainly, focuses in the attention of management strategy and team during this budget formulation. Top down approaches of budgeting have to decreases the motivation of lower level manager. For this top down approaches, there is creating a conflict between organisation executive and lower level manager. Proper budget creation in practical perspectives is a very time consuming. Work required in the budget is more extensive, if the conditions of the business constantly change in the repeated iterations of budgets periods. Time is consuming low, if there is better design in the creation of budgets. In this organisation, an experienced financial manager can be attempt in introducing budgetary slack, this mainly, involves deducting in estimating revenues and also improving this estimated expenses.

Lack of Practical perspectives in budgets is having expenses allocation that prescribed a specific amount of certain price. Managers of expenses allocation departments of this organisation are not allowed to provide alternatives due to the lower price services. Thus, proper budgets is making tends for the managers entitled certain amount of funds in a year. If this department is allowed with specific amount of expenditure, then it cannot appear in the quantitative aspects of the business (Appelbaum et al. 2018). Following nature of budgets is so numeric and it considers as a financial outcomes of this business. This usually means that the budgets intend to focus in maintaining or improving aspects of profitability. If, this department does not have any of the budgeted outcomes, then this department managers can be blame any of the other departments and provides certain services.

Top down approaches is creating easier to manage in implementation and drafting with goal of organisation. Ideas or projects in bottom down approaches are deciding proper values of organisation’s budgeting, that provides a great expectation in organisation. Budgets lead to the inflexibility in the decision making of an organisation. Budgeting has to be considered as the time consuming process in any of the large business. Procedure of budgets, is mainly consider financial outcomes. Proper nature of budgets tends to focus with management attention in these quantitative aspects of organisation.

Part C

Calculate the industry weighted Average

ia) Return on capital employed

Table 5: WACC

(Source: Created by Author)

Table 6: Calculation on Return on capital employed and Gearing Ratio

(Source: Wang and Byrd 2017)

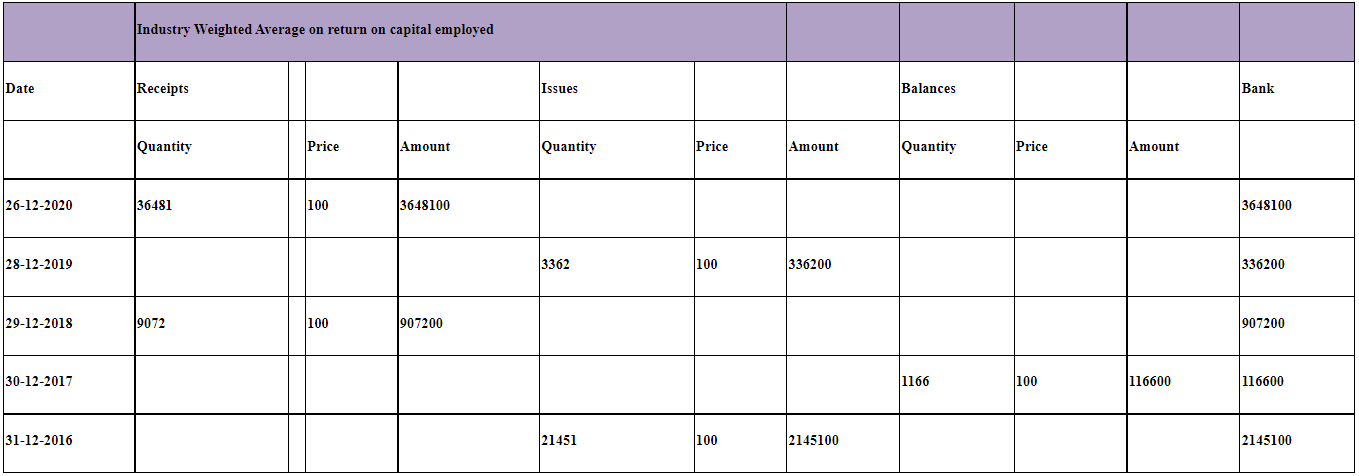

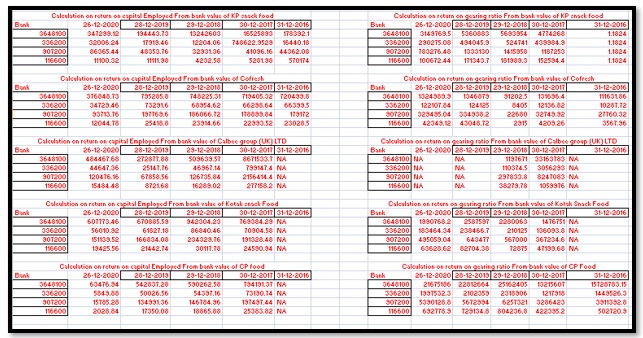

The Calculation of WACC is done by net tangible assets and Here, in 26-12-2020 36481*100 = 3648100, in issues of 28-12-2019 is 3362*100 = 336200, in receipts amount of 29-12-2018 is 9072*100 = 907200, in balance amount of 30-12-2017 is 1166*100 = 116600, in 31-12-2016 is 21451*100= 2145100. There is the following calculation of weighted average method of capital employed. Here, is the calculation of receipts, issues and balances of the bank. Further calculation of Specific amount of 26-12-2020 is GBP 3648100, in 28-12-2019 is GBP 336200, in 29-12-2018 is GBP 907200, in 30-12 2017 is GBP 116600 and in 31-12-2016 is GBP 2145100. There is the calculation of WACC from the ratio return on capital employed and gearing of five companies. Five companies are KP snacks limited, co-fresh, Calbee group (UK) limited, Kotak snack food and CP food.

