BST903 Financial and Business Analytics Assignment Sample

INDIVIDUAL ASSIGNMENT

KEY DETAILS:

The individual assessed assignment counts for 50% of your final module mark.

The submission date for the assignment is: 11 February 2022 by 11.00a.m.

GUIDELINES

You are required to answer all parts of the assignment. The word limit for the assignment is 2,000 words, excluding appendices, tables and a reference list for assignment help Calculations may be included as part of the appendices (they will not form part of the word count). Please note that failure to comply with the word limit may result in a restriction of marks.

You will be awarded marks for the assignment for a number of different criteria, including evidence of conceptual understanding of the material being tested, clear and accurate analysis of the data, and analytical and critical thought. You will also be awarded marks for originality and evidence of additional reading. Finally, a proportion of marks will also be allocated for the structure, style and logical development of the report, and grammar and appropriate referencing (you should reference appropriately all your work and cite the complete list of references used at the end of the report).

Kindly double/1.5 space your report and submit it via Learning Central.

All administrative issues should be directed to the Postgraduate Hub: carbs-PGQueries@cardiff.ac.uk

1. Introduction

The board of directors met for their regular quarterly meeting on 6 January at which the CEO, Charles Chatters, presented details about a new project. The board also, as part of its agenda, considered the funding preferences for this project and potential future ones.

The meeting of 6 January was the first meeting that Fred Franks (FF) the new finance director attended. Discussions at the meeting got somewhat heated when FF suggested that the company use the net present value model of investment appraisal to appraise capital projects. CC immediately became defensive and resisted this advice - arguing that the company had traditionally used the accounting rate of return model and ‘there was no need to change methods of appraisal’.

CC and FF were also disagreed on methods of financing for future investment projects. While FF deemed it prudent to use the retained surplus cash within the company before seeking external funding, CC was keen to seek out new debt, as the cheaper form of finance. The company currently has surplus funds of £120 million.

Following the diverse views of the board, a decision was taken to seek advice from an external consultant.

2. Investment Project

In recent years, CC has been keen to move into the niche market of healthy snacks. Following a sizeable investment into the research and development of such products (the costs of which have been written off in the annual accounts), the company has developed a new healthy snack for toddlers, Wigglers. CC now hopes that Wigglers is a commercially viable product. His team has generated the following data.

i. The company would manufacture the product out of its Bournemouth site that is currently unused, if deemed worthwhile. It would require capital investment in plant and equipment of £100 million, half of which is payable immediately and the other half in twelve months’ time. The plant and equipment will have a useful life of five years, at the end of which it will be sold for £25 million.

ii. Annual sales volume of Wigglers is expected to be 10 million wholesale boxes for the first two years. Thereafter it will fall by 20% as competition rises; this fall will be a one-off in year three and stagnate at this level thereafter. The sales price per wholesale box has been proposed to be £22.00 for the duration of the project.

iii. Variable costs per wholesale box have been estimated as follows:

Variable materials 8.00

Variable labour 1.80

Variable overhead 1.20

In addition, fixed costs inclusive of depreciation of plant and equipment have been calculated at £84 million per annum.

iv. Depreciation is computed on a straight-line basis by the firm. All assets are depreciable.

v. The company requires a working capital investment of 10% of the annual sales value. 95% of the working capital investment is expected to be recovered. Working capital investment levels (and in turn working capital recovered) reflect any change in demand patterns.

The company pays taxes at a rate of 20% and makes ample profits onto which to pay this tax. Finally, Magenta plc has a required rate of return of 15%.

3. Company Background

Magenta plc’s humble beginnings started with a staff base of 18 employees in 1988 and a turnover of just £240,000. Currently listed on the Alternative Investment Market (in 2000), the company is valued at £4 billion and has 3,500 employees across 15 locations in the UK. Originally specialising in potato crisps, today the company manufactures a range of different snacks, catering for different client preferences. The company’s financial performance has generally shown an upward trend and in recent years this is in part a reflection of its rapid expansion programme under the leadership of the current CEO. CC joined the company 8 years ago and has led considerable expansion of the business and has two more years to run before he retires. One observation in light of the expansion plans is that Magenta plc is more heavily geared than its competitors – 10% more than the industry average (ruling out any outliers).

