BEAFGE Business Economics and Finance in a Global Environment Assignment Sample

A. Project question

You have received an email from the Chief Executive Officer of Clark Casc Logistics plc, where you are employed as manager of the refrigerated goods division, inviting you to the first in a series of budget-setting meetings and asking you to submit a brief report in advance for assignment help.

You are only permitted to submit your report once. Trial runs are not permitted and no spare, draft or test drop boxes will be provided. It is your responsibility to submit your own work and to ensure that your report is finalised, complete and properly edited before, not after, you submit it.

This is an individual assignment. The sharing of files or copying of work between students is not permitted.

You are only allowed to submit one document, which must contain your full report, including your reference list. Do not attempt to submit additional documents.

Your submission must be either a Word document in .doc or .docx format or a .pdf document.

Appendices are not permitted.

Dear “Laser”,

For the last financial year Clark Casc Logistics plc made a profit of £32 million – with profits of £18 million in the first six months of this year and the Board believes that there is scope for continuing expansion. We are therefore reaching out to all managers to provide realistic budgets for the income and costs for which they are responsible, so that we can plan ahead with confidence.

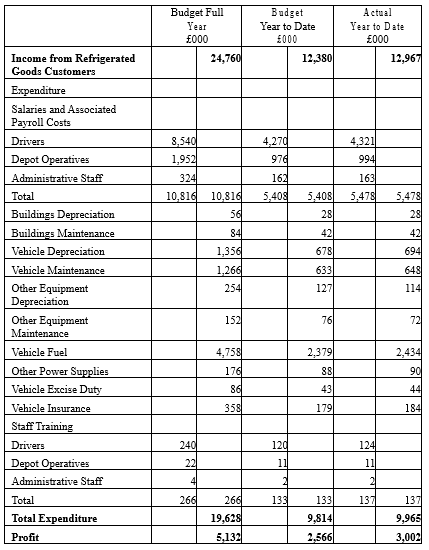

We will be holding a first round of budget-setting meetings on Thursday next week. As the manager of the refrigerated goods division, the income and expenditure for which you were responsible for the last financial year were as follows.

Your expenditure for the first six months of the present financial year is as follows, with a comparison with the budget which, I would remind you, you agreed to this time last year.

Year Ended April 30th 2022

Six Months to October 31st 2021

Refrigerated Goods

Next Year: Year Ending April 30th 2023

The purpose of next week’s meeting is not to congratulate ourselves on past profits but to plan for the future.

We already have a budget for the rest of this year and monitoring progress against this is an entirely separate exercise and not the purpose of this report, so do not include any budget monitoring information, as we already have that.

We need a realistic budget for income and expenditure, to tell us how much sales income we intend to make and how much we are going to have to spend to earn it. This year is already underway and what we need is a budget for next year. We need this budget to be agreed well in advance, so that we can make the necessary commitments and contractual arrangements for all our planned expenditure.

Please provide a report in advance of the meeting detailing your budget for the year ending April 30th 2023.

The format of the proposed budget is up to you, as is the method by which you arrive at the budget. However, please include the following sections in your report. We do not require an executive summary:

1. Introduction

2. Approach to evaluation of the proposed investment in a new depot

3. Evaluation of the proposed investment in the new depot

4. Approach to drawing up the refrigerated goods department budget

5. Relevant calculations to show that your budget for the year ending April 30th 2023 is realistic

6. Your proposed budget for the year ending April 30th 2023 with complete income and expenditure figures

7. A conclusion on the levels of income and expenditure in your department and on the likely result of building the new depot

8. Recommendations on the new depot proposal, including a recommendation on whether or not to proceed with it, and on the next steps in managing resources in the refrigerated goods department

Please make sure you provide a list of references to any published external material you refer to in your report.

Make sure your report is at least 2,250 words to prove you’ve done some work but I’m not reading it if it’s more than 2,750 words apart from the references. I will not waste time reading appendices. If you have something to say, say it in your report.

