BE167 Accounting and Finance for Managers Assignment Sample

Assignment Brief

(2,500 WORDS, excluding list of references)

All submissions must be presented in typescript (Word format), 12pt, 1.5 line spacing. Deadline for submission to FASER: 16 December 2022, 10:00hrs (Week 11)

AIM:

This assessment aims to provide you with an opportunity to reflect on the concepts you have learnt during the course of Accounting and Finance for Managers lectures and seminars. It will assist you in developing your ability to apply concepts to practice in the light of your experience while qualifying for the master’s degree.

You are required to write a report analysing the financial performance of a selected publicly listed company (please refer to submission guidelines for the choice of the company) for the latest THREE consecutive years, as a minimum. The report should include the following:

REQUIREMENTS:

a) Provide an introduction with a background of the business in question (e.g. strategy, prospects, competitor analysis, SWOT analysis). (20 marks)

b) Calculate at least three profitability ratios of your choice to support your analysis. Critically evaluate the profitability position of the company. (20 marks)

c) Calculate at least three efficiency ratios of your choice to support your analysis. Critically evaluate how the resources of the business are managed.

d) Calculate at least three investment ratios of your choice to support your analysis. Critically evaluate the investment position and potential opportunities of the company.

e) “Although ratios offer a quick and useful method of analysing the position and performance of a business, they suffer from problems and limitations” (Atrill and McLaney, 2019, p. 234). Do you agree with this statement? Discuss with examples from the above analysis to support your argument. Briefly indicate the alternative approaches to overcome limitations of ratio analysis.

Submission Guidelines:

This work should be presented as a report type – i.e. guiding the reader effortlessly through the arguments you present (e.g. introduction, development, final considerations – all that making use of subheadings, again, to guide the reader (shareholders, in this case). The purpose of the guideline offered below is to help you to organise your report (rather than to limit your creativity); and also, to provide you with a marking scheme. That is to say, you do not need to actually indicate the letters (a,b,c,...) when presenting the report. Consider that you are providing information to the shareholders to make financial decisions.

- Read updated literature on concepts, methods and tools for Analysis and interpretation of financial statements.

- you are expected to choose one company from the ones below in analysing financial statements:

1. Clarkson PLC https://www.clarksons.com/home/investors/

2. Marshalls PLC https://www.marshalls.co.uk/investor

3. Spirent Communications PLC https://corporate.spirent.com/investors

4. Morgan Sindall Group PLC https://www.morgansindall.com/investors/reports- and-presentations

Solution

1. Introduction

Clarksons is one of the reputed companies which provide robust solutions for shipping companies. The company's brief introduction is presented in the report along with its strategies, future prospects, competitor analysis and an internal evaluation of the company using the SWOT matrix. The report also analyses the performance and financial health of the company by utilizing several ratios. Lastly, the report discusses the limitation of these ratios and provides an alternative considering their limitations for assignment help.

1.2 Company Background

Clarksons is a firm that works across departments to ensure that everything it does is supported by data, made possible by technology, and carried out by the most capable workers in the industry (Clarksons.com, 2022). The breadth of the company's reach, the quality of its connections, and the comprehensiveness of its service offering combine to produce exceptional outcomes. As a long-term business associate, it advises customers on the best course of action throughout the shipping process (Clarksons.com, 2022).

1.3 Company Strategy

The company's strategy is to strengthen its position as a leading provider of services throughout the marine, offshore, commerce, and energy industries to provide its customers with tailored business strategies that help them make more informed choices (Clarksons.com, 2022). The company's commitment to Renewables and sustainability competence puts it in a prime position to spearhead this crucial shift as the market moves inexorably toward an increasingly sustainable future (Clarksons.com, 2022).

1.4 Future Prospects

The company's prospect is to adapt to the ever-changing needs of the global marine, offshore, commerce, and energy industries via its market-leading technologies and analytics to facilitate wiser, healthier international trade (Clarksons.com, 2022).