Return on capital employed has to be calculated with the dividing net profit and capital employed (Wang and Byrd 2017). It is useful to calculate because of comparing the performance of the organisation with the sectors of capital intensive. These analyses prove as the following business gains from the certain assets and liabilities of this organisation (Lacerenza et al. 2018). Return on capital employed represents amount of specific capital investment in front of operations.

b) Gearing Ratio

Table 6: Gearing Ratio

(Source: Created by Author)

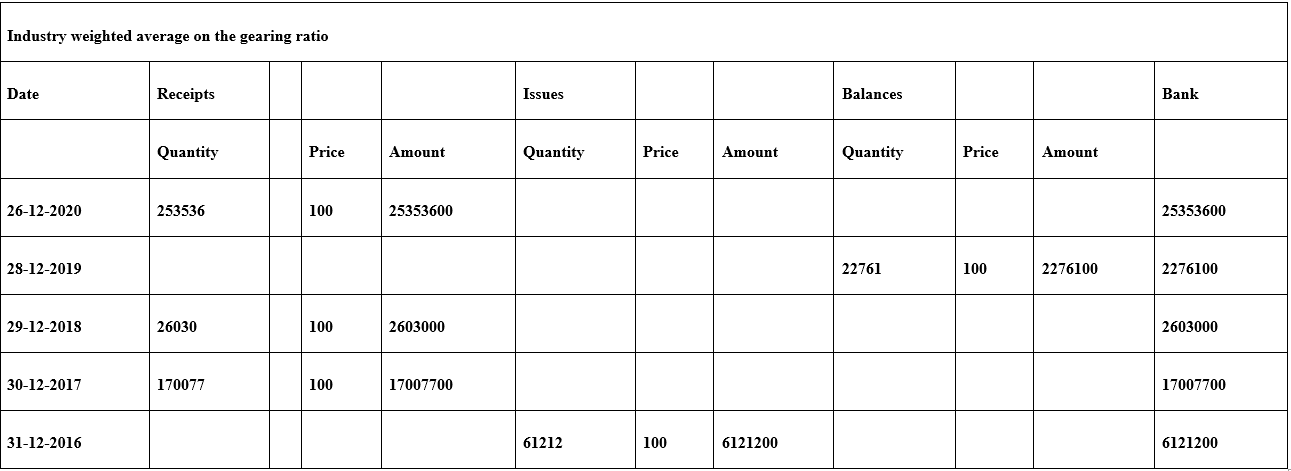

Industry weighted average return on gearing ratio have to be calculated in multiplying costs and capital of each of the following sources (Kumar et al. 2017). This causes a relevant sources of equity and debt, that can determines value of organisation. Calculation of the has been done by identifying Balance of 26-12-2020 has been calculated as GBP 25353600, in 28-12-2019 is GBP 2276100, in 29-12-2018 is GBP 2603000, in 30-12-2017 is GBP 17007700 and in 31-12-2016 is GBP 6121200.

Capital employed of the following balance sheet is the measure of reduced in valuing assets and current liabilities. Here, present liabilities of an organisation are considered as the portion of organisation’s debt. Working capital in gearing ratio maily, shows the amount of liabilities and assets of an organisation (Kokina and Davenport, 2017). Capital investments in gearing ratio represents how much of owner has invested into the business along having prospering profits. Gearing ratio mainly measure, how much operation are funded and received from shareholders as an equity. Gearing ratio in weighted average return indicates financial leverage and level with interest bearing of organisation. This analysis mainly, determines about the firms operation have to be funded with the shareholders. There is having appropriate level of the gearing ratio in organisation (Hofmann and Rutschmann 2018). 60% of this organisation shows debt level and 60% of its having equity. Gearing ratio can be manageable, for the utility in an organisation.

ii) Calculate the standard deviation of two variables

Table 6: WACC

(Source: Created by Author)

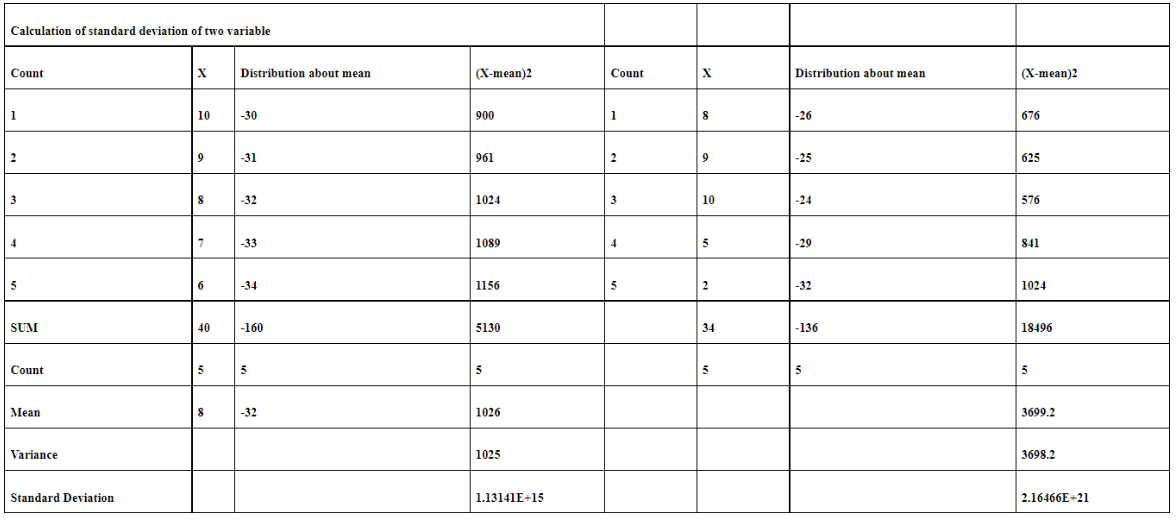

There is the following calculation of standard deviation of X and Y. Standard deviation of X is 1.31 and standard deviation of Y is 2.16. This analysis verifies about the spreading the values within datasets. Following calculation of variance of X have to be done by sum/Count-1. 5130/5 = 1025. Variance of X is 1025 and variance of y is 3698.2. The analysis of standard deviation is the following statistical terms that have to be measured in financial statements. Standard deviation is useful in analysing of trading strategies and also formulating proper investments decision of an organisation (Weber et al. 2019). Potential investments of an organisation are having important factors of an organisation. Return of investment helps in determining specific standard deviation of the organisation.

