Order Now

- Home

- About Us

-

Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

-

Assignment Writing

-

Resources

- Referencing Guidelines

-

Universities

-

Australia

- Asia Pacific International College Assignment Help

- Macquarie University Assignment Help

- Rhodes College Assignment Help

- APIC University Assignment Help

- Torrens University Assignment Help

- Kaplan University Assignment Help

- Holmes University Assignment Help

- Griffith University Assignment Help

- VIT University Assignment Help

- CQ University Assignment Help

-

Australia

- Experts

- Free Sample

- Testimonial

HI6028 Taxation Theory, Practice and Law Assignment Sample

Question 1

A. John recently purchased a Theatre Hall which was in poor condition. Before starting the hall, it needed to repair a portion of the ceiling, but he decided to replace the whole of the ceiling with different but better materials. The new ceiling, in addition to enhancing the appearance of the hall, improved the acoustics. The total cost of the material and of erecting the new ceiling was $210,000. It was estimated that the cost ofrepairing the ceiling would have been $150,000.

With reference to Income Tax Assessment Act 1997 and relevant case law, discuss the amount, if any, allowable as a deduction for income tax purposes. Kindly use the following instructions:

1. Facts of the scenario

2. Relevant laws and cases

3. Application of laws and cases

4. Conclusion

B. Sanjeev is employed as a marketing manager of the Theatre Hall. He requires to travel extensively during the year for work-related purposes using his car. Discuss the ways Sanjeev might be able to claim deductions for his car expenses. HI6028 Taxation Theory, Practice and Law Individual Assignment T1.2022

QUESTION 2

After completion of your course, you start working at an accounting and tax office. Julia is your first client. She requires to lodge his income tax for 2021/22. She gave her annual income and deduction below. Calculate her Total Assessable Income, Taxable Income, Tax Liability, Medicare Levy and Medicare Levy Surcharge, if applicable, for the taxpayer (Julia) with the information below:

• Julia is a resident single mom with two dependent children (7 and 4 years old) taxpayer of Australia for the tax year 2021-2022

• Her Taxable Salary earned is $109,000 (Including tax withheld), having no private health insurance.

• She had a $11,000 deduction.

• Julia has a student loan outstanding for his previous studies at Sydney University of $35,000.

• Julia’s employer pays superannuation guarantee charge of 10% on top of her salary to her nominated fund.

• Julia earned a passive income of $7,000 from the investments in shares in the same tax year.

Solution

Question: 1

a. Deduction for repairs and maintenance:

Facts of the scenario:

In this case, John has recently purchased a theatre hall which was in poor condition and wanted to repair that portion of the ceiling which would have cost $150,000. But, instead of carrying out the repairs on that portion of the ceiling, John has decided to replace the entire ceiling with different and better materials. This new ceiling will also enhance the acoustics of the building and the total cost will be $150,000. Hence, the issue here is John wants to know whether he will be able to claim a deduction for the replacement of the ceiling that he is doing under the income tax assessment act 1997.

Relevant laws and cases:

The income tax assessment act 1937 deals with the scenarios for assignment help under which deduction will be allowed to the taxpayer under section 25-10 or section 8(1) i.e. the general deduction or the specific deductions. From the facts of the case, it is the case of allowing deduction under repairs and maintenance head and to increase the understanding income tax assessment act 1997 has come up with a 97/23 ruling where previous laws have been referred to and an understanding has been created by the regulations.

As per the clarification, repairs mean making good the defects, or damages to the property or building. The object is returned to its original form in case of repairs and does not lose its originality. Hence, in this case, the only deduction will be allowed under sections 25-10 but if major changes are made to the building or property and the property loses its form, then the deduction under this section will not be allowed. It means that only revenue expenditures are allowed as a deduction, and if any capital expenditure is done to the property, it will not be allowed as a deduction and it will be added to the cost of building, on which the taxpayer can charge depreciation(Barkoczy, 2021 p9(6)).

Hence, the word repairs do not include the word replacement or reconstruction and if replacement is done in its entirety then the same will be treated as a capital expenditure which is not deductible. The same was decided in W Thomas & Co Pty Ltd v FC of T (1965) that the taxpayer will not be allowed to claim a deduction of the expenditure that was incurred on extensive renovations. The High court also stated that expenditure done on the building will not be claimed if, without the certain renovation, the building will not be able to continue as an income-generating unit.

So, it is very important to differentiate between the word repairs, replacement, renovations, and whether a particular expenditure is in the nature of capital or revenue. For instance, if a repair is termed as an improvement, it will not be counted as repair. Also, if the repair changes the character of the building and improves the efficiency of its economic nature, then the same will not be treated as repairs and will not be considered in the revenue nature. It is also said, if the nature of the material used is improved, the changes will be counted as improvement and it will not be considered repairs (Christians, et al., 2018 p5(6)).

Applications of laws and cases:

The ruling and the case law discussed above are applicable in this case as well. John was thinking to repair the part of the ceiling which was damaged, but later he decided to replace the whole part too with better and improved material, which will also improve the acoustics of the place, and as it is a cinema hall it will attract more customers. The ruling has stated that if a farmer is thinking to replace the damaged portion of the fence, it will be considered a revenue expenditure which is allowed as a deduction and the farmer will get the benefit of the deduction. But if the entire fencing is replaced it will be considered a capital expenditure which is not allowed as a deduction. Hence, here, the replacement of the ceiling will not be included in the definition of repairs (Ingram, 2021 p9(1)).

