Order Now

- Home

- About Us

-

Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

-

Assignment Writing

-

Resources

- Referencing Guidelines

-

Universities

-

Australia

- Asia Pacific International College Assignment Help

- Macquarie University Assignment Help

- Rhodes College Assignment Help

- APIC University Assignment Help

- Torrens University Assignment Help

- Kaplan University Assignment Help

- Holmes University Assignment Help

- Griffith University Assignment Help

- VIT University Assignment Help

- CQ University Assignment Help

-

Australia

- Experts

- Free Sample

- Testimonial

Finance Broking in Practice Assignment Sample

Question 1

Are your clients eligible for the First Home Owner’s Grant or stamp duty exemptions given they plan to buy in the same suburb as you? So Sweet organizational requirements requires you in addressing such questions to access the most recent figures from the website, including the link and the most recent data in your response.

Question 2

What documents would you request from your clients given their application for a mortgage loan? In what way do these documents meet organizational requirements?

Question 3

When serving this young couple, how would you fulfil your responsibilities as a mortgage broker under the anti-money laundering legislation?

Question 4

Given the fact that your clients have poor to adequate English language skills, what would you do to avoid committing unconscionable, misleading or deceptive conduct?

Question 5

Using the internet to find the most current products, decide which sort of a loan you would recommend to your clients and explain why.

Question 6

Would you recommend a portability feature within the loan for your clients?

Question 7

Calculate the loan-to-value ratio and discuss whether a lender would be prepared to lend your clients their desired amount on the basis of the information they have provided.

Question 8

What would be the monthly payments of an interest only loan be if the interest rate was 7% per annum?

Question 9

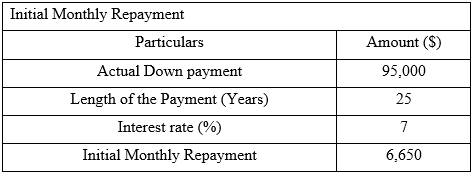

What would be the initial monthly repayments if you recommended a variable loan (principle and interest) if the interest rate was 7% and the loan term was 25 years?

Please review the illustrated example in chapter 5 for this calculation.

Question 10

How would you charge your clients? Please detail your remuneration arrangement in full in an email to your clients ensuring to sign off with your name.

Solution

Question 1

In general, the first home owner or buyer grant refers to a specific type of grant that is mainly for those who are buying their first home and just like other grants the first-time house owner or buyer does not hold a commitment to repay the grant. As being the financial broker in Australia, my clients named Peng and Mia both are definitely eligible for buying their first home in Australia. According to the reports for assignment help of Drukker (2021), to be eligible for the first home buyer grant any customer must need to buy a house or unit of townhouse which is under the value of $750,000. As in this case my clients want to buy a condominium or unit in a townhouse that values $ 410,000. The first home buyer grant is also applicable when the consumer earns income that is below $160,000 and as per their statement the couple has saved $ 95,000.

In order to take advantage of the grant Mia and Peng also lived in the nation over two years and in these years, they have been saved a fund of almost $ 1,00,000 and the rest of the money wants to acquire by a home loan. The first home buyer’s loans also include great benefits rather than other nominal bank loans.

Question 2

As per the rules of the Australian home loan system the documents are similar just as for the other loan grants. The documents needed to be carried in by my clients in order to meet the organizational requirements are birth certificate, certificate of citizenship, Medicare card, centre link pension card, utilities bill less than three months, notice of rates lesser than the three month and tax assessment notice less than 12 months. As per the statement of Nicholson et al. (2019), the documentation process of mortgage loans in Australia are divided mainly into four parts; proof of identification, ownership details or the documents related to property, documents related to customers income and expenses. The documents under the proof of identity are such as passport, birth certificate and driver license. Ownership details of properties, cars, and savings are coming under the documentation of properties and the income and expenses documentation process includes documents such as PAYG statement, recent payslips and monthly expenses from childcare to any other maintenance.

The related documents including the information of income and expenses are verified by the mortgage lenders through direct request from the consumers as these documents resolve the main four factors that are required for the verification such as gross annual income, assets and liabilities, credit history and down payment. For my clients I have been asked for the same including income for the last two years.