Analysis of standard deviation helps to calculate proper margins with error in consumer satisfaction and inventory prices. Standard deviation has to be determined by the variability in an organisation. Proper variance can help in finding distribution of information in this analysis. Standard deviation specifies the accurate mean of an organisation. Uses of standard deviation cannot assume its normality of the organisation. Formula of identifying the distribution of mean is (X-mean) and (X-mean) 2. Following calculation is based on the square root of the two variance by determining the data points related to its mean (Shaturaev, and Bekimbetova 2021). Assumption of normal distribution in standard deviation has to be obtained by random allocation and random sampling.

References

Journal

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z. 2017. Impact of business analytics and enterprise systems on managerial accounting. International Journal of Accounting Information Systems, 25, pp.29-44. Available at: DOI: http://dx.doi.org/10.1016/j.accinf.2017.03.003 R. [Accessed on: 1st February 2022]

Appelbaum, D.A., Kogan, A. and Vasarhelyi, M.A. 2018. Analytical procedures in external auditing: A comprehensive literature survey and framework for external audit analytics. Journal of Accounting Literature, 40, pp.83-101. Available at: DOI: https://doi.org/10.1016/j.acclit.2018.01.001. [Accessed on: 1st February 2022]

Aydiner, A.S., Tatoglu, E., Bayraktar, E., Zaim, S. and Delen, D. 2019. Business analytics and firm performance: The mediating role of business process performance. Journal of business research, 96, pp.228-237. Available at: DOI: https://doi.org/10.1016/j.jbusres.2018.11.028 R [Accessed on : 1st February 2021]

Hofmann, E. and Rutschmann, E. 2018. Big data analytics and demand forecasting in supply chains: a conceptual analysis. The International Journal of Logistics Management. Available at : DOI: https://doi.org/10.1108/IJLM-04-2017-0088. [Accessed on: 1st February 2021]

Kim, A., Yang, Y., Lessmann, S., Ma, T., Sung, M.C. and Johnson, J.E. 2020. Can deep learning predict risky retail investors? A case study in financial risk behavior forecasting. European Journal of Operational Research, 283(1), pp.217-234. Available at: https://core.ac.uk/download/pdf/250590642.pdf. [Accessed on: 1st February 2021]

Kokina, J. and Davenport, T.H. 2017. The emergence of artificial intelligence: How automation is changing auditing. Journal of emerging technologies in accounting, 14(1), pp.115-122. Available at: DOI: 10.1002/isaf.277 [Accessed on: 1st February 2022]

Kumar, A., Sah, B., Singh, A.R., Deng, Y., He, X., Kumar, P. and Bansal, R.C. 2017. A review of multi criteria decision making (MCDM) towards sustainable renewable energy development. Renewable and Sustainable Energy Reviews, 69, pp.596-609. Available at: DOI: http://dx.doi.org/10.1016/j.rser.2016.11.191 R [Accessed on : 1st February 2022]

Lacerenza, C.N., Marlow, S.L., Tannenbaum, S.I. and Salas, E. 2018. Team development interventions: Evidence-based approaches for improving teamwork. American Psychologist, 73(4), p.517. Available at: DOI: 0003-066X/18/$12.00 http://dx.doi.org/10.1037/amp0000295 [Accessed on: 1st February 2021]

Shaturaev, J. and Bekimbetova, G. 2021. THE DIFFERENCE BETWEEN EDUCATIONAL MANAGEMENT AND EDUCATIONAL LEADERSHIP AND THE IMPORTANCE OF EDUCATIONAL RESPONSIBILITY. InterConf. Available at: DOI: 0000-0002-0982-5741. [Accessed on : 1st February 2022]

Sun, Z., Strang, K. and Firmin, S. 2017. Business analytics-based enterprise information systems. Journal of Computer Information Systems, 57(2), pp.169-178.. Available at : DOI: 10.1080/08874417.2016.1183977 [Accessed on : 1st February 2022]

Vidgen, R., Shaw, S. and Grant, D.B. 2017. Management challenges in creating value from business analytics. European Journal of Operational Research, 261(2), pp.626-639. Available at: DOI: https://eprints.bbk.ac.uk/id/eprint/19847/ [Accessed on: 1st February 2022]

Wang, Y. and Byrd, T.A. 2017. Business analytics-enabled decision-making effectiveness through knowledge absorptive capacity in health care. Journal of Knowledge Management. Available at: DOI: link to article: https://doi.org/10.1108/JKM-08-2015-0301 [Accessed on – 1st February 2022]

Weber, M., Domeniconi, G., Chen, J., Weidele, D.K.I., Bellei, C., Robinson, T. and Leiserson, C.E. 2019. Anti-money laundering in bitcoin: Experimenting with graph convolutional networks for financial forensics. arXiv preprint arXiv:1908.02591. Available at: DOI: https://arxiv.org/pdf/1908.02591.pdf. [Accessed on: 1st February 2022]

Wild, J. 2019. Financial Accounting: Information for Decisions, 9e.DOI: Detailed List of New Features. Available at: http://ecommerce-prod.mheducation.com.s3.amazonaws.com/unitas/highered/changes/wild-financial-accounting-9e.pdf [Accessed on: 1st February 2022]

Website

Morningstar.com, 2022. Magenta 2020 PLC. Available at: https://www.dbrsmorningstar.com/issuers/24720/magenta-2020-plc. [Accessed on: 1st February, 2022]

HI6028 Taxation Theory, Practice and Law Assignment Sample

Question 1

A. John recently purchased a Theatre Hall which was in poor condition. Before starting the hall, it needed to repair a portion of the ceiling, but he decided to replace the whole of the ceiling with different but better materials. The new ceiling, in addition to enhancing the appearance of the hall, improved the acoustics. The total cost of the material and of erecting the new ceiling was $210,000. It was estimated that the cost ofrepairing the ceiling would have been $150,000.