1.5 Competitor Analysis

.png)

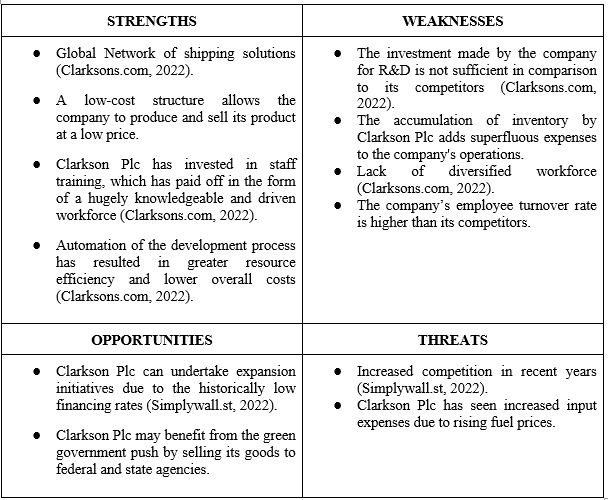

Table 1: Clarksons’ Competitor Analysis

(Source: Created by author)

1.6 SWOT Analysis

Table 2: Clarksons’ SWOT Analysis

(Source: Created by author)

2. Profitability Ratio Analysis

The profitability ratio compares operating expenses, sales, and equity to illustrate Clarksons' capacity to generate profits. A greater ratio is preferable since it indicates that Clarksons is well-positioned to sustainably generate profits (Bigel, 2022). In light of the importance of profitability ratios, the following three ratios are calculated to determine Clarksons' profitability.

2.1 Gross Profit Margin

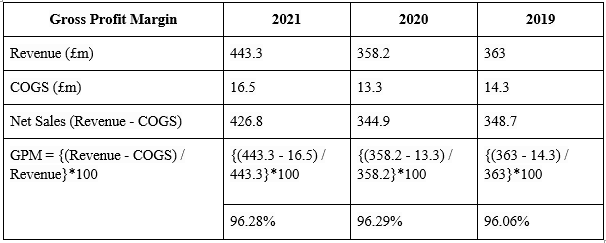

The term "gross profit margin" refers to the amount of money left over after expenses have been subtracted from sales. The number is standard and essential as a fundamental indicator of Clarksons’ financial health (Bigel, 2022).

Table 3: Clarksons’ GPM Analysis

(Source: Clarksons.com, 2022)

It can be observed from the above table that Clarksons’ revenue in FY 2020 declined, which is directly attributed to the pandemic. For example, ocean freight from Chinese ports declined by 10.1% during the pandemic. Air freight volumes declined by 19%, causing a significant halt in the logistics industry (Ifc.org, 2021). However, even with the fall in revenue during the pandemic, Clarksons maintained a consistent GPM of 96% throughout the analysis period with slight fluctuations. It, therefore, indicates that the company is in good financial health and has the capacity to maintain its profitability.

2.2 Return on Assets

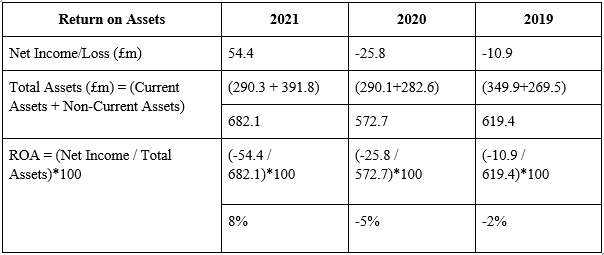

Clarksons’ capacity to create profit from its assets may be measured by calculating its return on assets. In other words, Return on Assets (ROA) is a metric used to assess how effectively Clarksons’ management is able to transform its entire balance sheet assets into net income (Hilkevics and Semakina, 2019).

Table 4: Clarksons’ ROA Analysis

(Source: Clarksons.com, 2022)

It is evident from the above table that the company incurred massive losses during FY 2019 and 2020. It can be seen that in FY 2019, the company incurred a £10.9 million net loss, and in the following FY 2020, it incurred a £25.8 million loss (Clarksons.com, 2022). It can also be observed that the company’s total asset has also decreased by £46.7 million from the previous year. The fall in total assets is primarily due to the decrease in right-of-use assets Clarksons.com, 2022). Moreover, during the pandemic, container freight rates surged dramatically, which led to losses. Higher than-average prices were charged when shipping to South America and western Africa (Unctad.org, 2019). Freight rates connecting Asia and the eastern coast of North America increased by 63% between 2020 to early 2021, while prices between China and South America increased by 443% (Unctad.org, 2021). However, as the pandemic subsided, the logistics industry recovered, which is evident from the increased net income of the company and positive ROA of 8%.

