Order Now

- Home

- About Us

-

Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

-

Assignment Writing

-

Resources

- Referencing Guidelines

-

Universities

-

Australia

- Asia Pacific International College Assignment Help

- Macquarie University Assignment Help

- Rhodes College Assignment Help

- APIC University Assignment Help

- Torrens University Assignment Help

- Kaplan University Assignment Help

- Holmes University Assignment Help

- Griffith University Assignment Help

- VIT University Assignment Help

- CQ University Assignment Help

-

Australia

- Experts

- Free Sample

- Testimonial

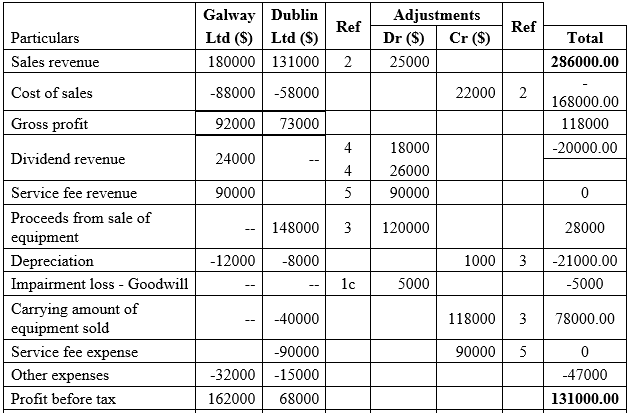

ACCT6005 Company Accounting Case Study Sample

Context:

• Assessment coverage: Module 1-2 Fair Value adjustment and Intra group transactions.

• You are required to demonstrate: the assumed knowledge and skills from Module 1 Introduction and Principles of Consolidation; understanding and ability to account for fair value adjustments and intra group transactions.

• You are able to prepare: acquisition analysis, adjustment entries for group using the consolidation worksheet, and consolidated financial statements.

• You are able to recommend and communicate strategic recommendations regardingfair value adjustment entries.

Instructions:

• Show all relevant workings where required.

• Combine the answers for both Part A and Part B into one assessment document.

Solution

Part A

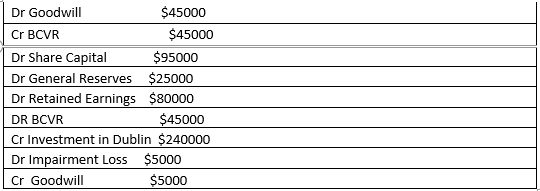

Point 1: Goodwill

1. The accounts that would get affected from the impairment of Goodwill are Goodwill, Retained Profit, BCVR, Investments in Dublin.

2. The above accounts have not been adjusted to eliminate the intragroup impairment of Goodwill of $5000.

It is to be further noted that Goodwill treatment would not get affected from the tax rate.

The individual companies would have passed the following entries before consolidation are as follows:

3. The Elimination Entry would be for the stated situation are as follows

4. If this error is not corrected, goodwill would be shown at book value instead of showing at fair value leads to which the value of assets would be shown at overstated value by $5000. As per the IAS 36 goodwill should be impaired if the book value is less than the fair value of the market. In the currents scenario goodwill of the Dublin Ltd has been impaired by $5000 and this should be shown at the consolidated balance sheet. Since the goodwill which has been acquired during the time of acquisition has been impaired the same should be reduced by $5000 to show the net and true effect. For Assignment Help Further, any impairment or any improvements in the valuation of the goodwill would be capitalized as such treatment is not regular in nature. However, in the current scenario as the impairment of goodwill has risen after acquisition hence the same should be reduced from the Retained Earnings. Also, impairment expense is the different type of expense for the company and hence this should not mix up with any other expense. (Glaum, Landsman, Wyrwa, 2018)

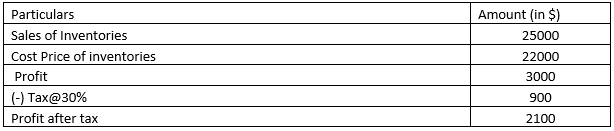

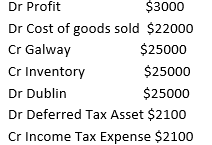

Point 2: Sales of inventory

1. The accounts that would get affected from the sales of inventory in between the companies are Cost of goods sold, Sales, Inventory, Net Profit.

2. The above accounts have not been adjusted to eliminate the intragroup unrealized profit of $3000.

The individual companies would have passed the following entries before consolidation are as follows:

3. Elimination entries for the current adjustment is follows

4. If this error is not corrected, inventory and profit would be shown at inflated value. Further, the overall value of the assets would reflect at the inflated values as the value of the inventory has been inflated. On the other side liabilities would be inflated due to the profit arrived from such sale. The intra group adjustment should be made appropriately so that net effect can be shown. Therefore, such adjustments have to make to deliver true and fair balance of the financial statements so that the value of assets and liabilities should reflect at correct balance. The profit would change for the company as the profit from the sale of inventory would reduce from the total profit. (Dubolazov, Simakova, Dubolazova, Makarov, 2020)

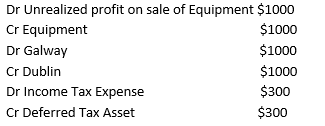

Point 3: Sale of Equipment

1. The account that would get affected from the sale of equipment in between two companies are Galway, equipment, Profit on equipment, Dublin.

2. The above accounts have not been adjusted to eliminate the intragroup unrealized profit of $5600. The sale of equipment between both the companies should be excluded as the same is considered under intra-group transaction.