With reference to Income Tax Assessment Act 1997 and relevant case law, discuss the amount, if any, allowable as a deduction for income tax purposes. Kindly use the following instructions:

1. Facts of the scenario

2. Relevant laws and cases

3. Application of laws and cases

4. Conclusion

B. Sanjeev is employed as a marketing manager of the Theatre Hall. He requires to travel extensively during the year for work-related purposes using his car. Discuss the ways Sanjeev might be able to claim deductions for his car expenses. HI6028 Taxation Theory, Practice and Law Individual Assignment T1.2022

QUESTION 2

After completion of your course, you start working at an accounting and tax office. Julia is your first client. She requires to lodge his income tax for 2021/22. She gave her annual income and deduction below. Calculate her Total Assessable Income, Taxable Income, Tax Liability, Medicare Levy and Medicare Levy Surcharge, if applicable, for the taxpayer (Julia) with the information below:

• Julia is a resident single mom with two dependent children (7 and 4 years old) taxpayer of Australia for the tax year 2021-2022

• Her Taxable Salary earned is $109,000 (Including tax withheld), having no private health insurance.

• She had a $11,000 deduction.

• Julia has a student loan outstanding for his previous studies at Sydney University of $35,000.

• Julia’s employer pays superannuation guarantee charge of 10% on top of her salary to her nominated fund.

• Julia earned a passive income of $7,000 from the investments in shares in the same tax year.

Solution

Question: 1

a. Deduction for repairs and maintenance:

Facts of the scenario:

In this case, John has recently purchased a theatre hall which was in poor condition and wanted to repair that portion of the ceiling which would have cost $150,000. But, instead of carrying out the repairs on that portion of the ceiling, John has decided to replace the entire ceiling with different and better materials. This new ceiling will also enhance the acoustics of the building and the total cost will be $150,000. Hence, the issue here is John wants to know whether he will be able to claim a deduction for the replacement of the ceiling that he is doing under the income tax assessment act 1997.

Relevant laws and cases:

The income tax assessment act 1937 deals with the scenarios for assignment help under which deduction will be allowed to the taxpayer under section 25-10 or section 8(1) i.e. the general deduction or the specific deductions. From the facts of the case, it is the case of allowing deduction under repairs and maintenance head and to increase the understanding income tax assessment act 1997 has come up with a 97/23 ruling where previous laws have been referred to and an understanding has been created by the regulations.

As per the clarification, repairs mean making good the defects, or damages to the property or building. The object is returned to its original form in case of repairs and does not lose its originality. Hence, in this case, the only deduction will be allowed under sections 25-10 but if major changes are made to the building or property and the property loses its form, then the deduction under this section will not be allowed. It means that only revenue expenditures are allowed as a deduction, and if any capital expenditure is done to the property, it will not be allowed as a deduction and it will be added to the cost of building, on which the taxpayer can charge depreciation(Barkoczy, 2021 p9(6)).

Hence, the word repairs do not include the word replacement or reconstruction and if replacement is done in its entirety then the same will be treated as a capital expenditure which is not deductible. The same was decided in W Thomas & Co Pty Ltd v FC of T (1965) that the taxpayer will not be allowed to claim a deduction of the expenditure that was incurred on extensive renovations. The High court also stated that expenditure done on the building will not be claimed if, without the certain renovation, the building will not be able to continue as an income-generating unit.

So, it is very important to differentiate between the word repairs, replacement, renovations, and whether a particular expenditure is in the nature of capital or revenue. For instance, if a repair is termed as an improvement, it will not be counted as repair. Also, if the repair changes the character of the building and improves the efficiency of its economic nature, then the same will not be treated as repairs and will not be considered in the revenue nature. It is also said, if the nature of the material used is improved, the changes will be counted as improvement and it will not be considered repairs (Christians, et al., 2018 p5(6)).

Applications of laws and cases:

The ruling and the case law discussed above are applicable in this case as well. John was thinking to repair the part of the ceiling which was damaged, but later he decided to replace the whole part too with better and improved material, which will also improve the acoustics of the place, and as it is a cinema hall it will attract more customers. The ruling has stated that if a farmer is thinking to replace the damaged portion of the fence, it will be considered a revenue expenditure which is allowed as a deduction and the farmer will get the benefit of the deduction. But if the entire fencing is replaced it will be considered a capital expenditure which is not allowed as a deduction. Hence, here, the replacement of the ceiling will not be included in the definition of repairs (Ingram, 2021 p9(1)).