REQUIRED:

PART A (20 Marks, split equally between Ai and Aii)

Assuming that the objective of the firm is to maximise the wealth of its shareholders:

i. Appraise the investment project using the two models supported by senior managers and determine whether Magenta plc should proceed with the manufacture of Wigglers, giving a justification for your choice of model. You may use a spread sheet for your computations;

ii. Drawing on literature you are familiar with, evaluate the views put forward by the senior managers in relation to the financing choices should the current project (or indeed other projects) be selected, proposing a solution based on your assessment of the company’s position.

(Indicative word count: 400 words for Ai and ii combined)

PART B (40 Marks)

CC firmly believes that budgets should be set by the board and then imposed on those in functional/operational positions, whereas FF thinks that the company's budgeting system is far more likely to attain its objectives if employees and junior management are given a say in how their budgets are set.

Give a critical review of the two apparently conflicting opinions, considering claimed advantages and disadvantaged from both practical and theoretical perspectives.

(Indicative word count: 800 words)

PART C (40 Marks)

Based on data relating to the six major firms in the snack industry as presented in the tabs of the accompanying Excel spread sheet:

i) Calculate the industry weighted average of a) the return on capital employed (%) and b) the gearing ratio (%). You should fully discuss your weighted averages, and clearly explain any key underlying assumptions in making these calculations.

ii) Calculate the standard deviation for the two variables in C(i) above. You should fully discuss your results for the standard deviation, along with any assumptions you have made in undertaking these calculations.

You may choose whichever approach you consider the most appropriate for calculating the weighted averages but you must specify and justify that approach.

(Indicative word count: 800 words)

Solution

Part A

Appraise the investment project using two models.

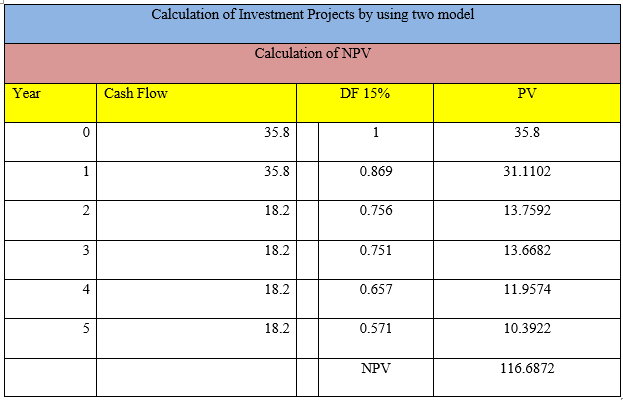

Table 1: Net Present Value

(Source: Created by Author)

Model NPV is considered as the time value of money. These are specified as the financial metrics that have to seek capture with the total value with potential value opportunity. Here, the value of NPV is 116.6872. Discounting factor is 15%. The positive value of NPV indicates the projected earnings that exceed the anticipated costs.

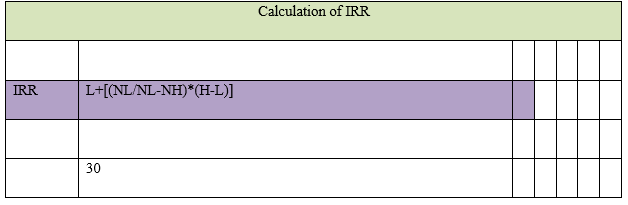

Table 2: Internal Rate of Return

(Source: Created by Author)

There is the calculation of IRR = L+[(NL/NL-NH)*(H-L)] (Wild 2019). Value comes in IRR is 30.

