MCR006 Financial Management Assignment Sample

Assignment Brief

Due date - Friday Week 10 11.59 pm

Weight - 15%

Marks for assignment - 50

The Research Report should contain no more than 2,000 words, excluding references.

Submission via Turn-it-in on Moodle and strict adherence to submission and uploading rules to be followed. All parts should be answered.

All references and examples must be within an Australian context.

Scope of the research can include Academic articles and journals, and relevant Books. Students are encouraged to use the e-library resources.

Assignment Topics

Complete all questions for assignment help

Part A 400 words each 10 marks each

a. Explain how the general dividend valuation model values a share.

b. Explain, compare and contrast the various capital budgeting methods such as the Net

Present Value Method, the Payback Period, the Accounting Rate of Return and the Internal Rate of Return.

c. Discuss the two Modigliani and Miller propositions and the key assumptions underlying them and their relevance to capital structure decisions.

Part B 800 words 20 marks

Your Board of Directors is considering acquiring a business in the same industry. The Board has not undertaken such a venture before. The CEO has come to you to ask you to prepare a Board report

which clearly explains the 3 main methods of valuing a business. Include in your report the specific valuation methods the board should consider when making their decision on the company they should acquire. Assume this is a listed company and the company Being acquired is a listed company.

In the report identify and explain some other areas than valuation methods that should be considered by the directors when undertaking the acquisition of another organisation.

Solution

Abstract

This report provides the acquisition analyses of the two business corporate belong to Australia in the industry of gold mines. Saracen Mineral Holdings has acquired Kalgoorlie Consolidated Gold Mine. It also includes the various financial appraisal technique and model. Saracen Mineral Holdings company engaged in the mineral development and exploration while KCGM has also been engaged in the same business filed.

Part A

a. Dividend Valuation Model

The dividend is referred to as a part of a business's profit that is distributed by an entity to its shareholders (Sahoo 2020). Whenever a business entity earns profits, it has the option to either reinvest the earned profits in its business or payout such profits to its shareholders in the form of a dividend. Different patterns or models may be followed by the business entities for the payment of dividends. These dividend valuation methods help in determining the value of an entity's share. These patterns may include the following:

? Zero Growth Model

When the payment of dividends by any business entity is expected to remain the same in the future, then it may be said that the business entity applies a zero growth dividend model. The following formula may be used to determine the value of share when the entity is using a zero growth model for the dividend payment:

Stock’s Value = Dividend / Required (RoR) Rate of Return

The above formula is also used to determine the present value (PV) of perpetuity. Also, the formula may be used to calculate the price of the preferred stock of the entity that pays the dividend at a particular rate. The price of the stock may change in the zero-growth model when there is a change in the required rate (RoR) of a return due to the change in risk factors (d'Amico & De Blasis, (2020)).

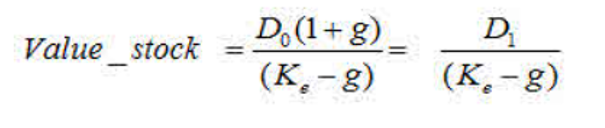

? Constant Growth Model

When the payment of dividends by any business entity is estimated to grow or increase at the same rate in the future, then it may be said that the business entity applies a constant growth dividend model. It is also known as Gordon (GGM) Growth Model. Valuation of matured companies may be performed based on this dividend model. The dividends of matured companies using this model increase on a steady basis. The formula in the below-provided image is used to determine the value of the entity's share who is applying constant growth model for dividend:

? Variable Growth Model

The variable growth model is the most commonly used dividend model in a real-life scenario. As the business entity goes through different phases, it becomes difficult for the entity to pay the same dividend every year. The growth in the variable model may be divided into 2 or 3 phases. The growth rate in the initial phase may be high, then it may get low in the transition phase and finally, it may end with a lower dividend rate. The formula in the below-provided image may be used to calculate the stock value as per the variable model:

b. Capital Budgeting

Capital Budgeting is a method used in finance to evaluate the potential of a major investment proposal or project (Siziba & Hall, (2021)). It helps the investors to ascertain the value that a potential project may provide to them. Capital Budgeting helps to make an important investment decision that may increase its profitability and ultimately the wealth of its shareholders (Cloyne & Surico, (2018)). Different methods may be used by the business entity in the process of capital budgeting that has been discussed hereunder:

? Net Present (NPV) Value

Net Present (NPV) Value helps to assess the profitability aspect of an investment proposal in the process of capital budgeting (Kadim & Husain, (2020)). The present value (PV) of all the cash inflows that are expected to be generated through the tenure of the project is subtracted from the present value (PV) of all the cash outflows to arrive at the Net Present (NPV) Value. If the difference between the cash flows is positive that the investment project may be considered viable. The discount rate is used to ascertain the expected cash flows of the future period. Assessing the profitability of a project from NPV may have several errors as it is based on various assumptions & estimates.

