TACC606 Accounting Business Report Sample

Name of the Student

Name of the University

Author’s Note

Table of Contents

Introduction:

Accounting for property, equipment and plant is considered an important element to record the right value of assets in the company’s financial statement. Generally, Net PPE value is determined by Gross PPE, plus Capital Expenditure, minus Accumulated depreciation. In this business report, ranges of measurement are being discussed. Different companies are recorded PPE following different accounting methods at the end of the financial report (Chadda and Vardia, 2020). However, the matter is most important to present such financial records in a most realistic and accurate way. Information about the significant portion of total assets of an entity will be discussed after assessing financial reports of two ASX listed companies: Goodman Group and Genesis Energy Ltd. In short, the objective of the business research report is to discuss and evaluate various disclosures related to PPE recoded by each company.

Evaluate PPE disclosure of the selected companies:

According to AASB116, all tangible items are measured as PPE if they are in use of the production process or in operation as a lease or purchased. However, this standard is generally recorded as PPE which expected to be used during more than the one accounting period. Thus better position of PPE indicates that the company was in good condition to exhaust their expenditures over the period. Goodman group, the chosen company measured their items of PPE at fair value of the cost at the recognition date. Interestingly, the figure of PPE has been increased over the last 3 years. In 2020, PPE was 115.60 $M and 128.7 $M was recorded in 2021. Here Goodman group leases their office buildings, office equipment and motor vehicles. Certain investment properties and developments classified as stocks are also built on land held under claiming interests of leaseholds. The company measures and recognizes an accurate application of asset and a “lease” liability at the date of initiation of lease agreement. The financial note clearly discussed that the chosen company initially measured the asset value at cost plus direct costs incurred considering estimating costs for reinstating the underlying asset or the place where it is situated, deducting any lease incentives collected. On the other hand, the lease liability of the company measured initially at the current value of the payment of rental which are yet to be made payment on the date of the commencement, less discounted incremental borrowing rate. After such initial measurement, the lease liability is determined at cost of amortization and interest expense.

In case of Genesis Energy limited, the valuation of PPE was based on a discounted cash flow model prepared by the management of the company. The recorded financial report in 2020 clearly disclosed that the asset value 3485.04$M which was high compare to the previous year 3367.70$M.Interestingly, the second chosen company valued their assets based on unobservable market data which is based on fair valuation method. Thus the valuation of the property of the company is based on a lot of assumptions. Depreciation of the assets is generally calculated in the method of straight line where the projected value of assets is being reviewed annually. Here the leased assets of the company are recorded at cost less accumulated depreciation and losses of impairment. The leased asset is being depreciated throughout the term of lease.

Validation to add items in PPE for that measured used:

It is completely valid to add items in PPE model of both the companies gives the measured used. During the scaling of the business, it is important to add one or several items of assets which might be obtained in exchange for a “non-monetary” asset or assets, or may be to position PPE between non-monetary and monetary (Prodanova,et al., 2022). The cost of such an item will be assessed at fair price unless the substitute transaction lacks substances related to commercial. However, the fair value of the adding items in PPE is reliable measurable if the possibilities of the several estimates within the range can be considerably assessed and practiced or the inconsistency in the range of fair value measurements is not considerable for that adding up assets.

Interpretation of total amount of PPE in the financial statement:

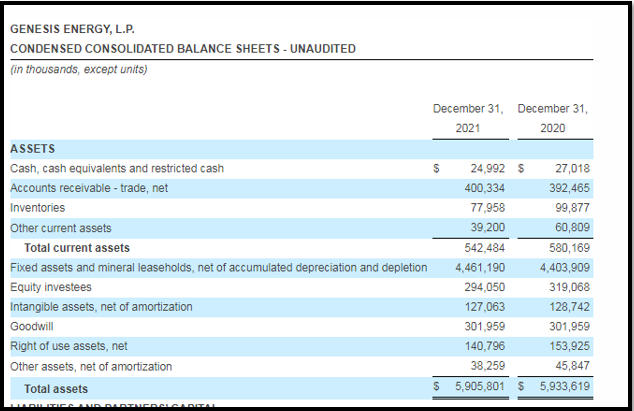

Plant, Property and Equipment are generally interpret the total amount long term fixed assets of the company which is tangible, identifiable and expected to generate an economic return for more than one operating cycle of the company. Here the total value of PPE can be derived from Gross PPE with adding up capital expenditures, less accumulated depreciation for the financial year. Based on the recent year’s reports of Genesis Energy LP, the company has been expecting to invest in fixed assets to sustain growth by aiding in operations.