Conclusion:

From the above discussion, it can be concluded that John will not be allowed to take a deduction of the repairs that he had done on the ceiling because first it will be considered as a replacement, and it was not done to make good the damage, but, the entire ceiling was repaired, which will be considered as an improvement, and improvements are not allowed as revenue deduction and will be charged to depreciation. Also, this change has increased the cost of repairs and will increase the efficiency which will increase the economic flow. Hence, this expenditure will not be allowed as a deduction to John as per the Income-tax assessment act 1997, and it will instead be added to the cost of building.

b. Deduction for Work-related car expenses:

Section 8.1 of the income tax assessment act 1997 states that there are certain circumstances where deduction will be allowed for work-related expenses to the taxpayer as a general deduction. The expense will be allowed to be deducted from assessable income when it is incurred to earn the assessable income or to continue with the business or profession it is crucial to incur the expense. But, the expense will not be allowed as a deduction if it is in the nature of capital expenditure or it is incurred to earn exempt income or a particular provision in the act restricts the person from claiming the deduction.

In this case, it states that Sanjeev is employed with the company and his work ask him to travel extensively for work-related purpose using his car. Here, Sanjeev wants to know whether he will be able to claim the deduction on car expenses which he has incurred for work purposes. Hence, after reading the law, it can be said that work-related expenses incurred by the taxpayer are allowed as expenses because they are incurred to earn the assessable income, and they are necessary to earn the income. In this case, the car has been used by Sanjeev for work purposes, and hence, he will be allowed to claim a deduction on the same, but, it is important to notice this expense is not in the form of reimbursement and the employee has paid for these expenses (Allen, 2020 p5(9)).

Also, if the car has been used by the taxpayer for both private purposes and for work-related purposes, then the deduction will be allowed only for work-related expenses and the taxpayer will not be allowed to take a deduction for private use. Also, if the expense is in the nature of capital then the same will not be allowed as a deduction. Travel related expenses will be considered work-related expenses till the time, they are used for business purposes or to earn income. If the work of Sanjeev is travel based, he will be allowed to claim the deduction because he is using his car for travelling for work purposes and not for this personal expense. However, in some cases the travel expense incurred on the way from home to work and vice-versa are not allowed because travelling from home to work is extremely essential and domestic (Legwaila, 2018 p5(2)).

Question: 2:

Calculation of assessable income and tax:

From the above, it can be said that the net tax liability that the taxpayer will be liable for discharge is $33,517. The taxpayer is an individual who has two dependents. The assessable income of the taxpayer will include the income from salary and the passive income earned by the taxpayer. The income tax is charged on the basis of rates that have been prescribed by the taxpayer and the same are as follows:

.png)

Here, the tax will be calculated as follows. For first 45,000 the tax will be 5,092 and for the remaining amount the tax will be (105000-45001) * 32.5% = 19,500. The Medicare levy will be charged as 2% of the taxable income i.e. the income calculated after reducing deductions from the assessable income.

Reference:

.png)

HI6028 Finance Assignment Sample

Question 1

An owner of a Cinema Hall, on ascertaining that a portion of the ceiling of the hall was in need of repairs, decided to replace the whole of the ceiling with different but better materials. The new ceiling, in addition to enhancing the appearance of the hall, improved the acoustics. The total cost of the material and of erecting the new ceiling was $320,000. It was estimated that the cost of repairing the ceiling would have been $220,000.

With reference to Income Tax Assessment Act 1997 and relevant case law, discuss the amount, if any, allowable as a deduction for income tax purposes.

Kindly use the four sections of:

1. Facts of the scenario

2. Relevant laws and cases

3. Application of laws and cases

4. Conclusion

QUESTION 2

A new client, Mary, is your first client. She needs to lodge his income tax for 2021/22. Further, she wants to know about some tax-related provisions and practices. She asks some questions - what are the differences between taxable income, ordinary income, and statutory income? What types of ordinary and statutory income do not constitute assessable income? (Maximum 700 words)

Furthermore- She gave her annual income and deduction below. Calculate her Total Assessable Income, Taxable Income, Tax Liability, Medicare Levy and Medicare Levy Surcharge, if applicable, for the taxpayer (Mary) with the information below:

- Mary is a resident single mom with one dependent child (4 years old) taxpayer of Australia for the tax year 2021-2022

- Her Taxable Salary earned is $110,000 (Including tax withheld) having no private health insurance.

- She had a $12,000 deduction.

- Mary has a student loan outstanding for his previous studies at Queensland University of $32,000.

- Mary’s employer pays superannuation guarantee charge of 9.5% on top of her salary to her nominated fund.

- Mary earned a passive income of $5,000 from the investments in shares in the same tax year.

Hint: The following website can be used to cross-check your answers but you need to provide detailed calculations, rates and explanations of rates from ATO website.

QUESTION 2: Income Tax Calculation and explanation Weighting

- Answer tax related questions 5%

- Total Assessable Income 1 %

- Total Taxable Income 1 %

- HELP repayment amount 1 %

- Medicare Levy 1 %

- Medicare Levy Surcharge 1 %

- Total Tax Liability 3%

Solution

Answer 1

1. Facts of The Scenario

The facts of the scenario are concerned with eligibility of deduction of expenses from the income by considering the Income Tax Assessment Act 1997. In the cited scenario, assesse has spent amount for repairing and maintenance expenses, whether or not such amount for assignment help can be deduced while computing taxable income, is required to be discussed.

2. Relevant Laws and Cases

Division 8 of the ITAA 1997 explains that, taxpayer could decrease their profit from particular expenses, which is divided into two following categories –

General deduction (section 8.1): According to the cited section, if taxpayer has expenses or losses from production of assessable income from directly or indirectly, then they could deduct it under section 8.1. It has been provided that, assesse could reduce their assessable profit or expenses or losses to the extent they are incurred in earnings of assessable profit or mandatorily occurred in running on a business for the objective of achieving or generating assessable profits (Australian Taxation Office, 2021).

Section 8-1(2) of ITAA 1997: According to the cited section, following are the amount is not allowed as deduction from the assessable income under section 8-1 –

- If expenses or losses are in capital nature.

- If they are occurred for the personal objective (Millane, &Stewart, 2019, p. 505(2)).

