Order Now

- Home

- About Us

-

Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

-

Assignment Writing

-

Resources

- Referencing Guidelines

-

Universities

-

Australia

- Asia Pacific International College Assignment Help

- Macquarie University Assignment Help

- Rhodes College Assignment Help

- APIC University Assignment Help

- Torrens University Assignment Help

- Kaplan University Assignment Help

- Holmes University Assignment Help

- Griffith University Assignment Help

- VIT University Assignment Help

- CQ University Assignment Help

-

Australia

- Experts

- Free Sample

- Testimonial

LAW6001 Taxation Law Case Study Sample

Task Summary

In response to the issues raised in the case study provided, research and develop a 3000-word tax advice that addresses (a) assessable income (b) allowable deductions (c) tax calculations and (d) your conclusions and recommendations that arise from a fact scenario and to give appropriate advice to clients. Please refer to the Task Instructions for details on how to complete this task.

Context

This assessment allows students to solve practical problems that arise from various scenarios and to give appropriate advice to clients. This assessment assesses your research skills, your ability to synthesise an original piece of work to specific content requirements and your ability to produce a comprehensible piece of advice which addressing the client’s needs.

It also assesses your written communication skills. The ability to deliver to a brief is an essential skill in the workplace. Clients may well approach advisors seeking a combination of specific information needs and advice on the tax implications of a particular arrangement in the Australian tax jurisdiction. It is therefore important to be able to identify all the issues presented by an arrangement and to think about the potential consequences of different approaches to addressing the client’s needs.

Task Instructions

• This case study must be presented as a group effort. The case study requires collaboration of effective team work. It is expected students will take parts and survey the relevant literature, including decided cases, and select appropriate additional resources.

• Your case study is not just a list of answers. Your reasons for your conclusions and recommendations must be based on your research into the relevant cases and legislation.

• With respect to each case study:

• Advise the best investment option for clients from the facts of the case study

• Identify the appropriate legal principles that requires discussion in the case study

• Apply the law to the facts of the case study

• After reaching a relevant conclusion, provide practical advice to your client(s).

• Your case study needs to identify and discuss the tax implications of the various issues raised.

• A report (word document, approx. 3,000 words) must be submitted for the calculations of the assessable income; allowable deductions and taxable income of the taxpayer including identifying and discussing them. E.g., how the amounts of income & deductions have been derived. If any receipts and payments are not assessable or deductible, the reasoning for non-inclusion of these in assessable income or deductions as per relevant legislation or cases. After all analysis, you must provide the best solution to save income tax payable.

• Your case study is not just a list of answers. Your reasons for your conclusions and recommendations must be based on your research into the relevant cases and legislation.

Solution

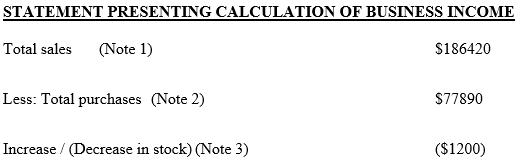

Case 1

Working Notes

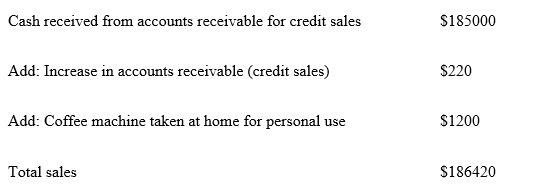

Notes 1 Total sale

In case any item of business trading stock is used for private purpose then in accordance with assertions provided by Australian taxation office; it is considered to be sold and its value is accounted in business assessable income. For Assignment Help, In present case as coffee machine has been taken to home for personal use it would be recognized as part of business income (Using trading stock for private purposes, 2020).

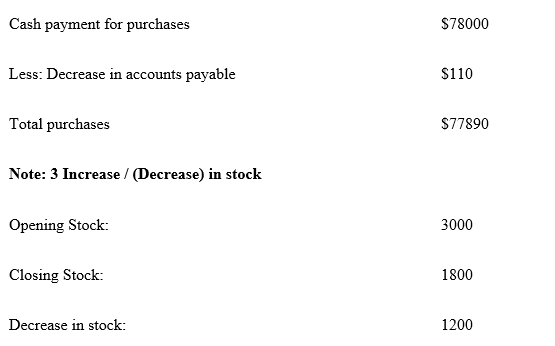

Note 2: Total purchases

In accordance with Para 9 of AASB 102, inventories are required to be measured at lower of cost or net realisable value. In present case the cost of inventory in 2000 and net realisable value of same is 1800; thus it would be recognized at 1800 i.e. lower of net realisable value or cost (AASB 102 Inventories, 2020).