.png)

(Source: Genesis-energy LP, 2021)

Initially, the carrying values of PPE items were valued at costs which are significant in relation to the total costs. Here Genesis Energy Company practiced revaluation method. Generation assets were revalued at 30th June 2021 to $3273.2 million resulting in a net gain of revaluation of $191.5 million. Here the carrying value of assets in June 2020 derived from $3177.2 at fair value of cost deducting accumulated depreciation and impairments which reduced the end carrying value of assets from $3662.5 to $3367.7 million (accumulated depreciation figure $294.9 million. It has been found from the financial report (specifically in Balance sheet) that assets were generated through following revaluation method $191.50 million. Interestingly, accumulated depreciation was increased from the year June 2020 ($535.1 million) to June 2021 ($570.7 million).

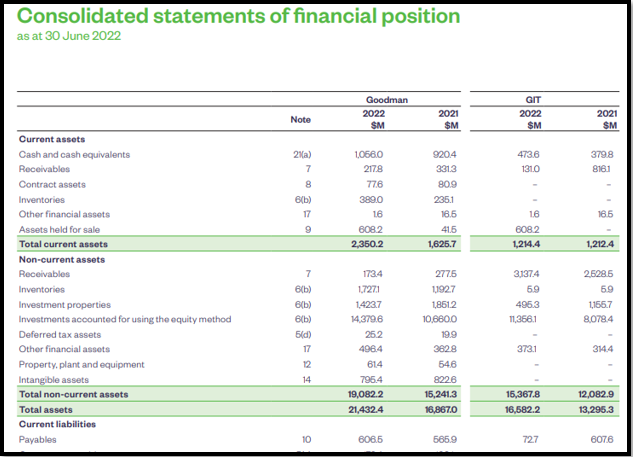

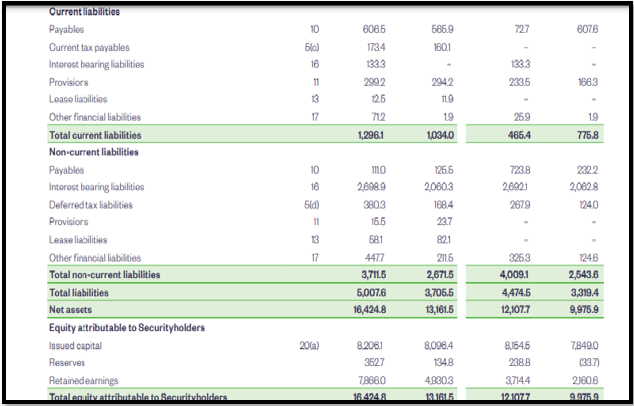

On the other hand, investment in plant, property or equipment of Goodman Group has been increased which disclosed in their financial report from $115.6 million to $128.7 million. Investment properties are carried at fair value. Here the fair value of stabilized investment properties of the Goodman Group is calculated considering present prices in an active market for similar properties in the same condition and location and also allowing for same lease and other contracts. The “carrying” value of PPE at the end of the financial year interprets the amount of newly acquired assets list of capital expenditure, and net gain from fair value adjustments and so on.

.png)

(Source: Goodman Group, 2022)

The value of assets are initially measured at cost plus any direct costs associated like labour costs, to restore the underlying assets less any lease incentives received over the particular period. In this way, total amount for PPE is being interpreted from the statement of financial.

Measurement comparison used by the several companies for same type “items” in PPE and finding inconsistencies, if any:

PPE is measured as per revaluation model or cost model by many companies considering the benefits as per the company’s financial requirements over the period (Karim, Islamand Bhuyan, 2020). PPE firstly recorded at its costs, consequently priced either using a revaluation model or cost and depreciated later, which indicates that such “depreciable” amount can be comprised on a methodical basis over the useful life of PPE. The carrying amount of PPE under the cost model, is generally being measured at its cost less accumulated loss and accumulated depreciation for impairment of assets. Goodman Group has been used such cost model in contrast of Genesis energy LP which used revaluation model for measuring PPE items for their company. Under the revaluation model, an asset is recorded at the revalued amount less depreciation which is accumulated and any losses of impairment. Generally the management of the company uses this revaluation method to ensure most accurately the fair value of PPE (Prodanovaet al., 2022). However, the business entities can switches from cost model to revaluation model, but there is no need for applying this change in the accounting policies. The chosen company, Genesis energy has previously experienced fluctuation in fair value of some items of PPE. Thus, all items of property, plant, and equipment was then revalued by the management and reported accordingly. Compare to cost model, the revaluation model helps to avoid inconsistencies of assets and the reporting figure in the financial statements that ascertain different values or cost at different date. Revaluation gain is recorded in the balance sheet as equity as a separate capital reserve, called “revaluation surplus”. On the other part, revaluation loss is being booked in the “statement of income” as considering expense. However, if there is some balance in the revaluation surplus presents in the accounts of the company from any previous revaluation gains of the same asset, that surplus of revaluation amount will be adjusted first and accounted for. Any excess revaluation loss will be recorded in the statement of income of companies. In that circumstances and for treating those surpluses and losses, the company will measure their PPE items of similar categories under revaluation model. As cost model is relatively simpler than other model of PPE measurement and it is based on cost of historical principles, inconsistency can be found in the fair value changes of PPE over the period.