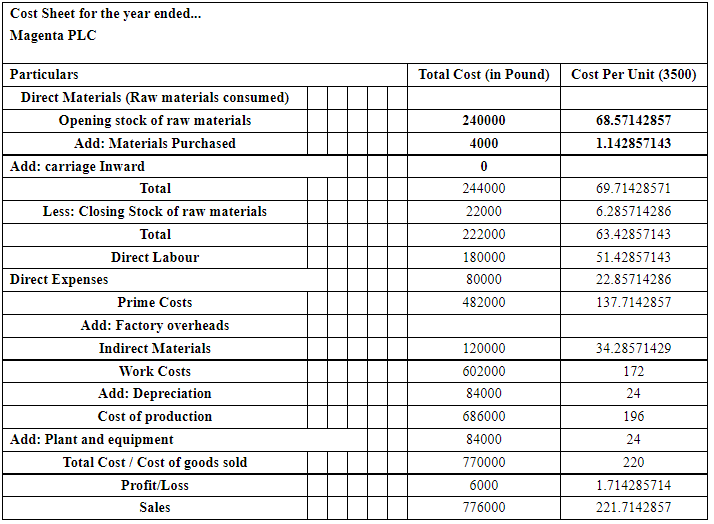

Table 3 Cost Sheet

(Source: Created by Author)

There is the following calculation of the cost sheet of Magenta PLC. The value of sales is GBP 694200. Here, the valuation of Magenta PLC is GBP 4 billion. Calculation of cost sheet is important for analysing production and factory costs (Appelbaum et al. 2017).Value of plant and equipment is GBP 84million.Magenta PLC is making working capital investments of 95%. Opening stock os raw materials are GBP 240000 million is based on 18 employees. Accurate costing information verifies the capacity to build and maintain a proper business in an organisation (Morningstar.com 2022). Here, the total cost/ cost of goods sold is GBP 688200.

Evaluate the views with senior managers about financing choice of current projects.

In this organisation, financial managers are responsible for the financial health of the organisation. Guiding as per supervisors in an individual’s departments is the following responsibilities roles of the senior managers. Investing and financial planning have to be analysed organisation weaknesses and strengths. Managers of organisations help to improve the profitability of an organisation. The above financial analysis is familiar with the business because of the positive value of Net present value. The positive value of net present value iis accepted for investment analysis. This current project must be select for the organisations current position. Most simple way of net present value determines about the market capitalisation of an organisation. Managers should be accepted positive value of NPV because of the free additional cash flows. Magenta PLC is required working capital investments 10%. Positive amount of IRR is also acceptable of a business organisation. Calculation of Net present value is done with the help of discounting factor 15%.This mainly, indicates about the angel investments, which is considered as the good for the organisation.

Senior manager assisting departments by creating and managing forecast and budgets for gathering information of an organisation. Financial manager helps to build capital structure of the organisation (Sun et al. 2017). This business used as a combination of financing sources and raising funds. Proper financial decision helps to perform in the financial statement analysis of the organisation.

Part B

Advantages and disadvantages of budgets in both theoretical and practical perspectives

Top down is more tedious in nature and have a vital advantages in growth of financial. Proper budgeting should be used in managing the money efficiently. Top down approach has an advantage for stating based on goal and budget allocation in an organisation. Specific flexible budgets are created by using formula and certain price of the organisation. Budgeting helps to know about the specific information of financial position in the organisation and in this organisation, flexible budgets and saves time with more realistically emphasising executive resource planning and decision in an organisation.

Figure b.1: Graph of budget in CC firm

(Source: Kim et al. 2020).

Certain financial criticisms of budgets have to reduce flexibility and entities of an organisation. Proper budgeting systems arises motivation of an organisation. Bottom down approaches in budgets is creating a financial budgeting in an organisation. Proper department of the organisation is creating is creating cost projection and list in expenses. Budget of employees in bottom down approaches of budgets can approved capital expenditure in a specific period.

A disadvantage in top down approaches may lead over and under employment with new plan of budget allocation. Top down approaches of may result in unrealistic calculation economic situation and organisational activities. Budgeting mainly allows to the financial managers to explore revenue and price within the sets of the operating assumptions. This represents a certain qualifications within management features. The Top down approach has eliminated bulks and fragment and accumulated High employment coverage and with having top visibility are the advantages of implementation in practical approaches. Specific standardize with services and products is having a business impacts of the theoretical approaches in management. Whereas the Bottom ups approach has initially identified the Proper budgets are having conflicting roles to evaluate co coordinating activities in an organisation. Output of the budgets should be matched with projected sales. In preparing the budgets properly, managers of all the levels of management have to take systematic rules of the organisation (Aydiner et al. 2019). Operational budgets systems are having vital roles that built difficult to meet them. It is often to evaluating individual managers from their budgets standards effects in price or certain circumstances in this development expenses.