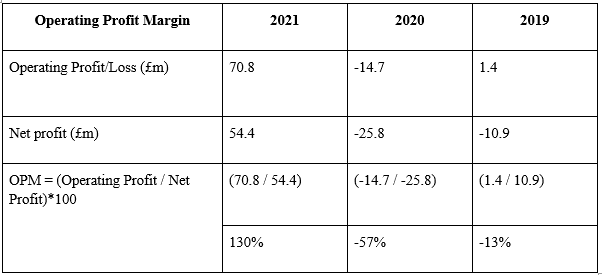

2.3 Operating Profit Margin

Operational performance metrics (OPMs) measure how well Clarksons’ operations are managed. A healthy business, for instance, is one that has higher operating profit growth than sales growth (Faello, 2015).

Table 5: Clarksons’ OPM Analysis

(Source: Clarksons.com, 2022)

It is evident from the above table that the company had an operating profit of £1.4 million; however, due to the net losses, the company's OPM stood at -13% in FY 2019 (Clarksons.com, 2022). It worsened during FY 2020 when the company incurred operating losses of £14.7 million. It is due to a significant increase in administrative costs, which included data populating, research spending, and employee training (Clarksons.com, 2022). Expenses for depreciating intangible assets having limited lifetimes, such as a company's Forward Order Book on an acquisition and Trade name and non-contractual commercial relationships (Clarksons.com, 2022). However, in FY 2021, the company incurred operating profits of £70.8 million. It was primarily due to increased revenue in FY 2021, which was greater than the administrative expense, even though it increased in FY 2021.

3. Efficiency Ratio Analysis

It examines the extent to which Clarksons makes effective use of its assets and liabilities. Clarksons may use this information to gauge whether or not its investments in people and machinery are yielding satisfactory returns (Faello, 2015). In light of the importance of the efficiency ratio, the following calculations are conducted to determine Clarksons' efficiency in managing its resources to generate profits.

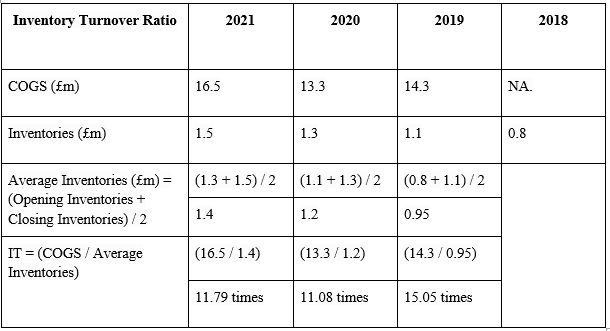

3.1 Inventory Turnover Ratio

The inventory turnover ratio quantifies how often Clarksons sells and restocks its goods over a certain time frame. If Clarksons has a high inventory turnover ratio, it means it efficiently moves through its stock (Bigel, 2022).

Table 6: Clarksons’ IT Analysis

(Source: Clarksons.com, 2022)

It can be observed from the above table that Clarksons' IT ratio has gradually decreased over the three FYs. From FY 2019 to FY 2021, the company's IT ratio decreased from 15.05 times to 11.79 times. It implies that the company is not efficiently moving its stock in the given period. A declining IT ratio means that the company's inventories are being held back and increasing its cost of goods sold, as observed in the above table (Hilkevics and Semakina, 2019).

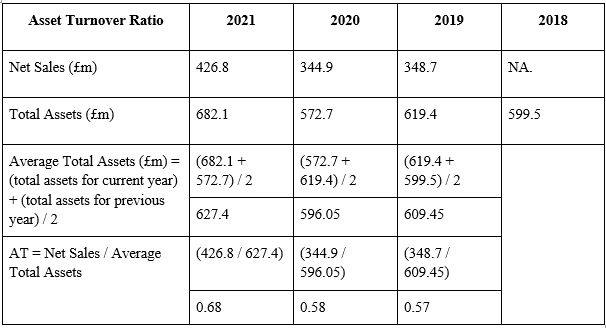

3.2 Asset Turnover Ratio

The asset turnover ratio gives insight into the Clarksons’ productivity. In a nutshell, it shows how much money Clarksons is making for every dollar it has invested in its physical assets (such as land, structures, machinery, cash on hand, accounts receivable, and inventory) (Bigel, 2022).

Table 7: Clarksons’ AT Analysis

(Source: Clarksons.com, 2022)

The AT ratio of Clarksons is below the standard ratio of 1. It means that the company is able to generate only £0.57 for every £1 worth of the asset. It is a bad sign for the company as it cannot maximise its assets to generate revenue greater than £1 against its assets (Bigel, 2022). It is because the company has increased its assets over the period, which is not proportionate to its revenue growth. The primary reason for the company's total assets to increase is the increase in its accounts receivable, as observed in the financial statement. According to the financial statements, the number of accounts receivable increased due to the grouping of past dues (Clarksons.com, 2022).