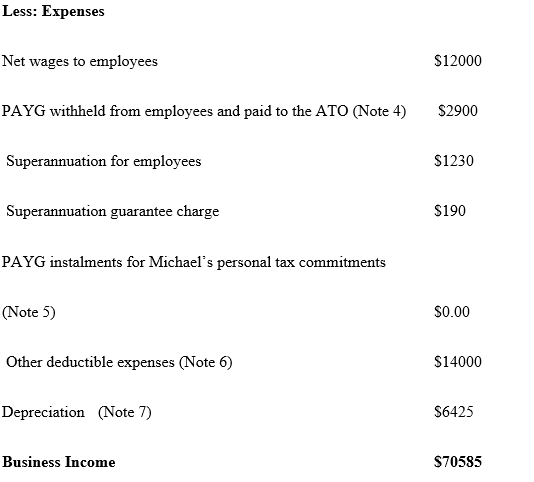

Note: 4 PAYG withholding

As per ATO provisions, employers does have responsibility to assist payee in accomplishing their tax liability and same is done through withholding payments from the amount paid to employees; thus it is part of salary or wage and deductible expense as well (Creighton, 2017).

Note 5: PAYG for personal tax commitments

When income or business receipts a certain amount as per taxable provisions; one is required to make payment of income tax instalment which could be quarterly or monthly. PAYG instalment assist in avoiding large bill; thus it is not a business expense hence no deduction would be available regarding same (Wollner, Barkoczy & Murphy, 2020).

Note 6: Other deductible expense

Other deductible expenses include decline in value of assets. It is assumed company complies with policy of accounting assets at market value, thus decline in values is being written off year. Hence same is deductible expenditure (Mather, 2018).

Note 7: Depreciation

Depreciation of coffee machine on straight line basis for each year

62000/10 =6200

For year 2020/21; it would be charged for 11 months i.e. 6200/12*11 =$5683

Depreciation of BMW motor vehicle on straight line basis for each year

89000/8 i.e. 11125

As vehicle is purchase on 1st May 2021, depreciation would be charged for 2 months and 40% only as it is used for business to specified extent only.

11125/12*2*40%

= 742

Total depreciation = 5683+742 =6425

Other notes and assumption

• It has been provided that cash receipts have been received as contribution by Michael to expand the business; thus it is a capital receipt and not considered as part of business income.

• Further cash drawings of $3000; are personal drawing thus same would be reduced from capital and not considered while calculating business profits.

• Payment of penalty for breach of Australian Customer regulation of $900 is not allowable as business expenditure; thus same would not be considered while evaluating business income.

• It has been assumed that company complies with straight line method of depreciation on its assets; thus same has been applied for calculating depreciation for motor vehicle and machine.

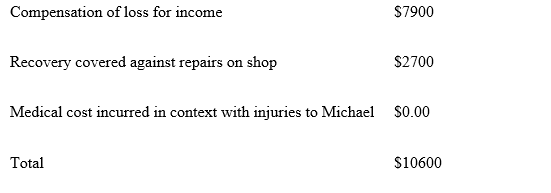

STATEMENT PRESENTING CALCULATION OF OTHER INCOME

Notes: In accordance with Australian taxation office provisions, insurance payout in context with personal items is not taxable. It includes insurance recovery received for family home or personal injury is not taxable. Thus, in present case recovery for medical relating to injury of Michael would not be taxable. However, other recovery i.e. receipts regarding business or income producing assets is to be taxed. Thus, compensation for loss of income as well as recovery against recovery of shop would be considered in assessable income as it is relating to personal.

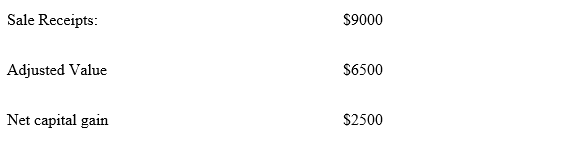

STATEMENT PRESENTING CALCULATION OF CAPITAL GAIN ON SALE OF MOTOR VEHICLE

Note: An assumption has been made that motor vehicle has been used for more than one year and adjustable amount represents amount after making adjustment in context with depreciation and other deductions. In accordance with taxation provision of Australian taxation provision, gains on assets which are held by individuals for minimum period of twelve months would be considered as long term capital gains and they are subject to 50% exclusion.