There is the potential conflict of top down approaches between motivation and evaluation roles of budgets. Top down approaches involves with senior management team that can improve high level of budgets in organisation. During the end of the budgets periods, certain modification and adjustments have to be made for changing this environmental condition in this organisation. Budgets are having specific consequences that have to achieve financial and academic goal of these organisation. Bottom down budgeting helps in indicating faster budgeting procedure and better financial controlling of the organisation. Effective budget mainly, forecast expenses and incomes of this organisation. Significance of the budgets helps to make investment contribution. Inaccurate forecasting and having potential with underperformance can be deducted in performance of demand planners in the organisation (Vidgen et al. 2017). Budgets are the following estimation of expenses and revenue in a specific future period.

Budgeting is also having unrealistic outcomes in this organisation. Following budgets is also set with assumptions that generally are not so distant in operating conditions. Top down approaches; budget can save both resources and time of the organisation. Due to these approaches, managers of the organisation can saves time in organisation and can use to formulate of implementation in budget Proper cost structure and organisation’s revenue can be change actual results from this expectations plotted of the budgets. In this organisation, there is rigid decision making in the practical perspective of budgets functions. Here, budgeting procedure mainly, focuses in the attention of management strategy and team during this budget formulation. Top down approaches of budgeting have to decreases the motivation of lower level manager. For this top down approaches, there is creating a conflict between organisation executive and lower level manager. Proper budget creation in practical perspectives is a very time consuming. Work required in the budget is more extensive, if the conditions of the business constantly change in the repeated iterations of budgets periods. Time is consuming low, if there is better design in the creation of budgets. In this organisation, an experienced financial manager can be attempt in introducing budgetary slack, this mainly, involves deducting in estimating revenues and also improving this estimated expenses.

Lack of Practical perspectives in budgets is having expenses allocation that prescribed a specific amount of certain price. Managers of expenses allocation departments of this organisation are not allowed to provide alternatives due to the lower price services. Thus, proper budgets is making tends for the managers entitled certain amount of funds in a year. If this department is allowed with specific amount of expenditure, then it cannot appear in the quantitative aspects of the business (Appelbaum et al. 2018). Following nature of budgets is so numeric and it considers as a financial outcomes of this business. This usually means that the budgets intend to focus in maintaining or improving aspects of profitability. If, this department does not have any of the budgeted outcomes, then this department managers can be blame any of the other departments and provides certain services.

Top down approaches is creating easier to manage in implementation and drafting with goal of organisation. Ideas or projects in bottom down approaches are deciding proper values of organisation’s budgeting, that provides a great expectation in organisation. Budgets lead to the inflexibility in the decision making of an organisation. Budgeting has to be considered as the time consuming process in any of the large business. Procedure of budgets, is mainly consider financial outcomes. Proper nature of budgets tends to focus with management attention in these quantitative aspects of organisation.