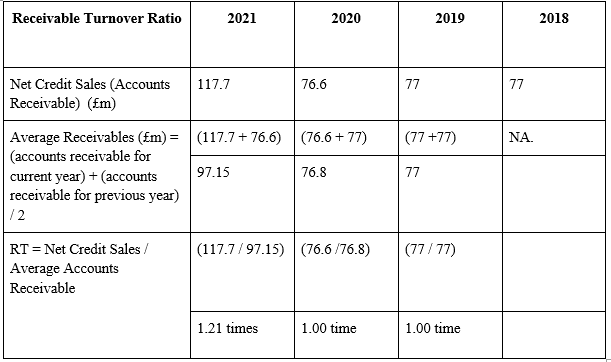

3.3 Receivable turnover Ratio

It's a crucial measure of Clarksons' economic and operational health. The Receivable Turnover ratio reveals how often receivables have been collected throughout a certain accounting time frame (Faello, 2015).

Table 8: Clarksons’ RT Analysis

(Source: Clarksons.com, 2022)

As observed in the previous analysis, there is a significant increase in the account receivable of the company, which is directly attributed to the grouping of past dues (Clarksons.com, 2022). Similarly, it can be observed in the above table as the RT ratio has increased in FY 2021 to 1.21 times from 1 time in FY 2020 and FY 2019. It was also evident from the IT ratio that the company's idle inventories have increased over time which attributes to the increase in the RT ratio in FY 2021.

4. Investment Ratio Analysis

The investment ratio, often called the liquidity ratio, indicates Clarksons' capacity to pay its loans when they come due (Bigel, 2022). It means that liquidity ratios reveal how fast Clarksons can turn its existing assets into cash, allowing it to meet its obligations in a timely manner. Therefore, this ratio is significant in determining a company's creditworthiness and financial stability (Bigel, 2022).

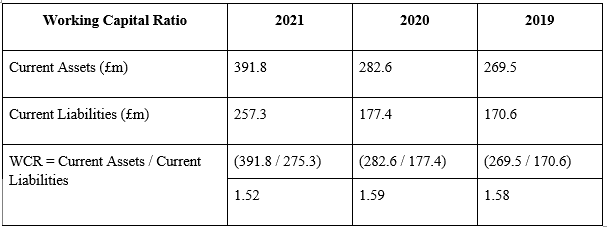

4.1 Working Capital Ratio

Clarksons' working capital is described as the difference between its current assets and liabilities. It measures how easily the company can cover its immediate debts with money on hand.

Table 9: Clarksons’ WCR Analysis

(Source: Clarksons.com, 2022)

It is evident from the above ratio analysis table that Clarkson's current assets are more than its current liabilities. In FY 2019, 2020 and 2021, the WCR stood at 1.58, 1.59 and 1.52, respectively. It can be observed that the company has maintained a sustainable working capital ratio throughout the period (Bigel, 2022). It indicates that Clarksons have sufficient current assets to pay off its short-term liability when the due date comes. In other words, the company has £1 current assets to pay off its £0.52 short-term liabilities in FY 2021 (Bigel, 2022). Therefore the company is in good financial health.

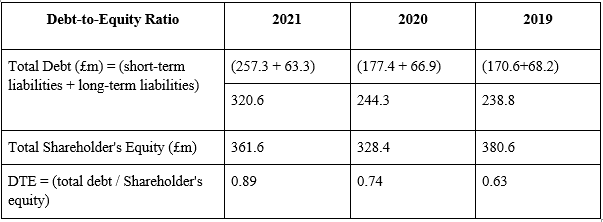

4.2 Debt-to-Equity Ratio

The Debt-Equity Ratio is a Financial measure that determines how much debt Clarksons has in relation to its equity. This ratio is used to calculate how much of the total funding came from outside investors in the form of debt vs equity (Hilkevics and Semakina, 2019). The debt-to-equity ratio is a common measure of a company's financial health; a lower ratio is preferable. It is recommended that debt-to-equity ratios not exceed 2:1. (Hilkevics and Semakina, 2019).

Table 10: Clarksons’ DTE Analysis

(Source: Clarksons.com, 2022)

It is evident from the above analysis that the company has a good debt-to-equity ratio. A good debt-to-equity is when ratio is below 1. It means that the company has more liabilities and is funded by them. It is a good indicator of a company's financial stability as the company has an optimum level of liabilities and equity (Hilkevics and Semakina, 2019). Conversely, if the company highly depended on liabilities to fund its operations, it significantly raised the risk of bankruptcy in times of financial crisis.

