MPAA604 Advanced Audit and Assurance Assignment Sample

Instructions:

This assignment is to be submitted in accordance with the assessment information stated in the MPAA604 - Advanced Audit and Assurance Subject Outline.

Students have the responsibility to ensure that the submitted work is in fact their own work.

• Incorporating another source, information or ideas into one's own work without the appropriate acknowledgement through the correct in-text citation protocols is potentially grounds for academic misconduct.

• Students must submit all assignments for plagiarism checking in turn-it-in in Moodle prior to the final submission. For further details, please refer to the MPAA604 Subject Outline and the MPAA604 - Advanced

Audit and Assurance unit information in Moodle.

• Maximum marks available: 15 Marks.

• Refer to the marking rubric for the marking criteria on page 7 of this document for assignment help

• This assignment should be a total of 1,500 words (maximum).

• Please use the "word count" function and include the number of words in the report on the front cover page.

• Due Date: Week 10

Topic: How is Enhanced Auditor Reporting currently being embraced in Australia?

Background and Context:

Since 2016, there has been a strong push to improve the quality of audit reporting. Listed entities now have to report on "key audit matters" and improve the way material information is communicated using "plain English”. As mentioned in the CPA Australia podcast "How is Enhanced Auditor Reporting Being Embraced around the Globe?" (available at CPA Australia website):

“The IAASB's new auditor reporting requirements commenced in December 2016. Standard setters in many jurisdictions, including Australia and New Zealand, have issued the new requirements with the same effective date, whilst others have committed to issue the standards but have not yet done so. The UK have had similar requirements in place since 2013 and some firms in other countries have early adopted the IAASB's requirements. Jim Sylph, Co-chairman of the IAASB's Auditor Reporting Implementation Working Group, and Merran Kensal, IAASB member and AUASB Chairman spoke to CPA Australia about the uptake and impact of enhanced auditor reporting around the globe.”

Research Assessment:

Download an annual report of an Australian Securities Exchange (ASX) listed company that is in the S&P/ASX 300 list. Review all the sections within the selected company's annual report which relate to the Auditor's role in providing reasonable assurance over the entity's financial statements and control environment. Students will need to review and analyses the following key areas included in the selected company's annual report:

• Auditor's Independence Declaration

• Independent Auditor's report

Non-audit services performed by the auditor

• Auditors' remuneration

Role, functions and composition of the Audit Committee

• Independent Auditors' report to the members (shareholders)

• Review all Key Audit Matters noted and the associated audit procedures

Requirements:

Based on your analysis of the auditors' sections and other areas pertaining to the auditor, as included within the annual report, submit a report which summarizes and evaluates the auditor's assurance services performed for the client company.

As part of your review of the assurance services provided, consider the following:

• Has the auditor complied with Independence requirements?

• If there were non-audit services provided, what was the nature of such services?

• Provide an analysis of the auditor's remuneration in a table with prior year comparisons. Include percentage changes and explanations of the remuneration.

Assignment Report Structure:

1. Executive Summary

• The Executive summary should be concise and not involve too much detail.

• It should make commentary on the main points only and follow the sequence of the report.

Write the Executive Summary after the report is completed, and once you have an overview of the whole text. The Executive Summary appears on the first page of the report.

2. Contents Page - This needs to show a logical listing of all the sub-headings of the report’s contents.

3. Introduction - A short paragraph which includes background, scope and the main points raised in order of importance. There should be a brief conclusion statement at the end of the Introduction.

4. Main Body Paragraphs with numbered sub-headings – Detailed information which

elaborates on the main points raised in the Introduction. Each paragraph should begin with a clear topic sentence, then supporting sentences with facts and evidence obtained from research and finish with a concluding sentence at the end.

5. Conclusion – A logical and coherent evaluation based on a thorough and an objective assessment of the facts. Key information has been appraised from an analysis of the company's annual report and supplementary research to support the final evaluation of the Auditor's findings based on the selected company's annual report.

6. Appendices – Include any additional explanatory information which is supplementary and/ or graphical to help communicate the main ideas made in the report. Refer to the appendices in the main body paragraphs, as and where appropriate.

Solution

Introduction

AGL Energy Ltd is one of the oldest and largest business houses that provide essential energy led products and services to households and business houses. It also owns the largest private hydro fleet and power station in Australia. The Board plans to put a demerger to be held in the financial year 2022. The number of customers in Australia is increasing and increasing the industry towards energy businesses (AGL, 2021). It is also engaged in battery development in bulk quantities and energy renewable. The company is engaged in energy products and services that will benefit the customers in the long run. Therefore, the company should make aware of the customers for better results.