Our growing sales income has already enabled the Board to give employment to the Chief Executive’s son and I was frankly astonished to find that he has been assigned to the Finance department. As I am struggling to find any real use for his talents, I will be reading your report carefully for signs that you “need help” with financial matters, in which case I will have no hesitation in sending young Tony to “help” you on a daily basis.

Best Wishes,

Iain

“Until a man dies, wait and until then never call him happy but only fortunate.”

Herodotus

This email contains confidential information relating to Clark Casc Logistics plc. If you are not the intended recipient delete this email immediately.

Further information

As manager of the refrigerated goods division you are responsible for sales income from the transport of refrigerated goods.

Note that the figures above are for six months. You are required to provide a budget for a full year and not for six months only.

You are responsible for pricing and negotiating each contract. You have complete discretion over pricing and all refrigerated goods contracts must be signed by you or somebody authorised by you. You usually start by offering a price based on £0.22 per tonne per kilometre. However, if a prospective client has asked for sealed bids in a competitive bidding process you submit a bid priced at £0.19 per tonne per kilometre, which is approximately the average price you are able to negotiate with customers.

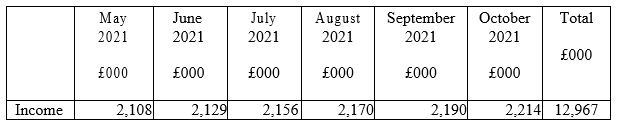

The sales income generated by your department over the past six months has been as

As manager of the refrigerated goods division, you are responsible for the following costs:

Salaries and Associated Payroll Costs

In addition to the salaries below, Clark Casc is required to pay Employer’s National Insurance Contributions. Employer’s National Insurance Contributions are presently assessed as 13.8% of each employee’s salary, including bonuses but excluding the first £8,840 of the employee’s annual salary.

Clark Casc is also required to pay an additional 0.5% of total salaries, including bonuses, as an apprenticeship levy.

Clark Casc also contributes to an employees’ superannuation scheme. Clark Casc’s contribution is 8.5% of all staff salaries, including bonuses.

All of these costs are part of your budget.

Heavy Goods Vehicle Drivers:

You have 202 drivers earning an average base salary of £35,000 per year. Each driver can presently cover about 125,000 miles per year. Last year, all drivers also qualified for a bonus of 10% of base salary for accident-free driving and there have been no vehicle accidents this year.

Employer’s insurance is handled centrally and is not part of your department’s budget.

Refrigerated Goods Depot Operatives

You have 97 operatives working at you refrigerated goods depot, earning an average salary of £19,000 per year.

Administrative Staff

You have 11 administrative staff in the refrigerated goods department, earning an average salary of £27,000 per year.

Property Plant and Equipment

Vehicles

Your department uses 151 heavy goods vehicles and 16 other vehicles, all of which are owned by Clark Casc. Each vehicle has an estimated useful life of 12 years in the company after which it can be resold for an estimated 10% of its original cost. The average replacement cost of a heavy goods vehicle is presently £120,000 and the average replacement cost of other vehicles is £24,000 per vehicle. You are responsible for the cost of depreciation on these vehicles. Depreciation is to be charged at current replacement cost.

Vehicle Excise Duty

Vehicle Excise Duty varies from vehicle to vehicle but is an average of £560 per vehicle per year for heavy goods vehicles and an average of £220 per vehicle per year for other vehicles.

Vehicle Insurance

Your vehicle insurance costs average £2,400 per vehicle per year for heavy goods vehicles and £400 per vehicle per year for other vehicles.

Other Equipment

You have just completed a major exercise with the finance department to establish what equipment you are using at the refrigerated goods depot and in the office. The annual depreciation cost at current replacement cost for this equipment is £228,000.

Equipment insurance other than vehicle insurance is handled by another department and is not part of your budget responsibilities.

Buildings Depreciation

The depot and office which you occupy have a current replacement cost of £3,500,000 and a useful life of 50 years. The land which they occupy has a current resale value of £600,000 and the scrap value of the building materials is estimated at £100,000 at current prices. You are required to budget for depreciation on the buildings on a straight-line basis.