Part C

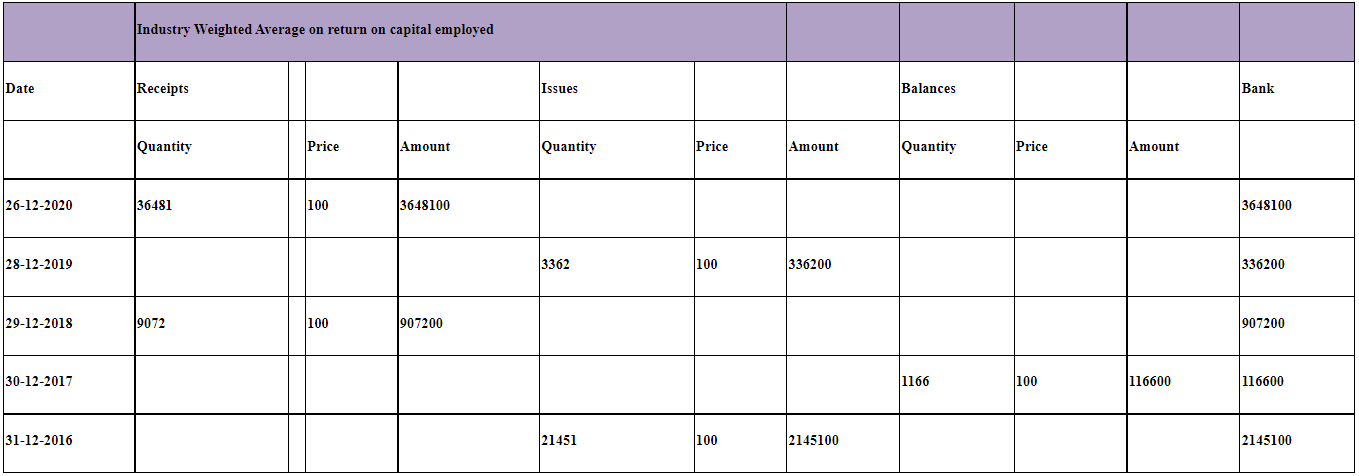

Calculate the industry weighted Average

ia) Return on capital employed

Table 5: WACC

(Source: Created by Author)

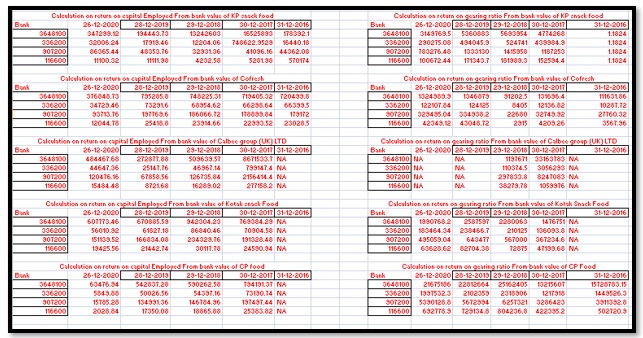

Table 6: Calculation on Return on capital employed and Gearing Ratio

(Source: Wang and Byrd 2017)

The Calculation of WACC is done by net tangible assets and Here, in 26-12-2020 36481*100 = 3648100, in issues of 28-12-2019 is 3362*100 = 336200, in receipts amount of 29-12-2018 is 9072*100 = 907200, in balance amount of 30-12-2017 is 1166*100 = 116600, in 31-12-2016 is 21451*100= 2145100. There is the following calculation of weighted average method of capital employed. Here, is the calculation of receipts, issues and balances of the bank. Further calculation of Specific amount of 26-12-2020 is GBP 3648100, in 28-12-2019 is GBP 336200, in 29-12-2018 is GBP 907200, in 30-12 2017 is GBP 116600 and in 31-12-2016 is GBP 2145100. There is the calculation of WACC from the ratio return on capital employed and gearing of five companies. Five companies are KP snacks limited, co-fresh, Calbee group (UK) limited, Kotak snack food and CP food.

Return on capital employed has to be calculated with the dividing net profit and capital employed (Wang and Byrd 2017). It is useful to calculate because of comparing the performance of the organisation with the sectors of capital intensive. These analyses prove as the following business gains from the certain assets and liabilities of this organisation (Lacerenza et al. 2018). Return on capital employed represents amount of specific capital investment in front of operations.