Background

The Auditor independent declaration highlights the key audit matter on property, plant and equipment and intangible assets. They also reported on financial instruments acquired by the company during the year. The management of the company has unbilled revenue at the reporting period and the invoice was not raised to the customers. Therefore, the auditors have correctly disclosed in the financial statements of the company.

Scope:

The Independent Auditors have complied with Independence requirements. As per section 307C of the corporation's Act 2001, the auditor has given an opinion on the financial report providing a truthful and fair picture of the company's financial situation as of June 30, 2021and also complying with Australian accounting standards (CPA Australia, 2021). The organization also commenced contracts related to long term arrangements for power purchase agreements.

Main Emphasis

The auditor has pointed out the value of goodwill of $ 2,440 million in the property, plant, and equipment in the financial statements of the organization (AGL Energy Limited, 2021). Auditor has pointed out that the company has invested in derivative financial instruments that have been recorded at a fair value price. Auditor also pointed out unbilled revenue due to collection was not executed during the reporting period. The Audit report also emphasizes environmental rehabilitation.

Analysis

Non-Audit Services

During the financial year 2020-21, the external auditor, Deloitte Touché Tohmatsu Australia (Deloitte), provided non-audit services. The Financial Report 2021 contains information about non-audit services. For audits and related services, the organization maintains a management policy. An external auditor, on the other hand, is prohibited from providing any services that would jeopardize its independence. The Board of Directors has approved the policy of external auditors, which is in line with the general standard of auditor independence. Non-audit services are those that auditors give outside of the scope of the audit.

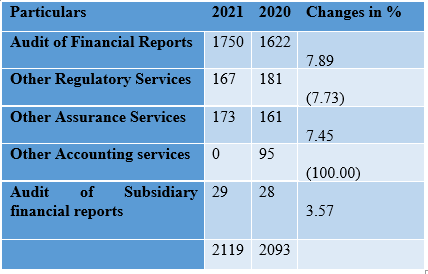

Auditors Remuneration

The analysis of the auditor’s remuneration is shown below with prior year comparisons. (‘$000)

The table shows that remuneration of the auditor has increased by 7.89% as compared to the previous year (AGL Energy Limited, 2021). However, remuneration of the assurance services, assurance services have increased during the current financial year.

Action taken by auditors on Key Audit Matters

Key Audit matters:

1. The auditor has pointed out the value of goodwill of $ 2,440 million in the property, plant, and equipment in the financial statements of the organization (AGL Energy Limited, 2021). However, management conducted impairment expenses on such tangible and intangible assets.

However, the procedure adopted by the auditor is not only limited to obtaining understanding associated with valuation models and boards approval for impairment charges (AUASB, 2021). The auditor has checked the mathematical accuracy of cash flow models. They have also assessed the historical forecasting accuracy.

2. The Auditor has pointed out that the company has invested in derivative financial instruments that have been recorded at a fair value price. The auditor has sought a significant judgement from the management for the valuation and accounting of those financial instruments.

The auditor has obtained the internal risk management process and controls, and systems adopted by the management for relevant accounting. The auditor has checked for accuracy on a testing basis and assessed for hedging effectiveness, the integrity of the models, contract terms and disclosure of their appropriateness in the financial statements.

3. The Auditor also pointed out unbilled revenue due to collection was not being executed during the reporting period.

The auditor has checked for process flows of the organization and key control management to estimate the unbilled amount. The auditor has also checked for management's challenges for assumption, pricing, and distribution tariff rates. These data have been checked on a sample basis by the auditor. They have also compared the historical data and current data. They have also checked for distribution tariff rates.

4. The Audit report also emphasizes making provisions for environmental rehabilitation.

The auditor has advised the company to restore and rehabilitate the environment disturbed by electricity generation. The auditor has asked for the amount of provision for environmental rehabilitation. They have asked for activities conducted for rehabilitation, the expected timing, and regulatory requirements.

The auditor has assessed the rehabilitation cost estimated with an independent expert. They have compared with historical data and also assess inflation rates and discount rates.

5. The company has recorded contracts relating to long term arrangements for power purchase agreements.

The auditor has checked for onerous contracts and also evaluated methods for completeness of unavoidable costs.

Audit Committee Meetings

The company has audit & risk committee meetings in the financial year ended on 30 June 2021. There are about 5 non-executive directors in the company. The company has an audit committee charter, and it is displayed on the company's website. The main purpose of the audit charter is to assist the Board in fulfilling its responsibilities to provide timely financial reports (IIA, 2021). The audit charter reviews and recommends a risk management framework. Members of the audit committee meetings are chosen by the Board of Directors from among the company's non-executive directors. The committee is required to convene at least four times per year. A quorum of two people is required for such gatherings. Every two years, this charter is reviewed and modified.