.png)

The individual companies would have passed the following entries:

.png)

3. Elimination Entry for the current adjustment is follows

4. If the above adjustment has not being made then assets and liabilities both would be shown at inflated values. The correct value of the equipment would be ignored and the unrealized profit that should be ignored has taken into consideration. Hence, net gain after tax should be excluded for the purpose of correct evaluation of the equipment. (Dutt, Nicolay, Spengel, 2021)

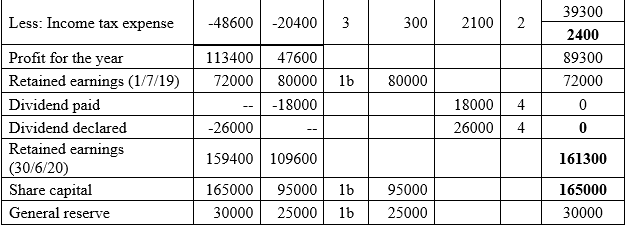

Point 4: Dividend

1. The account which have been affected Dividend received, Dividend Payable, Dublin, Galway.

2. The above accounts have not been adjusted to eliminate the intragroup adjustment of $18000. The date of acquisition is 1st July 2019 and dividend paid on September 2019 which is the part of post-acquisition profit and hence should be credited in the profit and loss account. Any revenue occurred after the acquisition should not be capitalized. Further, Galway Ltd has declared the dividend as on May 2020 and the same would be paid on October 2020.

The individual companies would have passed the following entries:

.png)

3. Elimination of entries for the current adjustment is follows

.png)

4. If the above adjustment has not being made then assets and liabilities both would be shown at inflated values leads to which the balance sheet of the company would not deliver true and fair statements. Further, dividend payment and received would show double effect which is not correct as per the international accounting standard. There would be no difference in the accounting of net profit as dividend is being paid after arriving at profit. The intra group transactions should be adjusted while preparation of the consolidation account so that the financial statement should deliver true value. As per the international accounting standard while preparation of the consolidation net effect should be shown.

Point 5: Charge of service Fees

1. The account which have been affected Galway, Dublin, Service Revenue, Service Expense.

2. The above accounts have not been adjusted to eliminate the intragroup adjustment of $9000 ($90000 x 10%). AS 90% of $90000 has already paid by Dublin Ltd to Galway Ltd.

The individual companies would have passed the following entries:

3. Elimination of entries for the current adjustment are as follows:

Dr Service Revenue $90000

Cr Service Expense $90000

4. If the above adjustment has not being made then assets and liabilities both would be shown at inflated values leads to which the balance sheet of the company would not deliver true and fair statements. In the current scenario, Dublin Ltd has purchased services expenses from Galway Ltd which leads to creation of creditors in Dublin Company and creation of debtors in the account of Galway Ltd. To show the net effect both the transaction should be eliminated. However, the value of the net assets and equity would not change for a group but the assets and liabilities would be inflated by $9000 in the financial statements. The Gross Profit would not change but the reporting of income would accordingly overstated by such amount. (Piuzzi, Song, Bigach, Khlopas, Mont, Vega, 2019)

Part B

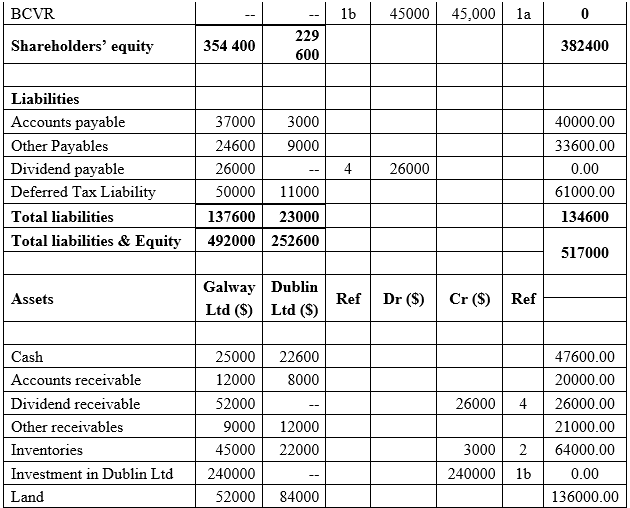

From the above adjustments the consolidation report has been created in which net affect has been considered thereby eliminating all the previous stated entries that enables us to understand the true and fair view of the financial statements of the company. As per the international accounting standard all the intra group entries should be adjusted effectively to deliver correct value of the statements.

References

.png)

Download Samples PDF

Related Sample

- MBM BST 713 Analysing Financial Performance Assignment

- MIS605 Systems Analysis and Design Case Study 2

- BE167 7 AU Accounting and Finance for Managers Assignment

- MITS4002 Object Oriented Software Development Assignment

- HEALT1113 Effective Communication For Health Professionals Assignment

- BIS1003 Introduction To Programming Assignment

- BIS3003 IS Capstone Industry Project A Assignment

- Qualitative Research Methods

- TBUS610 E Business Strategies Assignment

- Business Research Project Report

- Simukai Child Protection Programme Case

- LST2001 Introduction to Business and Company Law Assignment

- MGT603 Systems Thinking Report

- MITS5004 IT Security Research Report 2

- EDES105 Indigenous History and Culture Report

- MPAA604 Advanced Audit and Assurance

- ICT306 Advance Cybersecurity Report 2

- EDET461 Effective Teaching 6 Professional Engagement and Reflection Report

- Fluid Mosaic Model of Membrane Structure Assignment

- LB5236 International Political Economy Report

Assignment Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

.png)

~5.png)

.png)

~1.png)

.png)