- If expenses assists towards production of non-assessable non-exempt profit.

- If they are not eligible for deduction under any particular provision of ITAA 1997.

Specific deduction (Section 8.5): Along with general deductions, things could be added to decrease income of assesse if it is allowed under any particular section.

Section 25-10 of ITAA 1997: The taxpayer is eligible to avail deduction for repair of premises or depreciating assets that has been held for profit generating objective. Repair is referred as fixing something that is defective, which does not means renovation of the property, and creating the increment in value by application of distinct material (Burton, 2018, p. 34(1)). It should be noted that, there is difference between repair and improvement, and assesse is eligible to claim only expenses of repair and maintenance (Jones, 2018, p. 32(2)). In the case of FCT v Western Suburbs, assesse replaced the cinema ceiling by using distinct type of material, and the new material was better material. In this, it was stated by court that, it is considered as capital expenses because there was an improvement on the property (Woodcock, 1997). Further, in the case of Lindsay, court denied the deduction in which old ship ramp was demolished and replaced.

Moreover, as per the decision given in the case of W Thomas, repair expenses leads towards restoration of efficiency in functions instead the precise repetition of forms and material. It is because; anything would definitely get improved by repairing (Hümbelin, & Farys, 2017, p. 1(2)). Therefore, a limited improvement in the efficiency of function is not any concern for deduction of amount as improvement of the condition of items is possible by all repairs as compared to its earlier condition (Curran, & Yapa, 2021, p. 18(2)). On the other side, improvement is considered as adding benefits consisting of permanent features. In the case of Morcom v Campbell-Johnsom, a replacement with a modern comparable is considered as repair.

There is not any clear distinction between what is considered as repair and what an improvement expense is. Generally, if the expenses lead towards significant efficiency of functions rather than minor, then it is considered as improvement expenses in nature and therefore it will not allow for deduction from assessable income as per section 25 of the ITAA 1997 (Hrblock, 2020).

3. Application of Laws and Cases

The scenario states that, owner of cinema hall requires repairing of ceiling and he decided to make replacement of whole ceiling with distinct but better material. The facts of given case scenario is quite similar with the case of FCT v Western Suburbs. Since, expenses incurred replacement of whole ceiling with distinct but better material is considered as improvement rather than repair and maintenance. The reason behind the same is that, such expenses lead towards betterment of condition or increased value of ceiling beyond its original condition at the time of buy. Moreover, it is not considered as minor improvement in the functional efficiency of item as it is adding additional benefit, which has long lasting nature. Due to such aspect, such expenses are considered as improvement expenses instead of repair and maintenance.

By application of relevant provisions of ITAA 1997, it can be concluded that, expenses incurred by owner of cinema hall is not considered as repair and maintenance expenses of assets held for income generating purpose. Instead of this, expenses are considered as improvement, and therefore it is capital nature expenses and will not be allowed as deduction from assessable income.

Answer 2

In the prevailing case scenario, Mary requires to file income tax return for the year 2021-2022. However, prior to filing such income tax return, she wants to understand some provisions and practices of ITAA 1997. In this aspect, some of the requirements stated by her is explained as follows -

Dissimilarities between taxable income, ordinary income, and statutory income

Section 6-1 of the ITAA 1997 states that, assessable income of person consists of ordinary income and statutory income. Further, section 6-5(1) of the cited Act says that, assessable income includes income as per the ordinary concept. In the legal case Scott v FCT, it was stated by judges that, what receipts should be considered as income should be ascertained as per the ordinary concept and the application of mankind provided it is explained in statue otherwise. Therefore, it can be said that, ordinary income is the income generated as per the ordinary concept.

Further, it should be noted that, taxable income is the amount on which tax is levied by government. Since, ITAA 1997, section 8(1) and 8(5) explained about deduction of expenses from the assessable income, and tax is charged on the remaining amount. As per Section 4-15 of ITAA 1997, taxable income is computed from assessable profit and deduction.

Further, section 6-10 of the ITAA 1997 defined statuary income, which is the income of assesse that does not falls as ordinary income but it is required to include in the assessable profit due to particular rules in the ITAA 1997. For instance, capital gain is considered as statuary income of assesse.

Types of ordinary and statutory cinema do not consider assessable profit of assesse

The amount that is not included in the assessable income is divided into following categories such as –

Exempt Income: As per section 6-1 of the ITAA 1997, assessable income does not include exempt income, which is the tax-free income for assesse. Examples of exempt income includes but not restricted to following –

• Business grants and some scholarship.

• Some overseas allowance and payment for members of ADF (Australia defense force).

Non-assessable, non-exempt income: It is the receipts that are not assessed and payment of tax is not required to be done by taxpayer. Examples of non-assessable, non-exempt income includes but not restricted to following –

- Payments made by states as per Disaster Recovery Funding Arrangement 2018 in relation to 2019-20.

- Super co-contribution

Other receipts which is not included in assessable income: Usually, some of the following amount is required to declare by assesse –

- Winning money in ordinary lotteries.

- Gifts on special occasion.

- Prize receives on game show.

- Child help and spouse maintenance payment received by taxpayer.

Computation of income tax for Mary

By application of above concept of assessable income, calculation of assessable income for Mary is as follows –

Assessable income = Ordinary income + Statuary income

Taxable income = Assessable income – deduction

Tax = Taxable income*rate

Table 1 Calculation of tax for Mary for year 2021-2022

.png)

Notes:

a. Income tax

.png)

On the basis of this, Income tax = 23942

b. Medicare levy surcharge

It would be charged in addition to the Medicare levy. As per the provisions of ITAA 1997, Medicare levy surcharge would be charged to taxpayer if they do not have any private health insurance cover, and assessable income is more than basic threshold limit. The following rates is considered for Medicare levy surcharge –

.png)

Since, in this case, income of Mary is more than $90000, and not any private insurance cover is taken by her, therefore Medicare levy surcharge would be applicable. Rate of Medicare levy surcharge would be 1% by considering above threshold limits.