Audit Opinion

The auditor has given the unqualified report and stated that financial statements prepared were following the corporation’s act 2001 and given a true and fair view on the financial position prepared by the management as of 30 June 2021. The remuneration report for the year ended 30 June 2021 is in complies with section 300A of the corporation's Act 2001.

Difference between Director’s duties and auditor’s responsibilities

Auditor’s responsibilities are to comment or give emphasis on matters that are seen from the external point of view. However, directors’ duties and management responsibilities are to protect the interest of the company. The director has to implement the policies and take responsibility for any adverse happenings. The auditors are assigned with the responsibility of giving an opinion on the policies and financial viability of the organization. The auditor may give an adverse opinion if the documents asked for are not provided. Therefore, they are not implementers, but they are only entrusted with the task of giving an opinion (IAASB, 2021).

Material Subsequent Events

AGL Energy Ltd has received two penalty notices for releasing emissions beyond the limits. The company enhanced the emission limits with amendment limits that took place on June 1, 2021. However, implementation of such limits has to occur from such dates, but it was not followed.

Third-Party Assessment

Being a third-party stakeholder, the auditor has pointed out effective point’s relation to unbilled revenue and collection cycle. The management should make provisions for environmental rehabilitation. The cost of expenditure towards preserving the environment should be prepared by the company. They should take out effective cost emission costs and rehabilitating the environment for destroying the environment.

Follow-up questions

The auditor would be asked whether they have checked for expenditures and incomes earned during the reporting period. During the current financial period, the expenses have increased and whether they have been checked on a testing basis. The auditor is asked for an increase in liabilities and trade receivables. The auditors have to be asking for checking of dividend pay-out ratio as compared to previous declaration dates. The most important question to be asked to auditors is about the disclosure of financial assets acquired by the company during the reporting period.

Conclusion

Though the company has increased its revenue for unbilled collection, the company has not accounted for the actual amount against the sale of electricity. Therefore, the company should adopt measures to generate the bill within the due date and collect the amount accordingly. The company is also advised to show the financial instruments at fair market value. The company should complete contracts and duly give the information to the board and shareholders. It is also advised that the debt of the company is to be reduced and liabilities are also to be reduced as compared with assets. The company is also advised to increase the customer base for increasing the income. The company should contribute towards society as a whole and should maintain the interest of the customers. The company should adopt transparency policies to enhance its customer base. The company should look out for payment to subsidiaries and businesses before finalization and reduce long term loans.

References:

AGL. (2021). About AGL. Retrieved 13 October 2021, from https://www.agl.com.au/about-agl

AGL Energy Limited. (2021). AGL Energy Limited Annual Report 2021. Retrieved 13 October 2021, from https://www.agl.com.au/-/media/aglmedia/documents/about-agl/asx-and-media-releases/2021/210813_fy21annualreport.pdf

AUASB. (2021). Retrieved 13 October 2021, from https://www.auasb.gov.au/admin/file/content102/c3/ASA_500_Compiled_2019-FRL.pdf

CPA Australia. (2021). Audit and assurance | CPA Australia. Retrieved 13 October 2021, from https://www.cpaaustralia.com.au/tools-and-resources/audit-and-assurance

IAASB. (2021). Retrieved 13 October 2021, from https://www.iaasb.org/system/files/meetings/files/Discussed%20September%2018%20-%20Extract%20of%20ISA%20570%20-%20Wording%20Responsibilities%20of%20management%20and%20auditor.pdf

IIA. (2021). Model audit committee charter | Audit committees | Technical guidance | IIA. Retrieved 13 October 2021, from https://www.iia.org.uk/resources/audit-committees/model-audit-committee-charter/#:~:text=The%20audit%20committee%20charter%20sets,within%20the%20audit%20committee%20charter.&text=The%20audit%20committee%20may%20engage,to%20carry%20out%20its%20duties.

- SYSS202 System Software Assignment

- DAT7001 Data Handling and Decision Making

- Essay on Low Minimum Wage Assignment

- MBA600 Capstone Strategy Essay

- HM5003 Economics for Business Report

- EDUC8731 Motivation Cognition and Metacognition Assignment

- MBA5005 Managing Human Capital Assignment

- MBA631 Digital Marketing and Communication Report

- PROJ6000 Principles of Projects Management Report

- MKG102 Consumer Behaviour Assignment

- MITS5505 Knowledge Management Report

- FE7052 International Corporate Finance Coursework

- Financial Decision Making Behaviour Assignment

- BE253 Creating and Managing the New and Entrepreneurial Organisation

- TACC602 Accounting for Business Assignment

- MET 414 Applied Epidemiology Assignment

- INT102 Interpersonal Communication Skills Assignment 3

- FIN600 Financial Management Case Study 2

- MIS608 Agile Project Management

- MGT302A Strategic Management Assignment

.png)

~5.png)

.png)

~1.png)

.png)