? Payback Period

The payback period is the period by which the investment cost in any investment project is recovered. It is the period by which the project reaches its break-even. A short payback period is considered favorable by the investors. This method has some limitations as it ignores the time value (TVM) of money. Overall profitability of an investment proposal may not be ascertained through the payback period as it will only tell the time by which cost will be recovered and it will not tell what will happen after such period.

? Internal Rate (IRR) of Return

Internal Rate (IRR) of Return is referred to as a rate of discount that will make the NPV of future cash (FCF) flows to zero. A higher IRR is always considered good by the investors. It is calculated similarly as the NPV is calculated. The only difference in the calculation is that IRR makes the NPV zero.

? Accounting Rate (ARR) of Return

Accounting Rate (ARR) of Return is referred to a rate (RoR) of return that may be expected from an investment in comparison to the cost of the initial investment. ARR is calculated by dividing the average revenue of an asset by the entity's initial investment. ARR is useful when determining the profitability of investment quickly but it ignores the time value (TVM) of money.

c. Modigliani & (MM) Miller Approach

The theory of Modigliani & (MM) Miller Approach states that the overall value of a business entity is not affected by its capital structure. In Modigliani & (MM) Miller Approach's first version there were a lot of limitations as such version was developed with the assumption that a business entity operating in the perfectly efficient industry wherein it need not pay taxes. Later on, Modigliani along with Miller developed the next version of the theory wherein they included bankruptcy costs, asymmetric data, and taxes.

MM Approach in Perfect Market

Modigliani & Miller's first version of the theory assumed that businesses always operate in the perfectly efficient market. This means that the business entities are not required to pay tax, no transaction costs are incurred on the trading of the entity's shares. Also, it had the assumption that no bankruptcy costs are incurred in case of bankruptcy.

Proposition 1 (First Version)

Value of (Vl) Levered Entity = Value of (Vu) Unlevered Entity

According to the first proposition, the value of an entity is not affected by its capital structure whether it is funded by only equity or by a combination of debt & equity as its value is determined by the present value (PV) of future (FCF) cash flows. Additionally, entities need not pay taxes in a perfect market, the entity does not get a benefit tax deduction for the interest on the debt.

Proposition 2 (First Version)

Cost of (Re) levered equity = Cost of (Ra) unlevered equity + Debt to (D/E) Equity (Ra – Cost of (Rd) Debt)

According to the 2nd Proposition of the theory, the Cost of (Ke) Equity and leverage level of entity is directly proportional. When leverage level increases, the entity's profitability of entity also increases.

MM Approach in Real Life

Proposition I

Value of (Vl) Levered Entity = Value of (Vu) Unlevered Entity + Tax Rate x Debt

According to the 1st Proposition, the value of (Vl) levered entity is higher than the unlevered entity's value because of the tax benefit shield on the interest payment.

Proposition II

Cost of (Re) levered equity = Cost of (Ra) unlevered equity + Debt to (D/E) Equity x (1 – Tax Rate) x (Ra – Cost of (Rd) Debt)

According to the 2nd proposition, the cost of (Ke) equity and leverage level of the entity is directly proportional. The effect of tax shield makes the cost of (Ke) equity& entity’s leverage level less sensitive to each other.

Part B

Board Report

Introduction

At Saracen Mineral Holdings, all of our operations are controlled and managed by the Board of Directors on shareholders' behalf. This report has an agenda for the acquisition of the business of one of the listed companies known as Kalgoorlie Consolidated Gold Mines (KCGM) which is also engaged in the business of gold mining.