Considerable factors that important for setting up accounting policies for the company relating to PPE:

Accountants need to evaluate various factors before establishing company accounting policy relating to PPE. In case of structuring of PPE model for the company, all the factors such as useful life of the asset, depreciation method for PPE, correctly determination of value of assets, policy for PPE impairment and so on.

Detailed discussion of above mentioned factors are as follows:

Functional life of an asset: Useful life is generally indicates approximate efficacy period imposed on a range of the business entity’s properties. This information provided by the accountant is valuable for setting up accounting policies to PPE because useful life of assets forecasts end at the point where assets are anticipated to become outdated. The design of the valuable life of each asset, premeditated in years can be practiced as a reference to make the depreciation plans for inscribing outflows associated to investment purchase of goods for the company.

Depreciation method for PPE: Choosing right depreciation method for PPE valuation is significant as the accounting standard defines such depreciated value is a systematic allocation of fund over its useful life which can be used for cash collection or capital generation for the business. The carrying amount of PPE items can be measured by applying “straight line” method or reducing method or unit of production method. For instance, Genesis Energy uses the straight line method for valuing long lived assets to cover the total costs of an asset over its lifespan instead of recovering their purchase costs on an immediate basis. In accelerated method for PPE calculation, which generally creates more depreciation in early phase of the fixed asset. It considers the point of income tax which is a reasonable factor to make difference the value of assets for this reason.

Appropriate asset valuation: It is indeed an important factor for PPE to make an accurate asset valuation which is all about setting the right value of property including inventories, houses, equipment or land. It is typically happened when the management of the company is to make a decision to sold, taken over or insured their fixed assets. Such perfect valuation thus is significant factor for PPE to generate maximum cash for the growth of the business in future.

Impairment policy of PPE: As prescribed in accounting policy, an accountant must not carry an asset in the firm’s financial statements an exceeding highest amount which might be recovered through its sale or use. If the carrying amount of asset exceeds the recoverable amount, the asset is described as impaired then (Hladika, Gulin and Bernat 2021). Thus the accountant must maintain such impairment policy to provide the right information to the stakeholders of the company. In case the accountant find its fair market value of PPE items is less than its carrying amount then, it should be recorded as impairment loss for that difference. Therefore, accountant practitioners must be practiced their impairment policy of PPE with full conviction and clarity in books of accounts.

Initial and consecutive recognition criteria of PPE: An Accountant must initially measure their PPE items at its costs. However, there is a choice of subsequent measurement. The criteria of the recognition must be fulfilled with discussing the matter with the management of the company. For instance, Genesis Energy LP used revaluation model for the PPE recognition after initial measurement of assets at its costs. On the contrary, Goodman Group used cost model and allocate depreciable asset value on a periodic basis over its useful life. Here the fair value variations were being ignored while accounting those records into book.

Detailed observation on succeeding measurement of PPE:

Initially PPE must be recorded at its cost which includes purchase price of the asset adding up duty of import, directly associated costs (cost of installation, freight in, site preparation cost, testing, professional fees, and inescapable costs such as disassembling, removing and reinstating the site cost. Policy setters however, will definitely choose either the cost or the revaluation model in the subsequent phase of measurement of PPE. Under paragraph 6 of AASB 116, items of PPE are tangible in nature and expected to be used for more than one period. Thus subsequent measurement policies of PPE need to have an immense importance for the accounting practitioners. For the purpose of accounting, entities need to be measured subsequent expenditures for determining if it may be capitalized or treated as expense at the time of occurrence.

However, the asset recognition criteria must be fulfilled in case of subsequent PPE expenditures. It means that future economic benefits or the ability to contribute to the objectives of the entities for delivering goods or services for one that one accounting period can be capitalized. On the contrary, subsequent measurement for that expenditure on an item of PPE that fails to meet the recognizing criteria of asset at paragraph 7 of AASB 116 shall be considered as expense and positioned in the income statement of the company’s financial records at the end of the reporting period. Under the model of cost, if fair value calculates correctly, the value of the asset then should be calculated at its cost value, subtracting “accumulated depreciation” less “loss of impairment”.