Question 3

The Anti Money Laundering and Counter- Terrorism Financing Act 2006 (Cth) refers to the primary piece of legastisation in order to respect the prevention and detection of terrorism financing and money laundering, (Singh and Best, 2019). As being a mortgage broker the primary and basic responsibility would be to serve my recent clients the best fitted terms based on borrower’s financial situation. As my clients are both young and currently planning to take residence inside an Australian township’s unit, my focus is to gather the right data and make a proper documentation system. The basic difference between a lender and mortgage broker, we are more responsible to give accurate advice towards the customers or clients so from that suggestion clients can make further and prominent decisions for buying a home. One of the important and other responsibilities of being a mortgage loaner is to also to provide the best options among other average options.

Underlying the act of Anti Money Laundering the active and superior responsibilities would be to assess and identify the money laundering risk, fraud and other potential suspicious activity for both client and mortgage broker, (Bailes, 2017). Monitoring and re-confirmation from the data provided by my clients and provided by me towards the clients is very much important in order to prevent any type of mortgage risk, fraud or scams.

Question 4

Under the Australian Consumer Law, it is described that any business or any type of business must not be conducted with unconscionable engagement. According to the report of Syuib (2020), it is stated that understanding and determining or identifying the unconscionable conduct is much important to reduce the risk from any misconduct. In this situation both my clients are from Taiwan and as they are poor in English in this situation it will be better to provide written documentation rather than verbal conversation. In this case, there is also a need of understanding the systems and laws regarding the mortgage loan in Taiwan, so this will benefit me in order to understand their understanding based on the laws. Also, in order to avoid being a victim of unconscionable conduct I will be using such legal process or procedures such as ensuring all agreements are in a written form, double ensuring for fully understanding all terms of transactions, explaining the terms and conditions by using easy language, seeks for the best deal and negotiate in order to achieve the best outcomes for me as well as for my clients.

For the agreement process that will be done by using plain and easy English, making sure the contract is not lengthy and not included harsh words or unfair terms.

Question 5

Based on the client recommendation after researching other relevant current products on the internet for my current clients the FHA or Federal Housing Administration Role would be the bests options among the other loan offers or products. It is highly beneficial for those borrowers who have low to moderate income and also the loan system demands for lower minimum down payment and lower credit scores rather than other conventional loans, (Troy, 2017). The loan includes so many advantages and it is very popular among first time home buyers. FHA loans are commonly issued by FHA approved banks and FHA institutions in order to properly evaluate the qualifications for the loan grant. The loan is also required to purchase mortgage insurance and premium payments are made to FHA. According to the Spitzer and Lambie-Hanson (2020), Compared to other home loans the FHA home loans include the lowest down payments of just 3.5 %.

In this loan procedure or system my client would need to get a qualifiable credit score of 580 but if they still don’t get success, they still can apply for FHA loans by making a down payment of 3.5% only if they scored between 500 to 579.

Question 6

The FHA loans already include many profitable features for the first-time house buyer but in this case, there are no other profitability features available for my clients. Portability or home loan portability refers to a feature that allows consumers to keep the same home loan product but change the supporting security of a property. The feature is also able to save the time and costs of refinancing. The home loan portability feature usually recommended to our clients when moving houses while client owe less than 80% on their mortgage. Loan portability also provides support to the clients to keep their existing loan such as current balance, interest rate and several other attached features and also change the security attached to a particular loan. In Australia, the first-time buyer only gets a discount of $10,000 when the clients are buying a new house worth $ 600,000 or building a new home valued up to $ 750, 00, (Bian et al. 2018). As per the section 245(a) loan, this program mainly for those borrowers who are expecting their income will be increased as or by these recent clients they are also expecting that in future they will earn an extra profit from their bakery business. In addition, there are small perks of profit included in the FHA loan process such as if my clients started to earn a good profit from their bakery business then can easily apply for the FHA’s limited 203(k) programs. Apart from FHA loan, there are several home or building loans in Australia that provides different interest amount and also emerge new and different type of portability. Variable interest rate loan is also known as basic and standard home loan for new residents in Australia. In this loan program, the rate of interest needed to pay by my clients would be set by the Reserve Bank of Australia and essentially the rate will either move high or low according to Australia’s Reserve Bank.