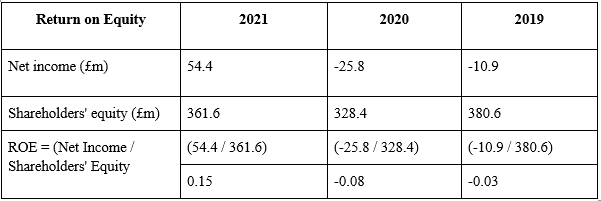

4.3 Return on Equity

One way to evaluate Clarksons' ability to create returns for its shareholders is to examine its return on equity ratio. Investors may see how much cash Clarksons has stashed away after paying all its expenses by calculating the company's Return on Equity (ROE).

Table 11: Clarksons’ ROE Analysis

(Source: Clarksons.com, 2022)

The above analysis shows that the ROE in FY 2019 and FY 2020 were negative at -0.03 and -0.08, respectively. It is primarily due to losses incurred in the two FYs, as observed in the above table. It means that during the two FYs, the investors lost their investment in the company. However, in FY 2021, the company had a positive ROE of 0.15, which means that the investors earned £0.15 for every £1 invested in the company (Hilkevics and Semakina, 2019). It pimples that the company has gradually become profitable for the investors. However, the ROE is not good enough for new investors to be attracted to make an investment in the company.

5. Discussion

Both professionals and researchers in the field of accounting make substantial use of ratios calculated from a wide range of financial variables when analysing financial statements. Inaccuracies may occur while using financial ratios (Hilkevics and Semakina, 2019). Anyone who uses financial accounts, not only those studying or working in accounting, should be aware of the difficulties and cautions that come with relying on financial ratios (Bigel, 2022).

Users of financial statements may utilise financial ratios to better understand the health of a firm and spot potential issues with its operations, liquidity, debt, or profitability (Faello. 2015). Financial ratios are useful for determining the level of risk associated with a company since they allow for comparisons to be made between similar businesses and assessments of performance. In assessing Clarksons Plc's financial health, the statistics mentioned earlier proved their worth.

However, from the viewpoint of those who use financial statements, the restrictions of financial statement ratios reduce the financial outcomes of different companies from being directly compared (Bigel, 2022). For instance, if one company decides to go from the more common LIFO to the less common FIFO method of inventory valuation, it will no longer be comparable to other companies. As a result, it becomes more difficult to compare companies' inventory turnover rates (Faello, 2015). Furthermore, because readers of financial statements cannot see a company's internal accounting-related choices, alternative methods must be used to reduce the likelihood of inaccurate accounting statistics in calculating financial ratios (Faello, 2015).

The impact of outliers on statistical findings is a significant problem when dealing with financial ratios, at least from the researcher's perspective. The term "outlier" describes a data point that doesn't fit in with the rest of the sample (Hilkevics and Semakina, 2019). Financial analysts may replace ratios using regression analysis. For instance, the Capital Asset Pricing Model (CAPM) attempts to approximate the relationship between the expected return on an asset and the market risk premium (Zerbib, 2022). The research may also be used to foretell a company's future performance or the returns on various investments (Wihartati and Efendi, 2021). The study may also be used to predict how a company will do in the future or to predict the returns on a variety of assets (Wihartati and Efendi, 2021).

References

.png)

.png)

- HLTWHS004 Manage work health and safety Assignment

- BFA704 Work Placement Assignment

- ITBO201 IT for Business Organisations Assignment

- SRM751 Principles of Building Information Modelling Report 1

- ENT201 Sales and Negotiation Strategies Assignment

- IND301A Industry Consulting Project Assignment

- LAW6000 Business and Corporate Law Case Study

- PUBH6007 Program Design Implementation and Evaluation Assignment

- PMN610 Project Management Principles Assignment

- Wind Turbine Power Production Estimation for Better Financial Agreements

- COIT20251 Knowledge Audit for Business Analysis Report

- MBA402 Governance Ethics and Sustainability Case Study 2

- PSYC20036 Assignment 3

- PPMP20009 Project Management Report

- MGT501 Business Environment Assignment

- CSE5CRM Cyber Security Risk Management Program Assignment

- MGT502 Business Communication

- MBIS4010 Professional Practice in Information Systems Essay

- MGT605 Business Capstone Project Report 2

- MIS607 Mitigation Plan for Threat Report

.png)

~5.png)

.png)

~1.png)

.png)