Buildings Maintenance

Buildings maintenance, including cleaning, is carried out by the in-house Buildings Maintenance Department and recharged to your department. It is a fixed cost and averages £7,000 per month.

Equipment Maintenance

Vehicle Maintenance

Clark Casc’s vehicle maintenance department is under separate management. You are responsible for booking the vehicles in your department in for repairs, routine maintenance and annual testing. You are also responsible for ordering the recovery of any vehicles which have broken down or been involved in accidents. All of these

services are managed by the vehicle maintenance department. There have been no motor vehicle accidents in your department in the last 18 months.

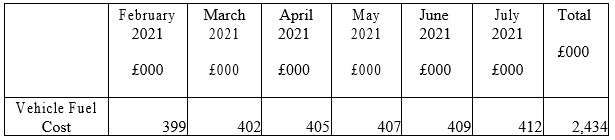

Vehicle maintenance is a semi-variable cost.

The vehicle maintenance costs charged to your department over the last six months have been as follows:

The sales income generated by your department over the past six months has been as follows:

Other Equipment Maintenance

Depot and office equipment maintenance is a fixed cost and averages £12,000 per month.

Fuel and Power Costs

Vehicle Fuel

Vehicle fuel is a semi-variable cost.

Total vehicle fuel costs for the last six months have been as follows:

Other Power Supplies

Gas and electricity supplies to the depot and office are a fixed cost and average £15,000 per month.

Staff Training

The cost of drivers’ training averages £1,225 per driver per year, including fees for Certificates of Professional Competence.

Depot operatives’ training costs average £225 per operative per year. Administrative staff training costs average £275 per person per year.

Other Costs

There are no other costs in your budget. All other costs, including legal costs, employer’s insurance, public liability insurance and insurance of buildings and non-vehicle equipment, are handled by other departments and you are not responsible for managing them.

Step Fixed Costs

You presently have enough drivers and vehicles to meet demand up to 140 million tonne kilometres per year (£26,600,000 sales income per year at £0.19 per tonne kilometre). To fulfil orders above this level you will need 2 extra drivers and 1 extra heavy goods vehicle for every 1.4 million extra tonne kilometres per year (£266,000 sales income per year at £0.19 per tonne kilometre).

Proposed New Depot

If sales exceed 150 million tonne kilometres per year (£28,500,000 sales income per year at £0.19 per tonne kilometre), your department will need a new depot of the same size and with the same number of depot operatives as the existing depot and you will also need 3 additional administrative staff with salaries of £27,000 per year each. It will take 12 months to build a new depot and bring it into use and Clark Casc will have to pay the builders before it is complete.

You are responsible for deciding whether to make this extra investment in a new depot or not. You are not responsible for deciding on how to finance it. However, you have been told that further investments are required to make a return of at least 9% per annum and that this is to be used as the discount rate in any discounted cash flow calculations.

Additional Information

You are the manager of the refrigerated goods department and you have full access to any additional information required. If more information is required from a published, broadcast or webcast source, you must present that information with a proper reference in the normal referencing format required in the business school. If further information would be required from internal sources at Clark Casc, you must create that information yourself for use in drawing up your report and provide your own indication of internal sources.

You must not present a report which concludes that information is incomplete, or that further information is required or which recommends that further information is obtained. This would be a clear indication that you have not completed your report as required.

Required:

Write your report, addressed to the Managing Director of Clark Casc and containing the following sections, as directed in the Managing Director’s email. Submit your report in the Turnitin dropbox.

1. Introduction

2. Budgeting Approach

3. Relevant Calculations, including any investment appraisal

4. Proposed Income and Expenditure Budget

5. Conclusion

6. Recommendations

7. References

Your report must be between 2,250 and 2,750 words in length excluding references.

Do not include an executive summary.

Appendices are not permitted.