To categories most PPE, AASB specifies the accounting treatment of PPE while recording the books of accounts in the financial statement at the end of the financial year. The cost model incorporates items of PPE being held at a lower price of depreciation and loss of impairment. On the other hand, the carrying amount of PPE whose fair price can be quantified reliably utilizing the revaluation model. In other words, where reliable cost measurement can be attained it is like that the expenditure would produce future economic benefits in case of subsequent expenditure on an item of PPE are for a part of replacement, major inspection, and enhancement or for safety or environment equipment. Here the fluctuations of fair value can be measured and accounted for at the end of the financial period. Under this model, the accountant shall take asset’s carrying value at its PPE’s fair value at the time of the revaluation less any following accumulated depreciation and loss of impairment. In other words, the asset is carried at the rate of revaluation if the model of revaluation is being practiced. This formula of measuring PPE items under this revaluation model is the fair value less asset’s cumulative depreciation along with any lack of impairment.

Recommendations to accounting standard setters related to PPE measurements:

Perfect policy choices must be taken considering the use of the PPE items of an entity. Interestingly, accounting standard setters are already discussed that such assets must be measured considering either the expense model or the model of revaluation. This is completely a management oriented decision whether which model will be choices later in the subsequent expenditure measurement of PPE items. As per the cost model, if fair value can be measured truthfully, the asset shall be priced at its cost subtracting “accrued depreciation” less loss of the value of impairment. On the other hand, the revalued sum is equal to fair value at the time of revaluation less following up any accrued losses of impairment and depreciation under the method of revaluation model. According to AASB 116, it is recommended to practitioners that all assets in the same group can be re-examined if one value is revalued. For instance, if the management of an entity wishes to revalue its equipments or buildings, and recorded to have five buildings and ten machineries, then it will re-evaluate all number of equipment and buildings of that entity. For simplicity reason, the cost model is always preferred and easy to measure PPE items for subsequent measurement purpose over revaluation model. However, an important recommendation for changing one measurement model to another can be taken place by any entity for better presentation of fluctuations of fair value where cumulative depreciation is calculated and any lack of impairment.

Conclusion:

The above report clearly discussed principles considered for identifying items of PPE as prescribed the accounting standards. However, different companies are followed different policy to record subsequent expenditures of entities after the initial measurement of PPE at cost. The above chosen both companies are followed different measurement policy for their PPE items. It makes it rational for PPE to be calculated at “Cost plus other accumulation” for obtaining the item of PPE’s definite cost for prospective purposes of valuation. The sum of the less accrued depreciable asset moves to the statement of performance (B/S) and the fee over the period goes at a cost to the P/L statement. Undeniably, both the chosen firms attain the right depreciation amount of assets and fulfilled requirements of overseas reporting from any assessment. Thus PPE reporting and measurement process is vital for any business firms at the financial year end.

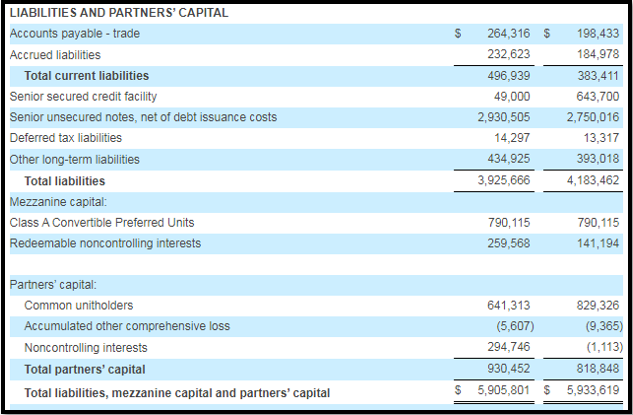

Appendix:

Goodman Group Balance Sheet 2021-2022

Genesis Energy, LP Balance Sheet

References:

.png)

- HDS310 Human Rights and Advocacy Assignment

- ICT102 Networking Report 3

- MGT607 Innovation Creativity Entrepreneurship Assignment

- STATS7061 Statistical Analysis Assignment

- MIS501 Principles of Programming Learning Activity Assignment

- CPC40120 Certificate IV in Building and Construction Assignment

- CAM529 Introduction To Public Health Assignment

- ACC2CRE Financial Accounting and Reporting Assignment

- CSIT985 Social Media for Organization Innovation Essay 2

- MKG203 Digital Marketing Communication Assignment

- PSYC1003 Understanding Mind Brain and Behaviour Assignment

- Data4400 Data Driven Decision Making and Forecasting IT Report

- LAW1081 The Individual and The State Formative Assignment

- BSBSTR601 Manage Innovation and Continuous Improvement Assignment

- AC7026 Master of Public Health Nutrition Assignment

- Organisational Behaviour Assignment

- MIS608 Agile Project Management

- Auditing Coursework Assignment

- NRSG367 Transition to Professional Nursing Assignment

- CIS7030 Geospatial Analysis Assignment

.png)

~5.png)

.png)

~1.png)

.png)