These programs help the clients to wrap up the $35,000 for additional renovation expenses into their mortgage loan and the service also includes other serviceable programs such as house repair, house improvement or any up gradation needed in house. As per the report of Whait et al. (2019), this particular loan system can also be applied by a single woman, just for example if Mia wants to buy a further property in future by all alone, she can easily apply for this loan and there is no extra documentation or verification needed.

Question 7

.png)

Based on the financial data or information provided by my customers, a lender would definitely provide many options regarding house buying. The couple are both intermediate in English so it is determined that if the lenders can communicate through by speaking English that will be beneficial for both in order to understand each other’s wants and needs. Based on the other information my both clients have stated that they want a big size house as per the view of their future perspectives but as they both do not have a proper stable income beside the profit, they earn from their bakery business it may be quite discomforting for the lenders. The couple has both stayed in Australia moreover two years and the resident they are looking for they want to spend over six months, as based on this relative information the lender can gain a trust ability in against the couple. Like mortgage brokers, lenders also want to see the proper documentation of the buyers in order to avoid any fraud or scam so by enabling the process of proper documentation the lender can actively sell their property without any further hesitation.

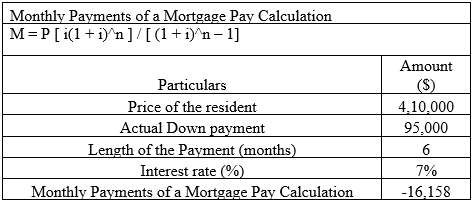

Question 8

Based on the financial information provided by my client, only if the interest changes into 7% Annum the Mortgage payment would be $ (16,158) monthly.

Question 9

Based on the financial data and by following the calculation method from chapter five the calculation process is mentioned above. As in this calculation we have presumed that the actual payment or the value of P is $95,000 and the interest rate is 7% and the length of the payment is 25 years. The calculation of initial monthly repayment is the interest rate divided by the length of the payment and multiplied by the down payment and through this the calculation of initial monthly repayment is evaluated, (Ampofo, 2020). Based on the future situation for my client, if they increase the rate of the payment, they can sustain a long-term process and as well as it will be very beneficial for them. The situation of increasing the interest would be only done if the clients increase their future earnings or the profit from their bakery shop.

Question 10

For this new client Mia and Cheng by the determination it is acknowledged that the FHA loan would be the best and most appropriate loan system for them. As per the report of Young et al. (2021), it is found that the FHA loan is known as one of the most popular house loans for first house buyers. Just as many other mortgage brokers based on the total loan amount from 1 to 3% will be charged from the client. The remuneration would be done by both in written or paper documentation and as well as a soft copy will be sent to the email address provided by my client. The process would also be done through writing in easy English and the verbal communication will be done through based on both sides' understanding. The documents regarding the remuneration will be defined through specific contents and not using too lengthy words as my clients are not experts in english. In the both documentation there will mention the 0.5 percent commission charged from the total price of the house, based on the data the fees will be applicable for these clients. 0.5 % of $ 410000 means $2,050.

Reference List

.png)

Download Samples PDF

Related Sample

- DATA4300 Data Security and Ethics Assignment

- SPO101 Introduction To Sports Management Assignment

- MRKT20057 Global Marketing Assignment

- EDUC9607 Preparation for Coursework Project Assignment

- ECE220 Science and Environmental Awareness for Young Children Assignment

- FIN921 Impact of CSR on Corporate Performance Assignment

- CSIT985 Social Media for Organization Innovation Essay 2

- LML6001 Practitioner Legal Skills for Australian Migration Law Case Study

- Data Modelling and Database Design Assignment

- Coursework on Demand and Supply of Certain Resources Assignment

- BUGEN5930 Business Society and The Planet Assignment

- MBA5006 Managing Organisational Behaviour Assignment

- MBA642 Project Initiation Planning and Execution Assignment

- TCHR5003 Principles and Practices in Early Childhood Assignment

- MGMT20132 Innovation and Sustainable Business Development Assignment Sample

- MGT501 Business Environment Assignment

- BMG704 International Finance

- Globalizations Effect on Central Asian Countries Socioeconomic and Political Development

- U24035 Customer Relationship Management Assignment

- MGT601 Dynamic Leadership Assignment 1 Part B

Assignment Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

.png)

~5.png)

.png)

~1.png)

.png)