Solution

Introduction

The term forecasting is associated with the aspect of predicting the future expected outcome by analysing the present situation. As we are all know, that being human, it is difficult to watch the future, but on can make an predication about the possibility. The corporate leaders or business leaders, use their skill and the methods, along with the past data for projection of future projected outcome. Forecasting is the systematic approach of examining the future. Forecasting sales in this context refers to the act of producing a prediction about future sales, followed by a careful investigation of data linked to future events and factors that may effect the entire firm. This budget report is drafted based on the past experience, the prevailing situation of business and the expectation of top management. (Ogun Bayo, B. F., Alibaba, C. O., Thala, W. D., & Akinradewo, O. I. (2022).

As a head of the refrigerator department, I believer, that every corporate operates under the Isolated business environment and they are open to influence by the factors associated in the business environment. the smart business tried to take an advantage through continues scanning, reviewing and analysing the operation and non-operation activities surrounding the business. All these activities are essential for continues growth and development of business. Further scanning, analysing, reviewing, planning, controlling and formulating the action plans are some key elements which are widely associated with business. After associating myself with Clark Cask Logistics plc, and after reviewing the work culture in the corporation. I feel that the planning and budgeting is the primary requirement for continues growth of business. Any decision with logical reason, required detail research, as well as this decision required continues observation of business environment. this budget report is drafted based on the experience gain in last year, as well as observing the overall strength of my department and considering that this budget report shall be realistic one. We have seen numbers of opportunities in the competitive business environment, but we sometime wait to check the actual reaction of change in the market.

Approach To Evaluate The Proposal To Invest in New Department

The growth and expansion of any business is the outcome of hardworking, delegation and continues commitment from the all the people associated with the company and the various department. projection about the future inflows and flows are made based on the overall demand for customer as the company market share in the competitive environment. further business is also required to update and up-grade them self, with the change in the business environment and level of competition. The expansion strategy of business can be carried out either by acquiring control over the competitor or by reinvesting the in exiting business by adding funds in exiting operation. Either of the selected option will result into growth of business and which will enhance the capacity of company to serve more and more customers. However, this decision of expansion of operation or the decision to enhance the operating capacity, again suffers from the numbers of drawback, hence it is essential to make proper research, before adding new capital either in exiting operating capacity or to expand the business operation. Here in current case, our management are on the option that we are in position to grow our business, considering these facts we have plan out to adopt some strategic action plan, at each division. It is totally true that we are in position to growth. But as the responsible person of the refrigerator goods department. I personally feel that before finally taking an decision for further, expansion or investment of funds in to the existing operation, we need to wait for another one year. (Nikodijevi?, M. (2021). the proposal of new investment is totally correct, but before finally deciding, or taking a finical conclusive decision. We are supposing consider the growth rate in sales of industry as whole as well as the growth of sales of our department from one year or another year. based on the growth in sales of during first 6 months, it can be projected that the refrigerator department will continues to grow at the stable rate, however as the industry is growing and our top executive also feel that we have a opportunities to expand, then in such a situation we can project that refrigerator department can grow at the rate of 10 % in total sales, this growth rate Is seem realistic, and if we consider this growth rate, then the budged sales will be nearly to £27000000, this situation does not permit use to make an further investment in new plan, rather we can go with the option of adding some more resources, which can help our operation to work smoothly and deliver the product and services with high quality standard. Here we can adopt the approach of being aggressive but with suitable Calculation. Here we will adopt the approach of adding new resources and expanding the operation in next one or two years. Further even if we take a decision for further investment in this department, it will start operating after a year.

This decision shall not be limited with the final conclusion to avoid investment in department in order to expand the operation strategy. As we are in middle of year, we are can wait for next 6 month in order to oversee the actual performance of industry as whole, the competitor position and the reaction of our customers. The new investment decision will result into the high outflow of cash. this decision required to consider the opportunity cost with this investment planning. Hence it is best suitable for wait for some time let say 6 months, and then after again the meeting shall be called to take a decision to start new operation division.