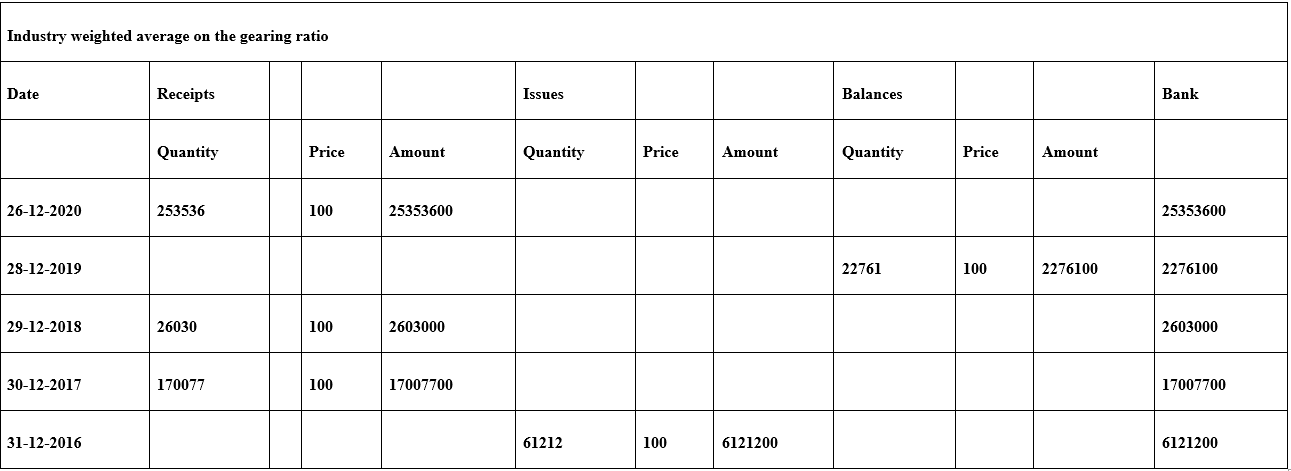

b) Gearing Ratio

Table 6: Gearing Ratio

(Source: Created by Author)

Industry weighted average return on gearing ratio have to be calculated in multiplying costs and capital of each of the following sources (Kumar et al. 2017). This causes a relevant sources of equity and debt, that can determines value of organisation. Calculation of the has been done by identifying Balance of 26-12-2020 has been calculated as GBP 25353600, in 28-12-2019 is GBP 2276100, in 29-12-2018 is GBP 2603000, in 30-12-2017 is GBP 17007700 and in 31-12-2016 is GBP 6121200.

Capital employed of the following balance sheet is the measure of reduced in valuing assets and current liabilities. Here, present liabilities of an organisation are considered as the portion of organisation’s debt. Working capital in gearing ratio maily, shows the amount of liabilities and assets of an organisation (Kokina and Davenport, 2017). Capital investments in gearing ratio represents how much of owner has invested into the business along having prospering profits. Gearing ratio mainly measure, how much operation are funded and received from shareholders as an equity. Gearing ratio in weighted average return indicates financial leverage and level with interest bearing of organisation. This analysis mainly, determines about the firms operation have to be funded with the shareholders. There is having appropriate level of the gearing ratio in organisation (Hofmann and Rutschmann 2018). 60% of this organisation shows debt level and 60% of its having equity. Gearing ratio can be manageable, for the utility in an organisation.