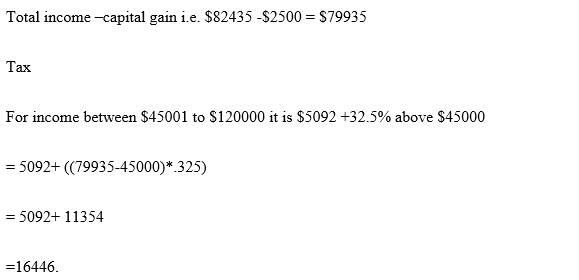

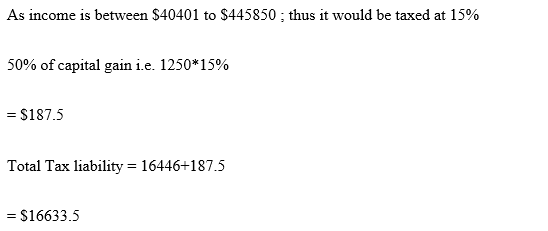

STATEMENT PRESENTING NET TAX LIABILITY OF MICHAEL PAYABLE FOR YEAR 2020/2021

.png)

.png)

Working Note:

Tax liability on ordinary income

Tax on capital gain

References

.png)

Download Samples PDF

Related Sample

- NURS2193 Nursing Therapeutics and Aged Clients Assignment

- MBA621 Healthcare Systems

- PROJ6003 Project Execution and Control

- PRJ6001 Applied Project Assignment

- LMED28003 Outline of The Innate and Adaptive Immune Systems Report 2

- CPCCOM1013 Plan and Organize Work

- LMED28002 Haematopathology Case study 1

- COIT20262 Advanced Network Security Assignment

- BIS3004 IS Security and Risk Management Assignment

- BE275 Global Supply Chain and Operations Management Assignment

- MBA611 International Strategy Report

- ACCT6007 Financial Accounting Theory and Practice Research Report

- MIS609 Data Management and Analytics Assignment

- HI6005 Management and Organisations in a Global Environment Report

- LB5236 International Political Economy Report

- MBA Capstone Strategy Assessment

- PUBH6012 Capstone B Applied Research Project in Public Health Assignment

- MANU2123 External Project Proposal Assignment

- MBA642 Project Initiation Planning and Execution Assignment

- BUSM4177 Leadership and Decision Making Assignment

Assignment Services

-

Assignment Writing

-

Academic Writing Services

- HND Assignment Help

- SPSS Assignment Help

- College Assignment Help

- Writing Assignment for University

- Urgent Assignment Help

- Architecture Assignment Help

- Total Assignment Help

- All Assignment Help

- My Assignment Help

- Student Assignment Help

- Instant Assignment Help

- Cheap Assignment Help

- Global Assignment Help

- Write My Assignment

- Do My Assignment

- Solve My Assignment

- Make My Assignment

- Pay for Assignment Help

-

Management

- Management Assignment Help

- Business Management Assignment Help

- Financial Management Assignment Help

- Project Management Assignment Help

- Supply Chain Management Assignment Help

- Operations Management Assignment Help

- Risk Management Assignment Help

- Strategic Management Assignment Help

- Logistics Management Assignment Help

- Global Business Strategy Assignment Help

- Consumer Behavior Assignment Help

- MBA Assignment Help

- Portfolio Management Assignment Help

- Change Management Assignment Help

- Hospitality Management Assignment Help

- Healthcare Management Assignment Help

- Investment Management Assignment Help

- Market Analysis Assignment Help

- Corporate Strategy Assignment Help

- Conflict Management Assignment Help

- Marketing Management Assignment Help

- Strategic Marketing Assignment Help

- CRM Assignment Help

- Marketing Research Assignment Help

- Human Resource Assignment Help

- Business Assignment Help

- Business Development Assignment Help

- Business Statistics Assignment Help

- Business Ethics Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Nursing

-

Finance

- Finance Assignment Help

- Do My Finance Assignment For Me

- Financial Accounting Assignment Help

- Behavioral Finance Assignment Help

- Finance Planning Assignment Help

- Personal Finance Assignment Help

- Financial Services Assignment Help

- Forex Assignment Help

- Financial Statement Analysis Assignment Help

- Capital Budgeting Assignment Help

- Financial Reporting Assignment Help

- International Finance Assignment Help

- Business Finance Assignment Help

- Corporate Finance Assignment Help

-

Accounting

- Accounting Assignment Help

- Managerial Accounting Assignment Help

- Taxation Accounting Assignment Help

- Perdisco Assignment Help

- Solve My Accounting Paper

- Business Accounting Assignment Help

- Cost Accounting Assignment Help

- Taxation Assignment Help