Evaluation of Proposed Investment in New Department

Starting the new department is always indicate that business is growing and creating new opportunities, but it is not means that we shall make an investment to start a new division, without being considering the negative phase of propose investment option. If the top management feel that it will be best suitable to make an investment in new division, then we need to consider the fact about the possible operating outflow, and expected inflow. Here we need to compare the proposal with the inflow and outflow. Cost benefit analysis is always advisable to consider. Here, the major investment is the capital investment, and I believer that out company is in sound position to make such investment. This addition division strategy will be suitable when it gives the high in sales by more than 25 % as again the current level of sales. In addition to that if the new department is in position to grow the net earnings by more than 12 % than again this investment option is best suitable, as here we believe that the nominal rate of return is nearly 7 %, which again indicate the risk-free return. Hence it is essential to consider that the new investment plan in department will contribute in net profitability of not less than 9 %. The second condition which as the superior authority at the department, I also think that the new department must be in position to give some additional benefits to the society at large as well as to the current and prospective customers. The further investment in new department also required supportive level of sales, which are nor less then £28,500,000, if we are fail to get this level of sales, than it become hard for our department to justify that our suggestion was correct, and we are in position to use the invested resources in productive ways. the new investment in department required, new deport with the same size, nearly 97 new of operators, whose average salaries are nearly to the existing staff, £19,000 per year. additional 3 administrative staff, whose expected salary are not less than £27,000 per year for each employee. Further this proposal will take nearly 1 year to build the new deport in order to bring into the usage and it is essential that our company shall allocate the space and allocate the work to the builder before it is complete. This outflow will not end here with as we are planning to enhance the operating capacity the additional investment in vehicles, driver, training to new staff, etc are some associated with the outflow and they will surly incurred. The new division will result into continues outflow for the fixed as well as operating expense, the expected sales level may not be in position to justify these expenses, however if we believe that out division will grow at the average rate, that is nearly 10%, then we are position to justify the expected outflow with the sales and profitability along with the return on investment.

Relevant Calculation To Associated with Budget

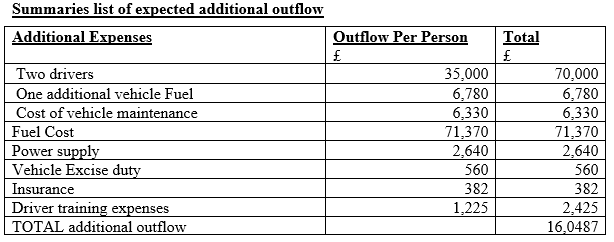

Instead of investing in new division, at this level we are can consider this option as the next level, and present we shall make certain amount of investment activities to enhance out ability to serve the customer. Our team believe that during the year ended 2023; we are in position to achieve the sales at the growth rate of 10% by taking the based budgeted sales of 2022. This sales required one additional vehicle, two additional driver. (Nikodijevi?, M. (2021).

This additional injection of new workforce will result in to additional outflow in driver salary. Additional outflow to Purchase new vehicle and additional cost of new vehicle for maintenance, fuel, vehicle excise duty, training expenses for the driver.

The above stated table shows the additional outflow one account of reaching our sales in excess of expected level. Here this expenses or additional investment can be justified by the level of sales we can achieve, the growth in the sales by nearly 10 % is suitable considering the fact about the overall growth of industry as well as again the inflection found in the market. Additional of two driver and one vehicle will enhance the strength of department and we are in position to boot our sales and improve the overall services in order to maintain the customer based as well as to maintain the strength of our department.

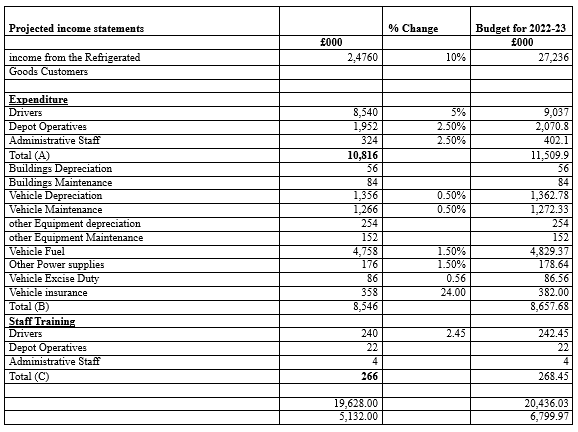

Computation of budgeted statement showing income and expenditure for the year ended on April 30th 2033