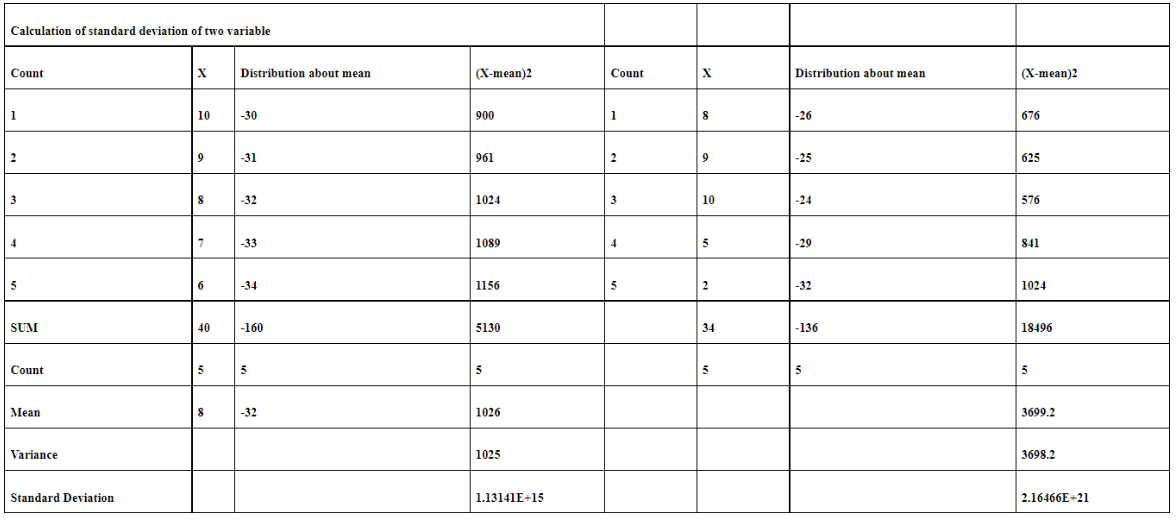

ii) Calculate the standard deviation of two variables

Table 6: WACC

(Source: Created by Author)

There is the following calculation of standard deviation of X and Y. Standard deviation of X is 1.31 and standard deviation of Y is 2.16. This analysis verifies about the spreading the values within datasets. Following calculation of variance of X have to be done by sum/Count-1. 5130/5 = 1025. Variance of X is 1025 and variance of y is 3698.2. The analysis of standard deviation is the following statistical terms that have to be measured in financial statements. Standard deviation is useful in analysing of trading strategies and also formulating proper investments decision of an organisation (Weber et al. 2019). Potential investments of an organisation are having important factors of an organisation. Return of investment helps in determining specific standard deviation of the organisation.

Analysis of standard deviation helps to calculate proper margins with error in consumer satisfaction and inventory prices. Standard deviation has to be determined by the variability in an organisation. Proper variance can help in finding distribution of information in this analysis. Standard deviation specifies the accurate mean of an organisation. Uses of standard deviation cannot assume its normality of the organisation. Formula of identifying the distribution of mean is (X-mean) and (X-mean) 2. Following calculation is based on the square root of the two variance by determining the data points related to its mean (Shaturaev, and Bekimbetova 2021). Assumption of normal distribution in standard deviation has to be obtained by random allocation and random sampling.

References

Journal

Appelbaum, D., Kogan, A., Vasarhelyi, M. and Yan, Z. 2017. Impact of business analytics and enterprise systems on managerial accounting. International Journal of Accounting Information Systems, 25, pp.29-44. Available at: DOI: http://dx.doi.org/10.1016/j.accinf.2017.03.003 R. [Accessed on: 1st February 2022]

Appelbaum, D.A., Kogan, A. and Vasarhelyi, M.A. 2018. Analytical procedures in external auditing: A comprehensive literature survey and framework for external audit analytics. Journal of Accounting Literature, 40, pp.83-101. Available at: DOI: https://doi.org/10.1016/j.acclit.2018.01.001. [Accessed on: 1st February 2022]

Aydiner, A.S., Tatoglu, E., Bayraktar, E., Zaim, S. and Delen, D. 2019. Business analytics and firm performance: The mediating role of business process performance. Journal of business research, 96, pp.228-237. Available at: DOI: https://doi.org/10.1016/j.jbusres.2018.11.028 R [Accessed on : 1st February 2021]

Hofmann, E. and Rutschmann, E. 2018. Big data analytics and demand forecasting in supply chains: a conceptual analysis. The International Journal of Logistics Management. Available at : DOI: https://doi.org/10.1108/IJLM-04-2017-0088. [Accessed on: 1st February 2021]

Kim, A., Yang, Y., Lessmann, S., Ma, T., Sung, M.C. and Johnson, J.E. 2020. Can deep learning predict risky retail investors? A case study in financial risk behavior forecasting. European Journal of Operational Research, 283(1), pp.217-234. Available at: https://core.ac.uk/download/pdf/250590642.pdf. [Accessed on: 1st February 2021]

Kokina, J. and Davenport, T.H. 2017. The emergence of artificial intelligence: How automation is changing auditing. Journal of emerging technologies in accounting, 14(1), pp.115-122. Available at: DOI: 10.1002/isaf.277 [Accessed on: 1st February 2022]