Reason for Acquisition

The main reason for the acquisition is to become the source player in the gold industry and to remain in the field of basic material . As our company is competing with Saracen Mineral in the Gold industry, its acquisition will help our company in gaining competitive advantages and both the company will merge to create the AUS 16 billion global gold producer (Saracen Mineral Holdings 2019)

Capital Expenditure

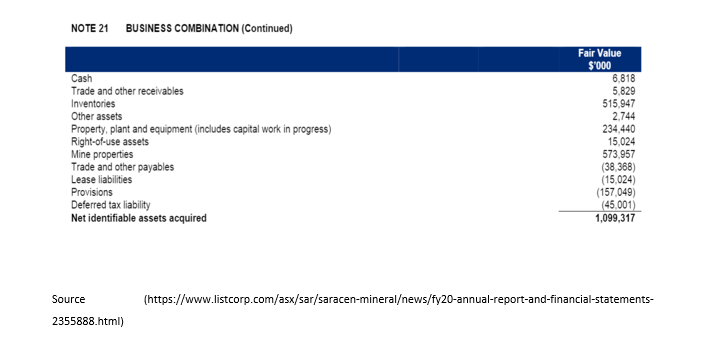

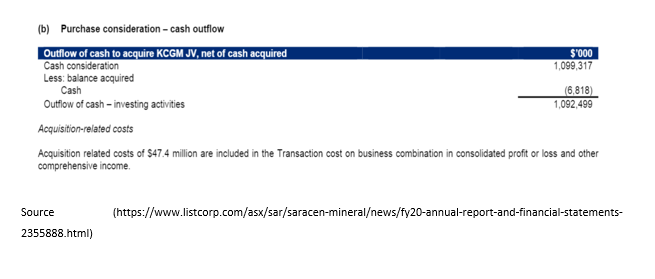

On considering the business of Saracen Mineral and its market value, Board is willing to expand a budget of AUD 1099.31million (Saracen Mineral Holdings 2019) Various business valuation methods have been applied to assess the most realistic value for the business of Saracen Mineral .

Business Valuation Methods

? Net Asset Method

Net Asset Method is one of the business valuation methods that derive the value of an entity's business by deducting all the liabilities of the entity from its total assets. The following formula may be used to derive the net asset of the business.

Net Assets = (Assets in Total – Total Liabilities – Preferred Stock) / Outstanding Equity Shares

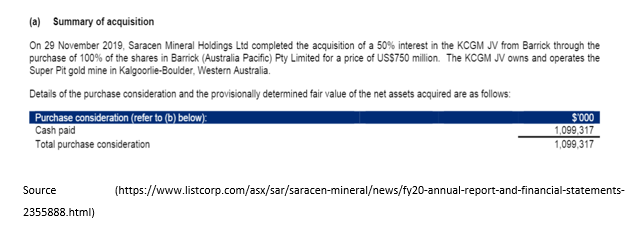

Net Asset (NAV) Valuation helps to understand the real worth of the business. The acquirer firm always wants to assess the value of the acquired firm to offer the best bid price. SARACEN MINERAL HOLDINGS is getting the value of 50% by paying a sum of $ 750 million which is a very great deal for the entity. This will add value to the wealth of the shareholders in the coming future (Saracen Mineral Holdings 2019)

? Price-Earnings (P/E) Ratio

Price-Earnings (P/E) ratio is used to determine the value of the business by comparing the share price of an entity's share with its earnings (EPS) per share (Anwar, (2019)). PE ratio helps to understand whether the share price of an entity is undervalued or overvalued. This ratio helps to know the value that an investor may pay for an entity's share on the earnings of the entity (Wibowo & Radianto, (2019)). The P/E ratio of KCGM is 24.14 and the P/E ratio of the industry in which Kalgoorlie Consolidated Gold Mines Operates is 18.6. This means that the share price of KCGM is undervalued and it is a great opportunity for us to make our investment in KCGM 's Business.

? Discounted Cash (DCF) Flow

Discounted Cash (DCF) Flow is one of the business valuation methods that consider the present value (PV) of all the cash flows that are expected from the investment proposal. The present value (PV) of future cash (FCF) flows are added with the present value (PV) of Terminal value (TV) to arrive at the total value of the business (Fernandez, (2019)). The following images are presented to show the business value of Kalgoorlie Consolidated Gold Mineson the basis of the DCF method:

According to the above calculation, the value of each share of KCGM is lower than market price of its share. This means that the share of the company is undervalued and the company has the potential to grow shortly that making it a great investment opportunity that will surely bring value addition to SARACEN MINERAL HOLDINGS and will help in increasing the wealth of its shareholders in near future.