Conclusion on income and expenditure over the refrigerator goods department

The above stated calculation shows the budgeted inflow and outflow based on the income year of 2021-22. Here major focus is given toward the overall growth in expenses and the income, further a change for the year ended 2023 as again 2022, is reflected in form of percentage (Hartanto, 2018). This can make the statement user-friendly for every interested stakeholder of this department. the drafted budget report shows the growth in sales by 10 %, along with minor to major change in the operating expenses, however we have assumed that there isn’t any addition of new building, hence the cost associated with building maintenance and depreciation will be same as it was in the previous year. major change is found in the area which are variable in nature and such expenses will continues to be change due to change in overall price, tax rate, and others expenses which are not in the control. Further the above budgeted report also excludes the employee insurance contribution, bounds to the employees and other benefits which employees are eligible to receive, these benefits and the outflow for the company are in addition to above stated projection, the average percentage of this additional expense will be 5 % of sales. The above stated budget shows the comparative data of two year, here we can see the change in all major expenses, except those which are fixed in nature, such as the non-cash expenses.

Recommendation for New Deport Proposal.

After going through the above stated discussion, and after analysing the possible benefits and the drawback of adopting and investment option of new department., we are on conclusion that instead of investment this major amount to expand operation, we need to wait for next 6 month or till the end of current financial year, at the year end we are in position to know the growth of industry and overall demand of our product and services. If there is a unexpected growth in sales for next 6 months then we should plan to make additional investment, and if we are not in position to observe the expected level of growth in sales and revenue than we shall drop an plan for new deport proposal.

References

Ogun Bayo, B. F., Alibaba, C. O., Thala, W. D., & Akinradewo, O. I. (2022). Assessing maintenance budget elements for building maintenance management in Nigerian built environment: a Delphi study. Built Environment Project and Asset Management. https://doi.org/10.1108/BEPAM-06-2021-0080

Nasri, H., Nurman, N., Azwirman, A., Zainal, Z., & Riauan, I. (2022). Implementation of collaboration planning and budget performance information for special allocation fund in budget planning in the regional development planning agency of Rokan Hilir regency. International Journal of Health Sciences (IJHS) Ecuador, 6(S4), 639-651. https://doi.org/10.53730/ijhs.v6nS4.5597

Nikodijevi?, M. (2021). Implications and challenges of using driver-based budgeting in contemporary business environment. Trendovi u poslovanju, 1(17), 49-57. https://scindeks-clanci.ceon.rs/data/pdf/2334-816X/2021/2334-816X2101049N.pdf

Hartanto M. R. (2018). Implementation of Performance-Based Budgeting: A Phenomenological Study on National Land Agency. International Journal of Scientific Research and Management. Vol. 6 No. 02 (2018). https://ijsrm.in/index.php/ijsrm/article/view/1277

Moses, M. (2022). Inside the Crisis of Municipal Budgeting. In The Municipal Financial Crisis (pp. 27-52). Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-030-87836-8_1

- TITP105 The IT Professional Report

- ISYS1003 Cybersecurity Management

- Knowledge and Attitudes of Nursing Students About Pain Management Assignment

- SITXSA002 Participate in Safe Food Handling Practices Instruction Assignment

- MIC11108 Drug Delivery System

- MGT607 Innovation Creativity and Entrepreneurship Report

- Impact of Firms Intangible Assets on Price Volatility

- 2128IBA Business Processes

- Microservices Architecture Assignment

- MIS609 Data Management and Analytics Case Study

- SBM1203 Business Finance Assignment

- MGT605 Business Capstone Project Report

- BMP4002 Business Law Assignment

- IM501 Agricultural Data and Information Management Report 2

- MITS5501 Software Quality Change Management and Testing Assignment

- BMP4005 Information Systems and Big Data Analysis Assignment

- Constantina Case Study Adult Female Marathon Runner Assignment

- BUS6101 Business Information System Report 3

- 3155IBA Operational Management Assignment

- DATA4100 Data Visualisation Software Rp 4

.png)

~5.png)

.png)

~1.png)

.png)