Medicare levy surcharge = 1030

c. Repayment of student loan

If the profit of borrower is more than $46620, then they have to pay particular percentage of loan amount. In this case, 7% is required to be repay by Mary as her income is exceeding $46620.

References

.png)

Finance Broking in Practice Assignment Sample

Question 1

Are your clients eligible for the First Home Owner’s Grant or stamp duty exemptions given they plan to buy in the same suburb as you? So Sweet organizational requirements requires you in addressing such questions to access the most recent figures from the website, including the link and the most recent data in your response.

Question 2

What documents would you request from your clients given their application for a mortgage loan? In what way do these documents meet organizational requirements?

Question 3

When serving this young couple, how would you fulfil your responsibilities as a mortgage broker under the anti-money laundering legislation?

Question 4

Given the fact that your clients have poor to adequate English language skills, what would you do to avoid committing unconscionable, misleading or deceptive conduct?

Question 5

Using the internet to find the most current products, decide which sort of a loan you would recommend to your clients and explain why.

Question 6

Would you recommend a portability feature within the loan for your clients?

Question 7

Calculate the loan-to-value ratio and discuss whether a lender would be prepared to lend your clients their desired amount on the basis of the information they have provided.

Question 8

What would be the monthly payments of an interest only loan be if the interest rate was 7% per annum?

Question 9

What would be the initial monthly repayments if you recommended a variable loan (principle and interest) if the interest rate was 7% and the loan term was 25 years?

Please review the illustrated example in chapter 5 for this calculation.

Question 10

How would you charge your clients? Please detail your remuneration arrangement in full in an email to your clients ensuring to sign off with your name.

Solution

Question 1

In general, the first home owner or buyer grant refers to a specific type of grant that is mainly for those who are buying their first home and just like other grants the first-time house owner or buyer does not hold a commitment to repay the grant. As being the financial broker in Australia, my clients named Peng and Mia both are definitely eligible for buying their first home in Australia. According to the reports for assignment help of Drukker (2021), to be eligible for the first home buyer grant any customer must need to buy a house or unit of townhouse which is under the value of $750,000. As in this case my clients want to buy a condominium or unit in a townhouse that values $ 410,000. The first home buyer grant is also applicable when the consumer earns income that is below $160,000 and as per their statement the couple has saved $ 95,000.

In order to take advantage of the grant Mia and Peng also lived in the nation over two years and in these years, they have been saved a fund of almost $ 1,00,000 and the rest of the money wants to acquire by a home loan. The first home buyer’s loans also include great benefits rather than other nominal bank loans.

Question 2

As per the rules of the Australian home loan system the documents are similar just as for the other loan grants. The documents needed to be carried in by my clients in order to meet the organizational requirements are birth certificate, certificate of citizenship, Medicare card, centre link pension card, utilities bill less than three months, notice of rates lesser than the three month and tax assessment notice less than 12 months. As per the statement of Nicholson et al. (2019), the documentation process of mortgage loans in Australia are divided mainly into four parts; proof of identification, ownership details or the documents related to property, documents related to customers income and expenses. The documents under the proof of identity are such as passport, birth certificate and driver license. Ownership details of properties, cars, and savings are coming under the documentation of properties and the income and expenses documentation process includes documents such as PAYG statement, recent payslips and monthly expenses from childcare to any other maintenance.

The related documents including the information of income and expenses are verified by the mortgage lenders through direct request from the consumers as these documents resolve the main four factors that are required for the verification such as gross annual income, assets and liabilities, credit history and down payment. For my clients I have been asked for the same including income for the last two years.

Question 3

The Anti Money Laundering and Counter- Terrorism Financing Act 2006 (Cth) refers to the primary piece of legastisation in order to respect the prevention and detection of terrorism financing and money laundering, (Singh and Best, 2019). As being a mortgage broker the primary and basic responsibility would be to serve my recent clients the best fitted terms based on borrower’s financial situation. As my clients are both young and currently planning to take residence inside an Australian township’s unit, my focus is to gather the right data and make a proper documentation system. The basic difference between a lender and mortgage broker, we are more responsible to give accurate advice towards the customers or clients so from that suggestion clients can make further and prominent decisions for buying a home. One of the important and other responsibilities of being a mortgage loaner is to also to provide the best options among other average options.

Underlying the act of Anti Money Laundering the active and superior responsibilities would be to assess and identify the money laundering risk, fraud and other potential suspicious activity for both client and mortgage broker, (Bailes, 2017). Monitoring and re-confirmation from the data provided by my clients and provided by me towards the clients is very much important in order to prevent any type of mortgage risk, fraud or scams.

Question 4

Under the Australian Consumer Law, it is described that any business or any type of business must not be conducted with unconscionable engagement. According to the report of Syuib (2020), it is stated that understanding and determining or identifying the unconscionable conduct is much important to reduce the risk from any misconduct. In this situation both my clients are from Taiwan and as they are poor in English in this situation it will be better to provide written documentation rather than verbal conversation. In this case, there is also a need of understanding the systems and laws regarding the mortgage loan in Taiwan, so this will benefit me in order to understand their understanding based on the laws. Also, in order to avoid being a victim of unconscionable conduct I will be using such legal process or procedures such as ensuring all agreements are in a written form, double ensuring for fully understanding all terms of transactions, explaining the terms and conditions by using easy language, seeks for the best deal and negotiate in order to achieve the best outcomes for me as well as for my clients.