Compliances

? Appropriate standards for corporate governance along with legal compliance are required to be established by the management to proceed with the acquisition.

? Statement on Corporate Governance along with ASX Appendix is required to be approved

? Charter of Board committee is required to be approved

Risk Management

? Framework for managing the overall risk of the company is to be approved.

? Policies regarding risk management, taxes, and financials are required to be approved.

? Due Diligence shall be exercised to make sure that the company is complying with all the required obligations.

Human resources

? Selection, Remuneration, cessation, and termination terms for the Managing director along with the CEO are required to be approved.

? Performance objectives for every person shall be set.

? Incentive plans for the employees shall be considered by the board.

Health & Safety

? Board is required to consider the reports on health & safety along with the environment.

? It shall be made sure that the health & safety of the entity's people is not compromised at any cost and the entity complies with all the environmental obligations.

? Policies related to health & Safety shall be approved.

? Policies related to Environment shall be approved.

References

Anwar, Y. (2019). The effect of return on equity, earning per share, and price earning ratio on stock prices. The Accounting Journal of Binaniaga, 4(01), 57-66.https://stiebinaniaga.ac.id/e-journal/index.php/Accounting/article/download/314/264

Cloyne, J., Ferreira, C., Froemel, M., & Surico, P. (2018). Monetary policy, corporate finance, and investment (No. w25366). National Bureau of Economic Research.https://www.nber.org/system/files/working_papers/w25366/w25366.pdf

D'Amico, G., & De Blasis, R. (2020). A review of the Dividend Discount Model: from deterministic to stochastic models. Statistical Topics and Stochastic Models for Dependent Data with Applications, 47-67.https://arxiv.org/pdf/2001.00465

Fernandez, P. (2019). Three residual income valuation methods and discounted cash flow valuation.http://pruss.narod.ru/ThreeIncome_OneDCF.pdf

Kadim, A., Sunardi, N., & Husain, T. (2020). The modeling firm's value is based on financial ratios, intellectual capital, and dividend policy. Accounting, 6(5), 859-870.http://m.growingscience.com/ac/Vol6/ac_2020_48.pdf

Sahoo, V. D. Investors perception on Dividend Policy and Valuation Models (2020) .https://www.academia.edu/download/79810078/13635.pdf.pdf

Siziba, S., & Hall, J. H. (2021). The evolution of the application of capital budgeting techniques in enterprises. Global Finance Journal, 47, 100504.https://repository.up.ac.za/bitstream/handle/2263/74586/Siziba_Evolution_2020.pdf?sequence=1

Wibowo, A. I. L., Putra, A. D., Dewi, M. S., & Radianto, D. O. (2019). Differences In Intrinsic Value With Stock Market Prices Using The Price Earning Ratio (Per) Approach As An Investment Decision Making Indicator (Case Study Of Manufacturing Companies In Indonesia Period 2016-2017). Aptisi Transactions On Technopreneurship (ATT), 1(1), 82-92.https://att.aptisi.or.id/index.php/att/article/download/23/6

- BUSM4738 Strategy Assignment

- STATS7061 Statistical Analysis Assignment

- MBA642 Project Initiation, Planning and Execution Report 3

- MBA403 Financial and Economic Interpretation and Communication Assignment

- MATH11247 Foundation of Mathematics Assignment

- GAL613 Grief and Loss Assignment

- FINM4100 Analytics in Accounting Finance and Economics Report 2

- TBUS610 E Business Strategies Assignment

- MGT605 Business Capstone Project 2A Report

- MBA5006 Managing Organisational Behaviour Assignment

- LAW3700 International Trade Law Assignment

- STT500 Statistics for Decision Making Assignment 2

- Financial Management Assignment

- MBIS4008 Business Process Management Report 2B

- EDES105 Indigenous History and Culture

- HI6006 Competitive Strategy Assignment

- BE955 International Marketing and Entrepreneurship Assignment

- Business Research Project Report

- MIS101 Information Systems for Business

- BDA601 Big Data and Analytics Case Study

.png)

~5.png)

.png)

~1.png)

.png)