- Activity Based Accounting Assignment Help

- Tax Accounting Assignment Help

- Financial Accounting Theory Assignment Help

-

Computer Science and IT

- Operating System Assignment Help

- Data mining Assignment Help

- Robotics Assignment Help

- Computer Network Assignment Help

- Database Assignment Help

- IT Management Assignment Help

- Network Topology Assignment Help

- Data Structure Assignment Help

- Business Intelligence Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- R Studio Assignment Help

-

Law

- Law Assignment Help

- Business Law Assignment Help

- Contract Law Assignment Help

- Tort Law Assignment Help

- Social Media Law Assignment Help

- Criminal Law Assignment Help

- Employment Law Assignment Help

- Taxation Law Assignment Help

- Commercial Law Assignment Help

- Constitutional Law Assignment Help

- Corporate Governance Law Assignment Help

- Environmental Law Assignment Help

- Criminology Assignment Help

- Company Law Assignment Help

- Human Rights Law Assignment Help

- Evidence Law Assignment Help

- Administrative Law Assignment Help

- Enterprise Law Assignment Help

- Migration Law Assignment Help

- Communication Law Assignment Help

- Law and Ethics Assignment Help

- Consumer Law Assignment Help

- Science

- Biology

- Engineering

-

Humanities

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- History Assignment Help

- Cookery Assignment Help

- Auditing

- Mathematics

-

Economics

- Economics Assignment Help

- Managerial Economics Assignment Help

- Econometrics Assignment Help

- Microeconomics Assignment Help

- Business Economics Assignment Help

- Marketing Plan Assignment Help

- Demand Supply Assignment Help

- Comparative Analysis Assignment Help

- Health Economics Assignment Help

- Macroeconomics Assignment Help

- Political Economics Assignment Help

- International Economics Assignments Help

-

Academic Writing Services

-

Essay Writing

- Essay Help

- Essay Writing Help

- Essay Help Online

- Online Custom Essay Help

- Descriptive Essay Help

- Help With MBA Essays

- Essay Writing Service

- Essay Writer For Australia

- Essay Outline Help

- illustration Essay Help

- Response Essay Writing Help

- Professional Essay Writers

- Custom Essay Help

- English Essay Writing Help

- Essay Homework Help

- Literature Essay Help

- Scholarship Essay Help

- Research Essay Help

- History Essay Help

- MBA Essay Help

- Plagiarism Free Essays

- Writing Essay Papers

- Write My Essay Help

- Need Help Writing Essay

- Help Writing Scholarship Essay

- Help Writing a Narrative Essay

- Best Essay Writing Service Canada

-

Dissertation

- Biology Dissertation Help

- Academic Dissertation Help

- Nursing Dissertation Help

- Dissertation Help Online

- MATLAB Dissertation Help

- Doctoral Dissertation Help

- Geography Dissertation Help

- Architecture Dissertation Help

- Statistics Dissertation Help

- Sociology Dissertation Help

- English Dissertation Help

- Law Dissertation Help

- Dissertation Proofreading Services

- Cheap Dissertation Help

- Dissertation Writing Help

- Marketing Dissertation Help

- Programming

-

Case Study

- Write Case Study For Me

- Business Law Case Study Help

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- Case Study Writing Services

- History Case Study help

- Amazon Case Study Help

- Apple Case Study Help

- Case Study Assignment Help

- ZARA Case Study Assignment Help

- IKEA Case Study Assignment Help

- Zappos Case Study Assignment Help

- Tesla Case Study Assignment Help

- Flipkart Case Study Assignment Help

- Contract Law Case Study Assignments Help

- Business Ethics Case Study Assignment Help

- Nike SWOT Analysis Case Study Assignment Help

- Coursework

- Thesis Writing

- CDR

- Research

.png)

~5.png)

.png)

~1.png)

.png)