For the agreement process that will be done by using plain and easy English, making sure the contract is not lengthy and not included harsh words or unfair terms.

Question 5

Based on the client recommendation after researching other relevant current products on the internet for my current clients the FHA or Federal Housing Administration Role would be the bests options among the other loan offers or products. It is highly beneficial for those borrowers who have low to moderate income and also the loan system demands for lower minimum down payment and lower credit scores rather than other conventional loans, (Troy, 2017). The loan includes so many advantages and it is very popular among first time home buyers. FHA loans are commonly issued by FHA approved banks and FHA institutions in order to properly evaluate the qualifications for the loan grant. The loan is also required to purchase mortgage insurance and premium payments are made to FHA. According to the Spitzer and Lambie-Hanson (2020), Compared to other home loans the FHA home loans include the lowest down payments of just 3.5 %.

In this loan procedure or system my client would need to get a qualifiable credit score of 580 but if they still don’t get success, they still can apply for FHA loans by making a down payment of 3.5% only if they scored between 500 to 579.

Question 6

The FHA loans already include many profitable features for the first-time house buyer but in this case, there are no other profitability features available for my clients. Portability or home loan portability refers to a feature that allows consumers to keep the same home loan product but change the supporting security of a property. The feature is also able to save the time and costs of refinancing. The home loan portability feature usually recommended to our clients when moving houses while client owe less than 80% on their mortgage. Loan portability also provides support to the clients to keep their existing loan such as current balance, interest rate and several other attached features and also change the security attached to a particular loan. In Australia, the first-time buyer only gets a discount of $10,000 when the clients are buying a new house worth $ 600,000 or building a new home valued up to $ 750, 00, (Bian et al. 2018). As per the section 245(a) loan, this program mainly for those borrowers who are expecting their income will be increased as or by these recent clients they are also expecting that in future they will earn an extra profit from their bakery business. In addition, there are small perks of profit included in the FHA loan process such as if my clients started to earn a good profit from their bakery business then can easily apply for the FHA’s limited 203(k) programs. Apart from FHA loan, there are several home or building loans in Australia that provides different interest amount and also emerge new and different type of portability. Variable interest rate loan is also known as basic and standard home loan for new residents in Australia. In this loan program, the rate of interest needed to pay by my clients would be set by the Reserve Bank of Australia and essentially the rate will either move high or low according to Australia’s Reserve Bank.

These programs help the clients to wrap up the $35,000 for additional renovation expenses into their mortgage loan and the service also includes other serviceable programs such as house repair, house improvement or any up gradation needed in house. As per the report of Whait et al. (2019), this particular loan system can also be applied by a single woman, just for example if Mia wants to buy a further property in future by all alone, she can easily apply for this loan and there is no extra documentation or verification needed.

Question 7

.png)

Based on the financial data or information provided by my customers, a lender would definitely provide many options regarding house buying. The couple are both intermediate in English so it is determined that if the lenders can communicate through by speaking English that will be beneficial for both in order to understand each other’s wants and needs. Based on the other information my both clients have stated that they want a big size house as per the view of their future perspectives but as they both do not have a proper stable income beside the profit, they earn from their bakery business it may be quite discomforting for the lenders. The couple has both stayed in Australia moreover two years and the resident they are looking for they want to spend over six months, as based on this relative information the lender can gain a trust ability in against the couple. Like mortgage brokers, lenders also want to see the proper documentation of the buyers in order to avoid any fraud or scam so by enabling the process of proper documentation the lender can actively sell their property without any further hesitation.

Question 8

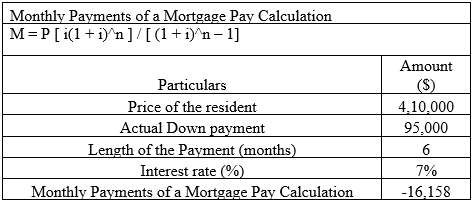

Based on the financial information provided by my client, only if the interest changes into 7% Annum the Mortgage payment would be $ (16,158) monthly.

Question 9

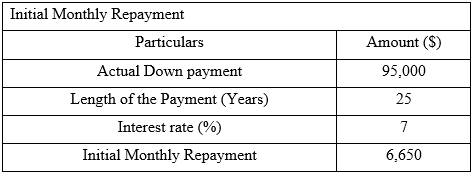

Based on the financial data and by following the calculation method from chapter five the calculation process is mentioned above. As in this calculation we have presumed that the actual payment or the value of P is $95,000 and the interest rate is 7% and the length of the payment is 25 years. The calculation of initial monthly repayment is the interest rate divided by the length of the payment and multiplied by the down payment and through this the calculation of initial monthly repayment is evaluated, (Ampofo, 2020). Based on the future situation for my client, if they increase the rate of the payment, they can sustain a long-term process and as well as it will be very beneficial for them. The situation of increasing the interest would be only done if the clients increase their future earnings or the profit from their bakery shop.

Question 10

For this new client Mia and Cheng by the determination it is acknowledged that the FHA loan would be the best and most appropriate loan system for them. As per the report of Young et al. (2021), it is found that the FHA loan is known as one of the most popular house loans for first house buyers. Just as many other mortgage brokers based on the total loan amount from 1 to 3% will be charged from the client. The remuneration would be done by both in written or paper documentation and as well as a soft copy will be sent to the email address provided by my client. The process would also be done through writing in easy English and the verbal communication will be done through based on both sides' understanding. The documents regarding the remuneration will be defined through specific contents and not using too lengthy words as my clients are not experts in english. In the both documentation there will mention the 0.5 percent commission charged from the total price of the house, based on the data the fees will be applicable for these clients. 0.5 % of $ 410000 means $2,050.

Reference List

.png)

Financial Decision Making Behaviour Assignment Sample

Description