Conclusion:

From the above discussion, it can be concluded that John will not be allowed to take a deduction of the repairs that he had done on the ceiling because first it will be considered as a replacement, and it was not done to make good the damage, but, the entire ceiling was repaired, which will be considered as an improvement, and improvements are not allowed as revenue deduction and will be charged to depreciation. Also, this change has increased the cost of repairs and will increase the efficiency which will increase the economic flow. Hence, this expenditure will not be allowed as a deduction to John as per the Income-tax assessment act 1997, and it will instead be added to the cost of building.

b. Deduction for Work-related car expenses:

Section 8.1 of the income tax assessment act 1997 states that there are certain circumstances where deduction will be allowed for work-related expenses to the taxpayer as a general deduction. The expense will be allowed to be deducted from assessable income when it is incurred to earn the assessable income or to continue with the business or profession it is crucial to incur the expense. But, the expense will not be allowed as a deduction if it is in the nature of capital expenditure or it is incurred to earn exempt income or a particular provision in the act restricts the person from claiming the deduction.

In this case, it states that Sanjeev is employed with the company and his work ask him to travel extensively for work-related purpose using his car. Here, Sanjeev wants to know whether he will be able to claim the deduction on car expenses which he has incurred for work purposes. Hence, after reading the law, it can be said that work-related expenses incurred by the taxpayer are allowed as expenses because they are incurred to earn the assessable income, and they are necessary to earn the income. In this case, the car has been used by Sanjeev for work purposes, and hence, he will be allowed to claim a deduction on the same, but, it is important to notice this expense is not in the form of reimbursement and the employee has paid for these expenses (Allen, 2020 p5(9)).

Also, if the car has been used by the taxpayer for both private purposes and for work-related purposes, then the deduction will be allowed only for work-related expenses and the taxpayer will not be allowed to take a deduction for private use. Also, if the expense is in the nature of capital then the same will not be allowed as a deduction. Travel related expenses will be considered work-related expenses till the time, they are used for business purposes or to earn income. If the work of Sanjeev is travel based, he will be allowed to claim the deduction because he is using his car for travelling for work purposes and not for this personal expense. However, in some cases the travel expense incurred on the way from home to work and vice-versa are not allowed because travelling from home to work is extremely essential and domestic (Legwaila, 2018 p5(2)).

Question: 2:

Calculation of assessable income and tax:

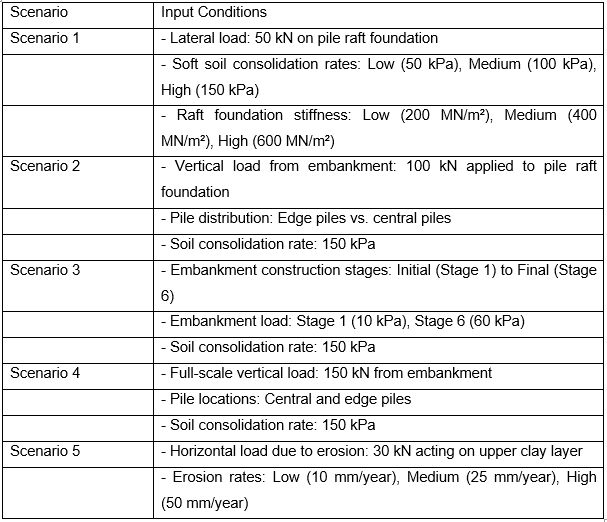

From the above, it can be said that the net tax liability that the taxpayer will be liable for discharge is $33,517. The taxpayer is an individual who has two dependents. The assessable income of the taxpayer will include the income from salary and the passive income earned by the taxpayer. The income tax is charged on the basis of rates that have been prescribed by the taxpayer and the same are as follows:

.png)

Here, the tax will be calculated as follows. For first 45,000 the tax will be 5,092 and for the remaining amount the tax will be (105000-45001) * 32.5% = 19,500. The Medicare levy will be charged as 2% of the taxable income i.e. the income calculated after reducing deductions from the assessable income.

Reference:

.png)

Download Samples PDF

Related Sample

- Internet Use and Economic Development Evidence and Policy Implications Assignment

- Project Audit and Quality Assessment Models Assignment

- TECH5300 Bitcoin Case Study 2

- MGN428 Developing Entrepreneurial Mindsets Assignment

- PUBH6013 Qualitative Research Methods Report

- LML6003 Migration Law Assignment

- PUBH6003 Health Systems and Economics Case Study

- LB5242 Value Creation Leadership Report

- HI6025 Accounting Theory and Current Issues Assignment

- MPAA604 Advanced Audit and Assurance

- ACCT20080 Governance and Ethics Assignment

- Principles of Project Management

- CSM80017 Managing Quality and Safety in Construction Site Operations Report 2

- HI6027 Business and Corporate Law Case Study

- PROJ6002 Project Planning and Budgeting Report

- BMP4004 Contemporary Issues in Marketing Assignment

- Dynamic Leadership Assignment

- MGT302A Strategic Management Assignment

- MKTG7512 Strategic Marketing Management Case Study

- INT102 Interpersonal Communication Skills Assignment 3

Assignment Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

.png)

~5.png)

.png)

~1.png)

.png)