Kumar, A., Sah, B., Singh, A.R., Deng, Y., He, X., Kumar, P. and Bansal, R.C. 2017. A review of multi criteria decision making (MCDM) towards sustainable renewable energy development. Renewable and Sustainable Energy Reviews, 69, pp.596-609. Available at: DOI: http://dx.doi.org/10.1016/j.rser.2016.11.191 R [Accessed on : 1st February 2022]

Lacerenza, C.N., Marlow, S.L., Tannenbaum, S.I. and Salas, E. 2018. Team development interventions: Evidence-based approaches for improving teamwork. American Psychologist, 73(4), p.517. Available at: DOI: 0003-066X/18/$12.00 http://dx.doi.org/10.1037/amp0000295 [Accessed on: 1st February 2021]

Shaturaev, J. and Bekimbetova, G. 2021. THE DIFFERENCE BETWEEN EDUCATIONAL MANAGEMENT AND EDUCATIONAL LEADERSHIP AND THE IMPORTANCE OF EDUCATIONAL RESPONSIBILITY. InterConf. Available at: DOI: 0000-0002-0982-5741. [Accessed on : 1st February 2022]

Sun, Z., Strang, K. and Firmin, S. 2017. Business analytics-based enterprise information systems. Journal of Computer Information Systems, 57(2), pp.169-178.. Available at : DOI: 10.1080/08874417.2016.1183977 [Accessed on : 1st February 2022]

Vidgen, R., Shaw, S. and Grant, D.B. 2017. Management challenges in creating value from business analytics. European Journal of Operational Research, 261(2), pp.626-639. Available at: DOI: https://eprints.bbk.ac.uk/id/eprint/19847/ [Accessed on: 1st February 2022]

Wang, Y. and Byrd, T.A. 2017. Business analytics-enabled decision-making effectiveness through knowledge absorptive capacity in health care. Journal of Knowledge Management. Available at: DOI: link to article: https://doi.org/10.1108/JKM-08-2015-0301 [Accessed on – 1st February 2022]

Weber, M., Domeniconi, G., Chen, J., Weidele, D.K.I., Bellei, C., Robinson, T. and Leiserson, C.E. 2019. Anti-money laundering in bitcoin: Experimenting with graph convolutional networks for financial forensics. arXiv preprint arXiv:1908.02591. Available at: DOI: https://arxiv.org/pdf/1908.02591.pdf. [Accessed on: 1st February 2022]

Wild, J. 2019. Financial Accounting: Information for Decisions, 9e.DOI: Detailed List of New Features. Available at: http://ecommerce-prod.mheducation.com.s3.amazonaws.com/unitas/highered/changes/wild-financial-accounting-9e.pdf [Accessed on: 1st February 2022]

Website

Morningstar.com, 2022. Magenta 2020 PLC. Available at: https://www.dbrsmorningstar.com/issuers/24720/magenta-2020-plc. [Accessed on: 1st February, 2022]

- Information Systems Capstone Assignment

- Novel Protein Acherons Distribution Using Fluorescence Microscopy Assignment

- Effect of Life Experiences on Psychology Theory Orientation

- PRO100 Information System Project Management Assignment

- SIT741 Statistical Data Analysis Assignment

- ACCT6007 Financial Accounting Theory and Practice

- MIS500 Foundations of Information Systems Report 3

- LAW6000 Business and Corporate Law Assignment

- BEHL2009 Bachelor of Social Science Assignment

- BUS5DWR Data Wrangling and R Report 2

- MBA632 Knowledge Management Assignment

- FIN921 Impact of CSR on Corporate Performance Assignment

- MIS610 Advanced Professional Practice Report

- LAWS20058 Australian Commercial Law Assignment

- Managing Information Systems Technology Projects

- DASE201 Data Security Assignment

- Internet Use and Economic Development Evidence and Policy Implications Assignment

- CPC40120 Certificate IV in Building and Construction Assignment

- Strategic Management Assignment

- Wind Turbine Power Production Estimation for Better Financial Agreements

.png)

~5.png)

.png)

~1.png)

.png)